PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073522

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073522

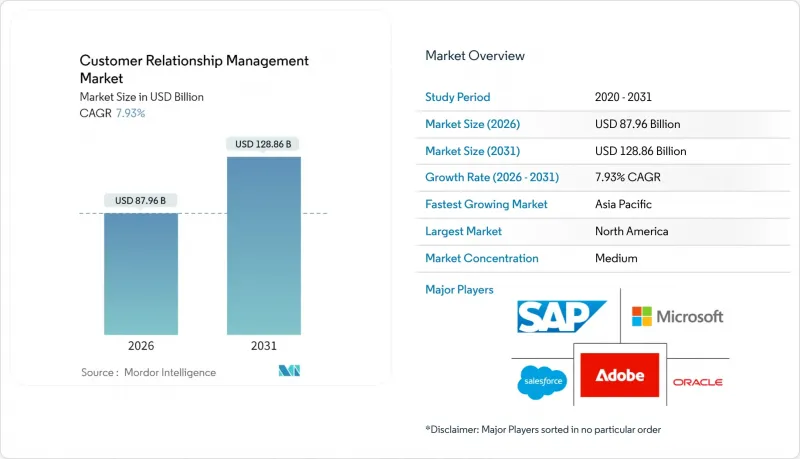

Customer Relationship Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the customer relationship management market size is USD 87.96 billion in 2026 and is projected to rise to USD 128.86 billion by 2031, reflecting a 7.93% CAGR.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Organization Size (Small and Medium Enterprises (SMEs), and Large Enterprises), Application (Sales Force Automation, Marketing Automation, and More), End-User Industry (BFSI, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Customer Relationship Management Market Trends and Insights

Rapid Integration of AI Machine Learning for Predictive Insights

Predictive models inside the Customer Relationship Management (CRM) market forecast churn, next-best actions, and deal closure probability at accuracy levels topping 80%, letting teams focus on high-value prospects. Salesforce Einstein generated more than 1 trillion predictions weekly by mid-2025, demonstrating how inference workloads have become core infrastructure rather than add-ons. Microsoft Copilot parses emails, transcripts, and CRM activity logs to suggest personalized outreach timing, lifting pilot win rates by 12%. SAP's Joule copilot allows natural-language pipeline queries, giving users instant dashboards without writing SQL. AI-generated call scripts shorten onboarding for new hires, while EU firms must document model logic under the AI Act.

Accelerated Shift Toward Cloud-based Deployment

Cloud architectures dominate the Customer Relationship Management market, removing capital expenditure and enabling pay-as-you-grow consumption. Salesforce said 87% of new implementations in 2024 were cloud-based. Oracle's multi-cloud option lets Fusion CX run on Azure or Google Cloud, cutting lock-in risk. Hybrid remains vital for regulated sectors that keep core data on-premise while using cloud analytics engines. Low-tier SaaS plans below USD 15 per user per month spur SME uptake, and ISO 27001 or SOC 2 compliance is now baseline.

High Total Cost of Ownership and Customization

License fees cover only 20% to 30% of overall spend as integration, data migration, and change management dominate budgets. Salesforce's transition from Classic to Lightning in 2024 forced many customers to refactor custom components, inflating consulting bills and delaying rollouts. Proprietary code in debt collection software often becomes technical debt when vendors deprecate APIs. Ongoing costs include user training and premium tiers that unlock higher API limits. Simplified alternatives from Pipedrive or Copper lower entry prices, yet limited extensibility constrains complex sales models. Procurement cycles lengthen as buyers scrutinize total cost over multiyear horizons.

Other drivers and restraints analyzed in the detailed report include:

- Digital Transformation Programs Among SMEs

- Generative AI Copilots and Autonomous CRM Capabilities

- Data-Privacy and Compliance Complexities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are expanding at 9.52% CAGR, outperforming software despite software's 74.12% revenue share in 2025 within the customer relationship management (CRM) market. Implementation contracts dominate as enterprises wire CRM to ERP, e-commerce, and data warehouses. Consulting teams map customer journeys and configure dashboards that match hierarchies. Training and support attract SMEs lacking in-house admins, while managed services grow fastest among firms preferring outsourced platform upkeep.

Software continues to innovate through no-code builders and industry templates, yet diverse use cases keep bespoke work common. Salesforce's professional-services arm generated more than USD 1.5 billion in fiscal 2025. Adobe Experience Cloud rollouts often require integrators for 6-12 months. Regulatory friction is limited, though managed-service providers in healthcare or finance need ISO 27001 and SOC 2 clearance.

Cloud commanded 80.16% share in 2025, led by public-cloud uptake across North America and Western Europe in the CRM market. Private-cloud persists where data-residency rules dominate, and on-premise remains mainly within government entities. Hybrid architectures are rising at 9.04% CAGR, pairing on-premise storage with cloud analytics to access GPUs for AI-driven insight.

IBM offers hybrid CRM on Red Hat OpenShift, syncing local data with Watson AI services. The Digital Markets Act forces gatekeepers to open APIs, smoothing hybrid integration. FedRAMP and C5 certifications elevate vendor costs but deter smaller rivals. Multi-cloud distribution mitigates outage risk and pricing leverage, with Oracle and SAP each supporting rival clouds.

Complete Report Scope:

- By Component

- Software

- Sales Force Automation Platforms

- Marketing Automation Platforms

- Customer Service and Support Suites

- Customer Data Platforms

- Digital Commerce Engines

- Analytics and Insights Tools

- Services

- Implementation and Integration

- Consulting

- Training and Support

- Managed Services

- Software

- By Deployment Mode

- Cloud

- Public Cloud

- Private Cloud

- Multi-cloud

- On-premise

- Hybrid

- Cloud

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Application

- Sales Force Automation

- Marketing Automation

- Customer Service and Support

- Digital Commerce

- Analytics and Insights

- Revenue Operations (RevOps)

- Partner Relationship Management

- By End-user Industry

- BFSI

- Retail and E-Commerce

- Healthcare and Life Sciences

- IT and Telecom

- Manufacturing

- Media and Entertainment

- Professional Services

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America generated 44.18% of Customer Relationship Management market revenue in 2025. U.S. enterprises adopt full-suite platforms that merge sales, service, and commerce, supported by dense SaaS ecosystems. Salesforce earned more than USD 34 billion in fiscal 2025 with roughly 60% bookings from the region. The California Privacy Rights Act imposes consent-management and data-correction duties, yet legal clarity and mature data centers sustain leadership.

Asia Pacific will expand at 8.86% CAGR to 2031, the fastest regional pace. India's cloud-credit vouchers and training support more than 50,000 SMEs, catalyzing adoption. China's Personal Information Protection Law obliges local data storage, creating openings for domestic vendors like Kingdee and UFIDA. Japan migrates from on-premise to cloud CRM, while Singapore positions itself as a SaaS hub for Southeast Asia. Diverse languages and regulations complicate rollouts, yet e-commerce expansion keeps demand strong.

Europe contributes a mid-tier share anchored by Germany, the United Kingdom, and France. GDPR enforces deletion rights and stringent consent, raising compliance budgets but leveling the playing field. The Digital Markets Act requires gatekeepers to provide data portability and API access, lowering switching costs and encouraging challenger platforms. Russia's segment contracted after vendor exits, whereas the Middle East and Africa show pockets of growth as governments digitize citizen services. Latin America gains momentum through Brazilian and Mexican omnichannel retail investment in the CRM market.

- Salesforce, Inc.

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Adobe Inc.

- HubSpot, Inc.

- Zoho Corporation Pvt. Ltd.

- Zendesk, Inc.

- Freshworks Inc.

- SugarCRM Inc.

- Pipedrive Inc.

- Insightly, Inc.

- Copper CRM, Inc.

- monday.com Ltd.

- Keap Inc. (Infusionsoft)

- The Sage Group plc

- Infor, Inc.

- International Business Machines Corporation

- ServiceNow, Inc.

- Pegasystems Inc.

- NICE Ltd.

- Genesys Telecommunications Laboratories, Inc.

- Creatio EMEA Ltd.

- Bitrix24 Ltd.

- VTiger CRM, Inc.

- Epicor Software Corporation

- Aptean, Inc.

- Intercom, Inc.

- Gainsight, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Integration of AI and Machine Learning for Predictive Insights

- 4.2.2 Accelerated Shift Toward Cloud-based Deployment

- 4.2.3 Digital Transformation Programs Among SMEs

- 4.2.4 Omnichannel Engagement and Hyper-personalization

- 4.2.5 Vertical-specific SaaS CRM Ecosystems

- 4.2.6 Generative AI Copilots and Autonomous CRM Capabilities

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership and Customization

- 4.3.2 Data-privacy and Compliance Complexities

- 4.3.3 Vendor Lock-in Limiting Interoperability

- 4.3.4 Ethical Risks and Hallucination in AI-generated Customer Interactions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Sales Force Automation Platforms

- 5.1.1.2 Marketing Automation Platforms

- 5.1.1.3 Customer Service and Support Suites

- 5.1.1.4 Customer Data Platforms

- 5.1.1.5 Digital Commerce Engines

- 5.1.1.6 Analytics and Insights Tools

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Consulting

- 5.1.2.3 Training and Support

- 5.1.2.4 Managed Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.1.1 Public Cloud

- 5.2.1.2 Private Cloud

- 5.2.1.3 Multi-cloud

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.2.1 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Application

- 5.4.1 Sales Force Automation

- 5.4.2 Marketing Automation

- 5.4.3 Customer Service and Support

- 5.4.4 Digital Commerce

- 5.4.5 Analytics and Insights

- 5.4.6 Revenue Operations (RevOps)

- 5.4.7 Partner Relationship Management

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Retail and E-Commerce

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 IT and Telecom

- 5.5.5 Manufacturing

- 5.5.6 Media and Entertainment

- 5.5.7 Professional Services

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Adobe Inc.

- 6.4.6 HubSpot, Inc.

- 6.4.7 Zoho Corporation Pvt. Ltd.

- 6.4.8 Zendesk, Inc.

- 6.4.9 Freshworks Inc.

- 6.4.10 SugarCRM Inc.

- 6.4.11 Pipedrive Inc.

- 6.4.12 Insightly, Inc.

- 6.4.13 Copper CRM, Inc.

- 6.4.14 monday.com Ltd.

- 6.4.15 Keap Inc. (Infusionsoft)

- 6.4.16 The Sage Group plc

- 6.4.17 Infor, Inc.

- 6.4.18 International Business Machines Corporation

- 6.4.19 ServiceNow, Inc.

- 6.4.20 Pegasystems Inc.

- 6.4.21 NICE Ltd.

- 6.4.22 Genesys Telecommunications Laboratories, Inc.

- 6.4.23 Creatio EMEA Ltd.

- 6.4.24 Bitrix24 Ltd.

- 6.4.25 VTiger CRM, Inc.

- 6.4.26 Epicor Software Corporation

- 6.4.27 Aptean, Inc.

- 6.4.28 Intercom, Inc.

- 6.4.29 Gainsight, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment