PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072615

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072615

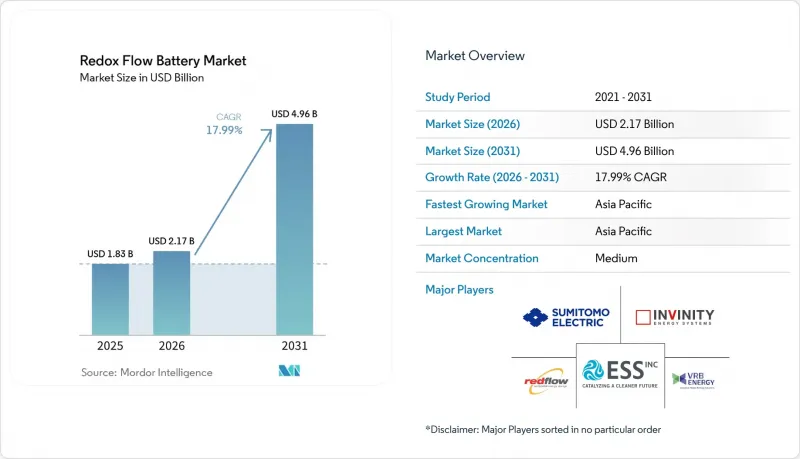

Redox Flow Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the redox flow battery market size is projected to expand from USD 1.83 billion in 2025 and USD 2.17 billion in 2026 to USD 4.96 billion by 2031, registering a CAGR of 17.99% between 2026 to 2031.

This report is Segmented by Type (Vanadium Redox Flow Battery, and More), Application (Utility-Scale Energy Storage, Commercial and Industrial Facilities, and More), End-User (Power Utilities/IPPs, Commercial and Industrial Owners, Government and Defense, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Redox Flow Battery Market Trends and Insights

Grid-Stability Mandates Drive Wholesale Market Integration

Federal Energy Regulatory Commission Order 841 obliges U.S. wholesale markets to accept storage assets for all services for which they are technically capable, unlocking new revenue streams for flow batteries that previously relied on behind-the-meter savings alone. Europe's Clean Energy Package imposes similar reforms by 2026, and developers have already announced 1.2 GW of flow projects in Germany, the United Kingdom, and the Nordic region. Order 2222 further aggregates distributed resources, allowing commercial sites to pool flow batteries and earn capacity and ancillary revenue, which shortens project payback from 12 years to 7 years in solar-heavy states. U.S. utilities in California and Texas now issue tenders that explicitly favor non-lithium chemistries for six-hour-plus services because flow systems decouple power and energy, enabling incremental capacity additions without full system replacement. Mandates, therefore, underpin scheduling flexibility and economic certainty, accelerating procurement decisions across both regulated and deregulated markets.

Vanadium Leasing Models Accelerate Capital Cost Reduction

Electrolyte leasing agreements, exemplified by Storion Energy's USD 85 kWh program, cut initial capital requirements by up to 60% and transfer commodity risk to the lessor. Because vanadium retains 99% recyclability, leasing firms can redeploy electrolyte over multiple 20-year cycles, creating a circular-economy advantage that lithium-ion lacks. Chinese developers have validated lease-to-own structures that convert operating expenses into asset ownership after roughly a decade, aligning cost profiles with corporate renewable PPAs. Academic studies project that ten-hour vanadium systems fall below USD 300 kWh when electrolyte is leased, undercutting lithium iron phosphate at equivalent durations. As financial innovations diffuse globally, capital-intensive long-duration projects gain bankability, widening the total addressable redox flow battery market.

Volatile Vanadium Pricing Creates Investment Uncertainty

Vanadium pentoxide fell from USD 9.20 lb in 2022 to USD 5.60 lb in March 2026, a 40% slide tied to weak Chinese steel demand. Although the slump lowered capex for new projects, uncertainty complicates long-term offtake agreements and deters lenders. CRU Group expects demand from China's 12 GWh mandate to lift prices later in the decade, but fresh supply from Brazil and Madagascar could mute any rally. Developers thus hedge price swings through electrolyte leasing, but fluctuations still sway debt-service coverage ratios, marginally slowing redox flow battery market growth.

Other drivers and restraints analyzed in the detailed report include:

- Solar and Wind LCOE Parity Creates Duration-Specific Storage Demand

- Corporate Net-Zero Procurement Drives 8-12-Hour Storage PPAs

- Lower Round-Trip Efficiency Versus Lithium-Ion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vanadium designs maintained 49.2% redox flow battery market share in 2025 on the back of a mature ecosystem in China, Japan, and South Korea. Iron flow systems, however, are projected to grow at 22.2% CAGR to 2031 as vendors eliminate reliance on critical minerals and boost energy density 20% over first-generation stacks. Vanadium's dominance persists because 99% electrolyte recyclability underwrites residual value at end-of-life, yet feedstock volatility nudges risk-averse financiers toward iron alternatives. Zinc-bromine occupies telecom backup and off-grid niches, while organic and hybrid concepts remain pre-commercial. Over the forecast period, technology pluralism is likely, with regional policies shaping deployment preferences rather than a single chemistry winning outright in the redox flow battery market.

Second-generation vanadium stacks now tout 20,000-cycle lifetimes, double that of lithium iron phosphate, supporting warranty terms that appeal to infrastructure investors seeking stable cash flows. Meanwhile, membrane innovators are striving for PFAS-free solutions to pre-empt European regulation. Altogether, technology shifts are starting to erode barriers to entry, suggesting that vanadium's share may slip below 40% by 2031 even as absolute shipments grow, broadening competitive dynamics within the redox flow battery market.

Complete Report Scope:

- By Type

- Vanadium Redox Flow Battery (VRFB)

- Zinc-Bromine Flow Battery

- Iron Flow Battery

- Organic/Hybrid Flow Battery

- Other Chemistries (e.g., Fe/Cr, H2-Br2)

- By Application

- Utility-Scale Energy Storage (Above 10 MWh)

- Micro-grids and Islands

- Commercial and Industrial Facilities

- Residential Nanogrids

- EV-Charging Plaza Buffering

- Other (Defense, Mining, Off-grid Telecom)

- By End-user

- Power Utilities/IPPs

- Renewable Project Developers

- Commercial and Industrial Owners

- Government and Defense

- Research and Academic

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific held 45.9% of capacity in 2025 and is forecast to maintain a 19.3% CAGR through 2031, chiefly due to China's 12 GWh mandate for vanadium systems that decouple renewable volatility. Provincial subsidies of USD 0.04 - 0.07 kWh guarantee dispatch revenues, while domestic giants like Rongke Power are erecting an 800 MWh array in Hubei slated for 2026 completion. Japan and Australia are piloting iron flow chemistries to hedge critical-mineral exposure, signaling chemistry diversification across the region.

North America contributed a significant share of capacity in 2025, but with Section 45X tax credits in force until 2029, the region's share of the redox flow battery market size could climb to one-third by 2031. California alone procured 1.8 GW of long-duration storage in 2024, 40% of which favored flow chemistry for six-hour-plus services. Canadian provinces are evaluating flow systems to firm hydropower exports, while Mexico's utility CFE is reviewing tender guidelines for eight-hour storage near industrial corridors, illustrating expanding continental demand. Sumitomo Electric's 51-megawatt, 306-megawatt-hour California installation, operational in 2024, is the largest North American deployment, showcasing Japanese manufacturers' U.S. market share gains. Europe, with 18% of 2025 capacity, led by Germany and the UK, is advancing PFAS-free membrane technologies. The European Chemicals Agency's updated PFAS restriction dossier and final opinions drive investments by IONOMR, Fraunhofer IAP, and Cellfion, positioning European suppliers to meet regulatory-driven demand.

Germany's innovation auctions and the United Kingdom's Capacity Market both award duration bonuses that materially improve flow economics. Yet pending PFAS restrictions raise execution risk for legacy membrane suppliers, prompting OEMs to accelerate PFAS-free rollouts. Scandinavia and the Baltic states, vested in wind-plus-hydrogen hybrids, now include flow batteries in project pipelines to mitigate seasonal deficits.

Chile and Brazil are mapping policy frameworks that value long-duration storage as a transmission alternative, while South Africa's Eskom deployed a 12 MWh vanadium system to cut load shedding, demonstrating applicability in emerging grids. These regions could collectively account for 8 GWh of cumulative deployments by 2031 as solar LCOE parity spreads.

- Sumitomo Electric Industries

- VRB Energy

- Invinity Energy Systems

- ESS Inc.

- Redflow Limited

- Primus Power

- Largo Clean Energy

- CellCube (Enerox GmbH)

- VoltStorage GmbH

- VFlow Tech

- Lockheed Martin (GridStar Flow)

- HydraRedox

- H2 Inc.

- Bushveld Energy

- Rongke Power

- Stryten Energy

- EnerVenue

- UniEnergy Tech (UET)

- Volterion GmbH

- StorEn Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-stability mandates (FERC 841, EU-Clean-Energy Package)

- 4.2.2 Rapid cost decline of vanadium leasing models

- 4.2.3 Solar & Wind LCOE parity creating long-duration storage gaps

- 4.2.4 Corporate net-zero procurement of 8-12 h storage PPAs

- 4.2.5 "Made-in-USA" tax credits for non-Li chemistries (Inflation Reduction Act under Section 45X)

- 4.2.6 Data-center drive for 99.999 % uptime micro-grids (Over 10 h)

- 4.3 Market Restraints

- 4.3.1 Volatile vanadium price linked to steel demand

- 4.3.2 Lower round-trip efficiency vs Li-ion

- 4.3.3 PFAS-free membrane regulations raising cost of legacy stacks

- 4.3.4 Long permitting cycle for Above 50 MWh electrolyte trucking & Haz-mat storage

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Vanadium Redox Flow Battery (VRFB)

- 5.1.2 Zinc-Bromine Flow Battery

- 5.1.3 Iron Flow Battery

- 5.1.4 Organic/Hybrid Flow Battery

- 5.1.5 Other Chemistries (e.g., Fe/Cr, H2-Br2)

- 5.2 By Application

- 5.2.1 Utility-Scale Energy Storage (Above 10 MWh)

- 5.2.2 Micro-grids and Islands

- 5.2.3 Commercial and Industrial Facilities

- 5.2.4 Residential Nanogrids

- 5.2.5 EV-Charging Plaza Buffering

- 5.2.6 Other (Defense, Mining, Off-grid Telecom)

- 5.3 By End-user

- 5.3.1 Power Utilities/IPPs

- 5.3.2 Renewable Project Developers

- 5.3.3 Commercial and Industrial Owners

- 5.3.4 Government and Defense

- 5.3.5 Research and Academic

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Sumitomo Electric Industries

- 6.4.2 VRB Energy

- 6.4.3 Invinity Energy Systems

- 6.4.4 ESS Inc.

- 6.4.5 Redflow Limited

- 6.4.6 Primus Power

- 6.4.7 Largo Clean Energy

- 6.4.8 CellCube (Enerox GmbH)

- 6.4.9 VoltStorage GmbH

- 6.4.10 VFlow Tech

- 6.4.11 Lockheed Martin (GridStar Flow)

- 6.4.12 HydraRedox

- 6.4.13 H2 Inc.

- 6.4.14 Bushveld Energy

- 6.4.15 Rongke Power

- 6.4.16 Stryten Energy

- 6.4.17 EnerVenue

- 6.4.18 UniEnergy Tech (UET)

- 6.4.19 Volterion GmbH

- 6.4.20 StorEn Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment