PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072612

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072612

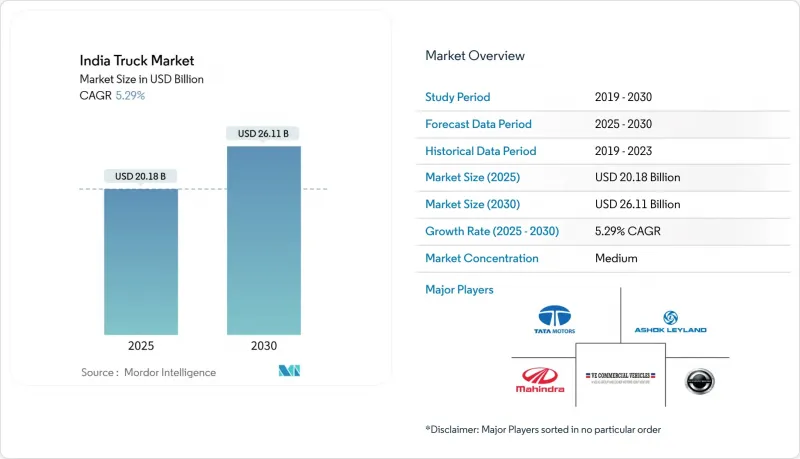

India Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

According to Mordor Intelligence, the indian truck market size stood at USD 20.18 billion in 2025 and is forecast to reach USD 26.11 billion by 2030, reflecting a 5.29% CAGR.

This report is Segmented by Vehicle Type (Light Duty, Medium Duty, and More), Tonnage Capacity (3. 5-7. 5 Tons, 7. 5-16 Tons, and More), Fuel Type (Diesel, Petrol, and More), Application (Logistics, Construction, and More), Ownership (Fleet Operators and Individual Owners), Body Type (Flatbed, Box Truck, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

India Truck Market Trends and Insights

Government Infrastructure Push (Bharatmala, Gati Shakti)

In FY24, the National Highways Authority of India (NHAI) set a new benchmark by investing a staggering Rs. 2,07,000 crore (USD 24.79 billion) in national highway construction. This capital outlay marked a record high, surging 20% from the previous fiscal year. For the Union Budget 2025-26, the government earmarked Rs. 2,87,333.3 crore (USD 33.07 billion) for the Ministry of Road Transport and Highways, a modest 2.41% increase from FY25's allocations. Completing 19,201 km of economic corridors by 2025 already lifts tipper and tractor-trailer utilization. New axle-load norms align with higher-capacity fleets, guiding OEM chassis design. The Indian truck market responds with heavier configurations optimized for bulk cement, steel, and coal haulage. Rising freight density on the Delhi-Mumbai route alone supports continuous-duty cycles that improve truck total cost of ownership.

E-commerce-Led Logistics Boom

India's logistics sector is experiencing a rapid transformation, driven by a sharp rise in parcel deliveries, fueling continuous demand for trucking services in the India truck market. Leading e-commerce companies are expanding their delivery networks and infrastructure to meet growing consumer expectations for faster service. As logistics operations extend deeper into smaller cities, freight routes are reoriented toward new consumption hubs, increasing the need for agile, light-duty vehicles suited for urban environments. Technological advancements in telematics enhance route efficiency and vehicle productivity, making the trucking ecosystem more responsive and optimized for evolving market dynamics.

High BS-VI Truck Capex

Mandatory BS-VI upgrades and AC cabs add INR 20,000-30,000 (USD 250-375) per unit from October 2025, elevating industry capex to INR 60 billion (USD 750 million) in FY26 . Small operators, still 70% of ownership, struggle with higher EMIs, delaying fleet refresh, and dampening near-term demand within the India truck market.

Other drivers and restraints analyzed in the detailed report include:

- Scrappage Policy-Driven Replacement Demand

- Shift to CNG/LNG on TCO Benefits

- Volatile Diesel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light-duty trucks held 48.33% of 2024 shipments, underpinning the India truck market while posting a 6.94% CAGR through 2030. Urban road restrictions and e-commerce time windows favor compact wheelbases that weave through dense streets. OEM financing schemes and low-maintenance EV drivetrains further tilt demand toward this class. Medium-duty units cater to regional express lines, whereas heavy tractors dominate cement, steel, and coal corridors. Light-duty electrification unlocks rapid payback on 200-km urban routes, supported by depot chargers that bypass public-grid constraints.

Second-generation models such as Magenta Mobility's 3-ton EV now complete three turns daily, doubling asset productivity and reshaping cost curves. Meanwhile, rising ton-mile demand from Tier-3 trade clusters preserves internal-combustion variants, keeping the segment an indispensable growth engine within the India truck market.

Trucks in the 3.5-7.5 ton band captured 39.18% of 2024 volume, reflecting India's granular retail networks that call for payload agility rather than brute capacity. Their 7.14% CAGR stands above all other tonnage classes as omnichannel retailers push fast replenishment to micro-warehouses. Tight municipal axle mandates and low-bridge clearances reinforce small-tonnage utility.

Continued highway upgrades could gradually swing freight toward 16-ton gross vehicle weights for hub-to-hub lanes, yet doorstep delivery promises keep sub-7.5-ton demand vibrant. Strategically, OEMs overlay modular body kits to stretch platform economics, augmenting the India truck market size through SKU diversity without new homologation cycles.

Complete Report Scope:

- By Vehicle Type

- Light Duty

- Medium Duty

- Heavy Duty

- By Tonnage Capacity

- 3.5-7.5 Tons

- 7.5-16 Tons

- 16-30 Tons

- Above 30 Tons

- By Fuel Type

- Diesel

- Petrol

- Electric

- Other Fuel Type

- By Application

- Logistics

- Construction

- Agriculture

- Mining

- Utility

- Others

- By Ownership

- Fleet Operators

- Individual Owners

- By Body Type

- Flatbed

- Box Truck

- Refrigerated

- Tanker

- Tipper

List of Companies Covered in this Report:

- Tata Motors Limited

- Ashok Leyland

- Mahindra & Mahindra Limited

- VE Commercial Vehicles Ltd. (Eicher)

- BharatBenz (Daimler India Commercial Vehicles)

- Volvo Trucks India

- Scania Commercial Vehicles India Pvt. Ltd.

- Force Motors Limited

- Isuzu Motors India Private Limited

- Hino Motors India

- Olectra Greentech

- BYD India

- Omega Seiki Mobility

- Tresa Motors

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Infrastructure Push (Bharatmala, Gati Shakti)

- 4.2.2 E-commerce-Led Logistics Boom

- 4.2.3 Scrappage Policy-Driven Replacement Demand

- 4.2.4 Shift to CNG/LNG on TCO Benefits

- 4.2.5 Cold-Chain Expansion in Tier-2/3 Cities

- 4.2.6 Connected-Truck Telematics Adoption

- 4.3 Market Restraints

- 4.3.1 High BS-VI Truck Capex

- 4.3.2 Volatile Diesel Prices

- 4.3.3 Driver Shortage and Aging Workforce

- 4.3.4 Sparse Heavy-Duty Charging Network

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value and Volume)

- 5.1 By Vehicle Type

- 5.1.1 Light Duty

- 5.1.2 Medium Duty

- 5.1.3 Heavy Duty

- 5.2 By Tonnage Capacity

- 5.2.1 3.5-7.5 Tons

- 5.2.2 7.5-16 Tons

- 5.2.3 16-30 Tons

- 5.2.4 Above 30 Tons

- 5.3 By Fuel Type

- 5.3.1 Diesel

- 5.3.2 Petrol

- 5.3.3 Electric

- 5.3.4 Other Fuel Type

- 5.4 By Application

- 5.4.1 Logistics

- 5.4.2 Construction

- 5.4.3 Agriculture

- 5.4.4 Mining

- 5.4.5 Utility

- 5.4.6 Others

- 5.5 By Ownership

- 5.5.1 Fleet Operators

- 5.5.2 Individual Owners

- 5.6 By Body Type

- 5.6.1 Flatbed

- 5.6.2 Box Truck

- 5.6.3 Refrigerated

- 5.6.4 Tanker

- 5.6.5 Tipper

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Tata Motors Limited

- 6.4.2 Ashok Leyland

- 6.4.3 Mahindra & Mahindra Limited

- 6.4.4 VE Commercial Vehicles Ltd. (Eicher)

- 6.4.5 BharatBenz (Daimler India Commercial Vehicles)

- 6.4.6 Volvo Trucks India

- 6.4.7 Scania Commercial Vehicles India Pvt. Ltd.

- 6.4.8 Force Motors Limited

- 6.4.9 Isuzu Motors India Private Limited

- 6.4.10 Hino Motors India

- 6.4.11 Olectra Greentech

- 6.4.12 BYD India

- 6.4.13 Omega Seiki Mobility

- 6.4.14 Tresa Motors

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment