PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073447

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073447

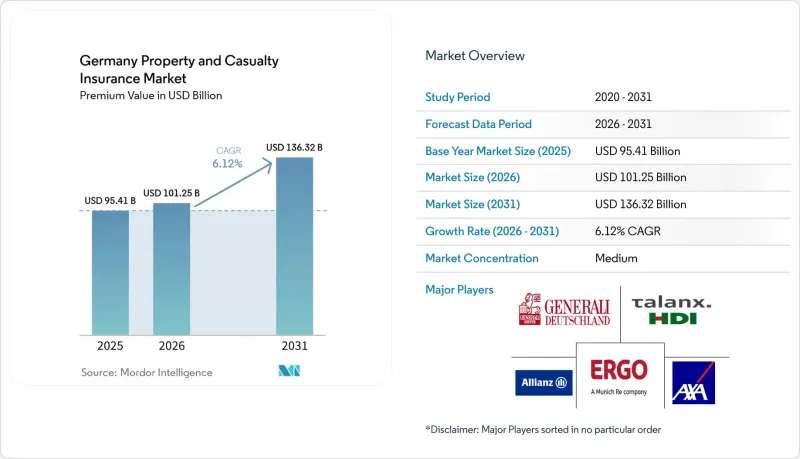

Germany Property and Casualty Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany property and casualty insurance market size in terms of premium value is expected to increase from USD 95.41 billion in 2025 to USD 101.25 billion in 2026 and reach USD 136.32 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Insurance Type (Motor, Property, General Liability, Speciality Lines, and More), Distribution Channel (Direct and Digital, Agents, Brokers, Banks and More), Customer Type (Personal, Commercial Lines, and More), End-User Industry (Manufacturing, Construction and Real Estate, and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

Germany Property and Casualty Insurance Market Trends and Insights

Digitalization and API-first insurance ecosystems driving market

API-first architecture is reshaping how players engage customers and partners. ERGO's tie-up with O2 Telefonica rolled out "O2 Care" in August 2024, embedding device insurance directly in mobile bills and unlocking a demographic that prefers digital-native transactions. Allianz Direct's single-platform model spans multiple EU markets, enabling real-time pricing, instant policy issuance, and low-touch claims flows. As the German property and casualty insurance market scales API connectivity, incumbents integrate motor telematics, travel, and gadget cover into fintech, mobility, and retail ecosystems, broadening reach without heavy fixed-cost sales networks. BaFin's proportionality approach eases supervisory burdens for innovative pilots while keeping consumer protections intact .

Regulatory reforms (IDD, Solvency II review, ESG disclosures) as driver

The 2024 Solvency II recalibration introduced capital-efficiency levers for long-term infrastructure assets and stricter climate-risk stress testing, steering investment toward renewable-energy projects and low-carbon portfolios. From 2025, the Corporate Sustainability Reporting Directive (CSRD) adds mandatory climate-risk disclosure for large insurers, nudging underwriters to integrate ESG metrics into pricing and reserving. IDD enhancements elevate product-suitability duties, favoring players with digital portals that offer real-time comparisons and personalised guidance. Collectively, these shifts strengthen policyholder protection and channel fresh capital into sustainable German infrastructure, enlarging the Germany property and casualty insurance market over the long term.

Claims-cost inflation (auto-repair parts & labor)

Motor insurers face a squeeze as complex sensors in advanced driver-assistance systems and battery-electric drivetrains lift parts prices and workshop times. The German Insurance Association estimates motor-line outgo could exceed USD 38.15 billion for 2024, eroding underwriting margins. Supply-chain bottlenecks and labour shortages add further strain, prompting mid-single-digit premium hikes across the Germany property and casualty insurance market in 2025. Players with direct-repair networks and AI-guided damage appraisal reduce leakage, cushioning profitability.

Other drivers and restraints analyzed in the detailed report include:

- Rise in NatCat losses driving premium growth

- Embedded & usage-based coverages in mobility and retail

- Data-privacy & GDPR compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Motor generated 35.54% of Germany property and casualty insurance market share in 2025, underpinned by mandatory third-party liability and the country's 49 million-plus registered vehicles. Yet, claims inflation forces tariff increases, driving consumers to telematics-based products. Specialty Lines, marine, aviation, and engineering, post a 12.86% CAGR, elevating their contribution to the Germany property and casualty insurance market size through 2031 as Germany expands offshore wind, airport modernisation, and semiconductor-fab construction. Insurers with technical-underwriting depth leverage global facultative reinsurance to capture this growth.

Insured sums for homeowners and commercial property benefit from potential compulsory flood cover. General liability persists as a mid-scale segment but grapples with rising social inflation stemming from collective-redress mechanisms. Accident and supplementary health under P&C regulation see renewed demand as employers expand voluntary benefits. Overall, players that blend usage-based motor offers with engineering and cyber-risk packages balance their risk mix across the Germany property and casualty insurance market.

Brokers and independent agents controlled 44.02% of premiums in 2025. Their advisory depth proves critical for industrial fire, construction all-risk, and multinational programs, sustaining relevance despite fee compression. Direct & digital channels expand 10.88% annually, powered by API gateways that embed household and mobility coverage in e-commerce journeys. The Germany property and casualty insurance market size for broker-sold products still rises, yet its share will dilute gradually as embedded and affinity partners unlock new micro-ticket volumes. These shifts are also influencing the broader Germany life and non-life insurance market, where insurers increasingly adopt unified digital platforms to cross-sell life, health, and property products through integrated customer ecosystems.

Multi-access strategies dominate players roadmaps: virtual video-advice blends with chatbot self-service, while in-branch agents focus on life-event reviews. Bancassurance retains steady household-insurance cross-sales via mortgage portfolios. Affinity schemes with utilities and mobility platforms illustrate how the Germany property and casualty insurance market adopts retail pricing disciplines to lower distribution cost ratios.

Complete Report Scope:

- By Insurance Type

- Motor

- Homeowners / Residential Property

- Commercial Property (incl. Fire & Multi-risk)

- General Liability

- Specialty Lines (Marine, Aviation, Engineering)

- Legal Expense

- Accident & Health (P&C regulated)

- By Distribution Channel

- Direct & Digital

- Tied Agents

- Brokers & Independent Agents

- Banks & Bancassurance

- Affinity & Embedded Partners

- Customer Type

- Personal Lines

- Commercial & SME

- Corporate & Industrial

- By End-user Industry

- Manufacturing

- Construction & Real Estate

- Transportation & Logistics

- Retail & Wholesale

- Professional & Financial Services

- Public Sector & Utilities

- By Region

- Norddeutschland

- Ostdeutschland

- Westdeutschland

- Suddeutschland

List of Companies Covered in this Report:

- Allianz SE

- Munich Re (ERGO, Great Lakes)

- Talanx Group (HDI, Hannover Re)

- AXA Konzern AG

- R+V Versicherung AG

- HUK-Coburg Versicherungsgruppe

- Zurich Insurance plc Germany

- Generali Deutschland

- Gothaer Allgemeine Versicherung AG

- DEVK Versicherungen

- SIGNAL IDUNA Gruppe

- Versicherungskammer Bayern

- Provinzial Versicherung AG

- ARAG SE

- DFV Deutsche Familienversicherung AG

- AdmiralDirekt & Luko / Getsafe (Insurtech)

- Wurttembergische Gemeinde-Versicherung (WGV)

- VHV Gruppe

- Debeka Allgemeine Versicherung

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitalization & API-first insurance ecosystems

- 4.2.2 Regulatory reforms (IDD, Solvency II review, ESG disclosures)

- 4.2.3 Rise in NatCat losses driving premium growth

- 4.2.4 Embedded & usage-based coverages in mobility and retail

- 4.2.5 AI-driven straight-through underwriting efficiencies (under-reported)

- 4.2.6 Mandatory flood cover debate & public-private pool design (under-reported)

- 4.3 Market Restraints

- 4.3.1 Data-privacy & GDPR compliance costs

- 4.3.2 Claims-cost inflation (auto-repair parts & labour)

- 4.3.3 Thin investment yields pressuring combined ratios (under-reported)

- 4.3.4 Growing cyber-risk aggregation limits re/insurance appetite (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Insurance Type

- 5.1.1 Motor

- 5.1.2 Homeowners / Residential Property

- 5.1.3 Commercial Property (incl. Fire & Multi-risk)

- 5.1.4 General Liability

- 5.1.5 Specialty Lines (Marine, Aviation, Engineering)

- 5.1.6 Legal Expense

- 5.1.7 Accident & Health (P&C regulated)

- 5.2 By Distribution Channel

- 5.2.1 Direct & Digital

- 5.2.2 Tied Agents

- 5.2.3 Brokers & Independent Agents

- 5.2.4 Banks & Bancassurance

- 5.2.5 Affinity & Embedded Partners

- 5.3 Customer Type

- 5.3.1 Personal Lines

- 5.3.2 Commercial & SME

- 5.3.3 Corporate & Industrial

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Construction & Real Estate

- 5.4.3 Transportation & Logistics

- 5.4.4 Retail & Wholesale

- 5.4.5 Professional & Financial Services

- 5.4.6 Public Sector & Utilities

- 5.5 By Region

- 5.5.1 Norddeutschland

- 5.5.2 Ostdeutschland

- 5.5.3 Westdeutschland

- 5.5.4 Suddeutschland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Allianz SE

- 6.4.2 Munich Re (ERGO, Great Lakes)

- 6.4.3 Talanx Group (HDI, Hannover Re)

- 6.4.4 AXA Konzern AG

- 6.4.5 R+V Versicherung AG

- 6.4.6 HUK-Coburg Versicherungsgruppe

- 6.4.7 Zurich Insurance plc Germany

- 6.4.8 Generali Deutschland

- 6.4.9 Gothaer Allgemeine Versicherung AG

- 6.4.10 DEVK Versicherungen

- 6.4.11 SIGNAL IDUNA Gruppe

- 6.4.12 Versicherungskammer Bayern

- 6.4.13 Provinzial Versicherung AG

- 6.4.14 ARAG SE

- 6.4.15 DFV Deutsche Familienversicherung AG

- 6.4.16 AdmiralDirekt & Luko / Getsafe (Insurtech)

- 6.4.17 Wurttembergische Gemeinde-Versicherung (WGV)

- 6.4.18 VHV Gruppe

- 6.4.19 Debeka Allgemeine Versicherung

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment