PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072654

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072654

United States Customer Relationship Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

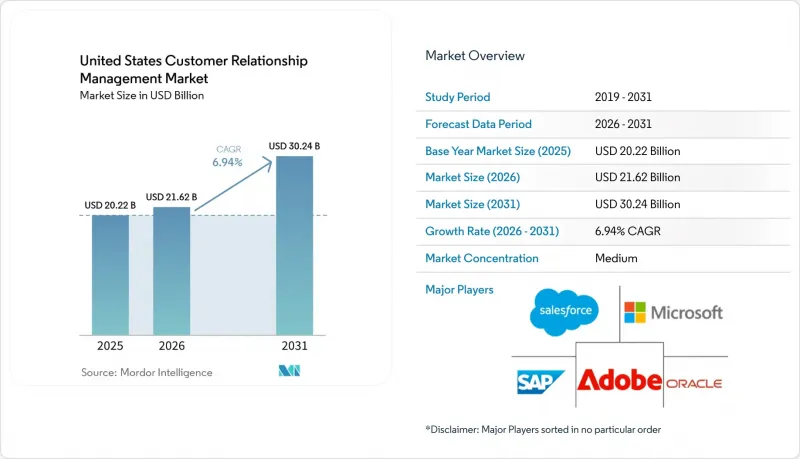

According to Mordor Intelligence, the united states customer relationship management market size was valued at USD 20.22 billion in 2025 and is estimated to grow from USD 21.62 billion in 2026 to reach USD 30.24 billion by 2031, at a CAGR of 6.94% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premise, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Sales Force Automation, Marketing Automation, and More), End-User Industry (BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

United States Customer Relationship Management Market Trends and Insights

AI Copilots and Autonomous Agents In Frontline Workflows

AI agents inside frontline systems are moving the United States customer relationship management market away from feature comparison and toward measurable workflow execution. ServiceNow said in May 2026 that its Autonomous CRM for Sales and Service was already resolving more than 100 million customer cases, orchestrating more than 16 million orders, and configuring more than 7 million quotes each month, which gives the market a clear operating benchmark for large-scale autonomous work. Salesforce also framed this shift around continuous digital labor, positioning Agentforce Sales as a 24-7 workforce that can execute repetitive selling tasks inside CRM environments. As more L1 and L2 tasks move to software agents, human teams are being redirected toward exception handling, approvals, and judgment-heavy work, which raises the value of each active user rather than simply expanding user counts. That dynamic increases switching friction because the vendor increasingly owns the work layer, not only the system of record. California's effective 2026 rules also add human oversight and opt-out obligations around automated decision-making, which means adoption in the United States customer relationship management (CRM) market is rising alongside governance requirements, not outside them.

Cloud-First CRM Modernization

Cloud modernization remains a central growth engine for the United States CRM market because vendors are now using rapid release cycles as a product advantage. Salesforce's Summer '26 release added multi-agent orchestration, Slack-first workflows, real-time data activation, and broader AI engagement tools, showing how new functionality is being delivered through cloud-native update cadences rather than periodic upgrade projects. ServiceNow followed a similar path in 2025 and 2026 by recasting CRM around one unified platform for selling, fulfillment, and service, then layering governed AI controls on top of that operating model. The result is that cloud migration is no longer centered only on infrastructure efficiency, it is increasingly tied to access to new AI functions, faster service releases, and better interoperability across adjacent systems. That shift also explains why service demand is rising, because cloud-led modernization often requires integration redesign, change management, and ongoing administration. In the US CRM market, this makes cloud migration both a software growth driver and a services growth driver at the same time.

State-By-State Privacy and Consent Complexity

State privacy fragmentation remains one of the clearest constraints on the United States customer relationship management (CRM) market because CRM data flows now sit directly inside consent, personalization, and automated decision-making processes. IAPP said that 20 comprehensive state privacy laws were in effect as 2026 began, which means companies must manage materially different obligations across multiple jurisdictions. California's updated CCPA framework also took effect on January 1, 2026, with rules around opt-out processing, risk assessments, and other compliance obligations that directly affect CRM operating models. For platform buyers, that turns privacy variation into a product selection issue, because consent workflows, jurisdiction logic, and audit trails have to work inside daily operations instead of being handled through manual workarounds. It also lengthens implementation cycles because national deployments cannot assume a single compliance standard. In the United States CRM market, that slows some projects even while it pushes demand toward platforms with stronger policy controls.

Other drivers and restraints analyzed in the detailed report include:

- First-Party Data Unification Through CDPs

- SME Adoption Via Lower-Cost Modular Suites

- Legacy Integration and Switching Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 75.22% of the United States customer relationship management market size in 2025, which kept the revenue base anchored in platform ownership across sales, marketing, service, and data functions. This leadership reflects the central role of CRM software as the operating layer for customer records, workflow routing, campaign execution, and service resolution across large enterprises and growing mid-market users. In the United States customer relationship management (CRM) market, software also remains the main point where vendors differentiate on AI, data activation, low-code configuration, and user productivity. Customer data management and analytics functions are drawing a larger share of product investment because the value of CRM now depends on how well the platform can unify customer context and activate it across multiple teams. Salesforce's November 2025 Informatica acquisition reinforced this direction by adding data catalog, governance, quality, privacy, metadata management, and master data management capabilities that strengthen the data foundation sitting under CRM workflows.

Services, while smaller in revenue terms, is projected to grow at a 7.12% CAGR during 2026-2031, which places it ahead of the overall market and signals a shift in how value is captured. The United States CRM market is becoming harder to implement through simple template rollouts because organizations are connecting more clouds, more data sources, and more AI-enabled processes inside one operating model. That change favors implementation partners, managed service providers, and specialist consultants that can redesign processes, not only configure screens. Service revenue is also being supported by longer onboarding cycles, more governed AI deployment, and greater demand for ongoing platform administration after go-live. In effect, software still anchors spending, but the US CRM market is increasingly monetizing the complexity required to make those platforms work well at scale.

Cloud held 79.54% of the United States customer relationship management (CRM) market share by deployment mode in 2025, confirming that SaaS delivery remains the preferred model for most organizations. Cloud leadership reflects the need for continuous feature delivery, elastic scaling, and direct access to new AI capabilities that are arriving through frequent vendor releases. In the United States customer relationship management market, these benefits matter more as enterprises tie CRM to workflow automation, real-time data activation, and cross-functional collaboration. Salesforce's Summer '26 release and its broader Agentforce roadmap show how quickly new capabilities are now being introduced into production environments, which favors cloud-centered operating models. That pace makes on-premise environments less attractive for organizations that want immediate access to autonomous service, guided selling, and AI-assisted administration.

Hybrid is expected to grow at a 7.67% CAGR during 2026-2031, which makes it the fastest-growing deployment approach in this segmentation. That trend does not signal hesitation about cloud adoption, instead it reflects a practical architecture choice for organizations that need tighter control over sensitive data and regulated workflows. The United States CRM market is seeing hybrid demand from sectors that cannot move every process into a pure public cloud model while still needing cloud-native innovation. Salesforce Headless 360 supports this pattern by letting organizations expose CRM logic through APIs and tools while controlling how data is surfaced across external environments. On-premise remains relevant in narrower regulated settings, but hybrid is the segment that best captures how buyers are balancing innovation speed with control requirements.

Complete Report Scope:

- By Component

- Software

- Sales Force Automation Platforms

- Marketing Automation Platforms

- Customer Service and Support Suites

- Customer Data Platforms

- Digital Commerce Engines

- Analytics and Insights Tools

- Services

- Implementation and Integration

- Consulting

- Training and Support

- Managed Services

- Software

- By Deployment Mode

- Cloud

- Public Cloud

- Private Cloud

- Multi-cloud

- On-premise

- Hybrid

- Cloud

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Application

- Sales Force Automation

- Marketing Automation

- Customer Service and Support

- Digital Commerce

- Analytics and Insights

- Revenue Operations (RevOps)

- Partner Relationship Management

- By End-user Industry

- BFSI

- Retail and E-Commerce

- Healthcare and Life Sciences

- IT and Telecom

- Manufacturing

- Media and Entertainment

- Professional Services

- Other End-user Industries

- By Country

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Salesforce, Inc.

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Adobe Inc.

- HubSpot, Inc.

- Zoho Corporation

- Zendesk, Inc.

- Freshworks Inc.

- SugarCRM Inc.

- Creatio Ltd.

- Pegasystems Inc.

- monday.com Ltd.

- Pipedrive OU

- Copper CRM, Inc.

- Insightly, Inc.

- Nimble Holdings, Inc.

- ServiceNow, Inc.

- Bitrix24 Ltd.

- Keap

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI copilots and autonomous agents in frontline workflows

- 4.2.2 Cloud-first CRM modernization

- 4.2.3 First-party data unification through CDPs

- 4.2.4 SME adoption via lower-cost modular suites

- 4.2.5 Zero-copy and headless CRM activation

- 4.2.6 RevOps automation for routing and forecast accuracy

- 4.3 Market Restraints

- 4.3.1 State-by-state privacy and consent complexity

- 4.3.2 Legacy integration and switching costs

- 4.3.3 AI-ready data quality gaps

- 4.3.4 Agent governance and auditability burden

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of buyers

- 4.7.3 Bargaining power of suppliers

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Sales Force Automation Platforms

- 5.1.1.2 Marketing Automation Platforms

- 5.1.1.3 Customer Service and Support Suites

- 5.1.1.4 Customer Data Platforms

- 5.1.1.5 Digital Commerce Engines

- 5.1.1.6 Analytics and Insights Tools

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Consulting

- 5.1.2.3 Training and Support

- 5.1.2.4 Managed Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.1.1 Public Cloud

- 5.2.1.2 Private Cloud

- 5.2.1.3 Multi-cloud

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.2.1 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Application

- 5.4.1 Sales Force Automation

- 5.4.2 Marketing Automation

- 5.4.3 Customer Service and Support

- 5.4.4 Digital Commerce

- 5.4.5 Analytics and Insights

- 5.4.6 Revenue Operations (RevOps)

- 5.4.7 Partner Relationship Management

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Retail and E-Commerce

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 IT and Telecom

- 5.5.5 Manufacturing

- 5.5.6 Media and Entertainment

- 5.5.7 Professional Services

- 5.5.8 Other End-user Industries

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Salesforce, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 SAP SE

- 6.4.5 Adobe Inc.

- 6.4.6 HubSpot, Inc.

- 6.4.7 Zoho Corporation

- 6.4.8 Zendesk, Inc.

- 6.4.9 Freshworks Inc.

- 6.4.10 SugarCRM Inc.

- 6.4.11 Creatio Ltd.

- 6.4.12 Pegasystems Inc.

- 6.4.13 monday.com Ltd.

- 6.4.14 Pipedrive OU

- 6.4.15 Copper CRM, Inc.

- 6.4.16 Insightly, Inc.

- 6.4.17 Nimble Holdings, Inc.

- 6.4.18 ServiceNow, Inc.

- 6.4.19 Bitrix24 Ltd.

- 6.4.20 Keap

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment