PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072674

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072674

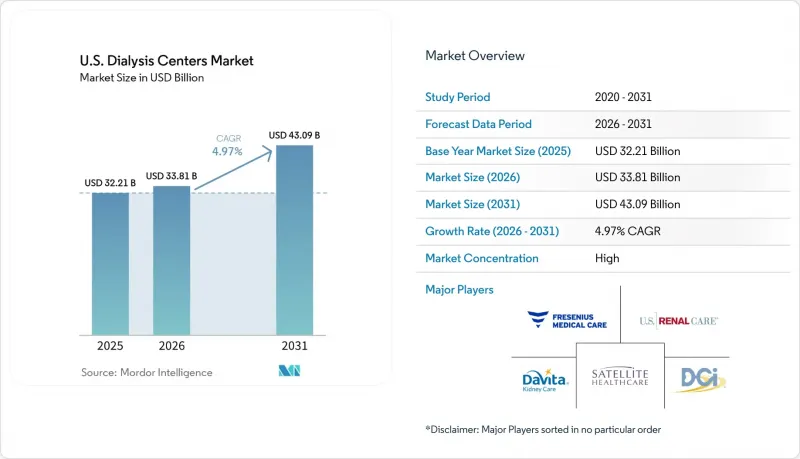

U.S. Dialysis Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. dialysis centers market size is projected to expand from USD 32.21 billion in 2025 and USD 33.81 billion in 2026 to USD 43.09 billion by 2031, registering a CAGR of 4.97% between 2026 to 2031.

This report is Segmented by Modality (In-Center, In-Home, SNF-Based), Dialysis Type (Hemodialysis, Peritoneal Dialysis), and Facility Type (Dialysis Chains, Independent Facilities, Hospital-Based). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Dialysis Centers Market Trends and Insights

Rising ESKD Prevalence from Diabetes, Hypertension, and Related Causes

The United States dialysis centers market continues to grow, driven by an increasing patient base. The ESKD population has risen steadily in the early 2020s, with diabetes, hypertension, and chronic kidney disease remaining significant contributors. Approximately 37 million adults in the United States, or 1 in 7, live with chronic kidney disease, with many undiagnosed until advanced stages. Incident ESKD cases increased by 31.3% between 2002 and 2022, highlighting a widening demand base. An aging treated population and limited transplant eligibility further sustain the market's growth.

Durable Medicare-funded Treatment Demand Base

The United States dialysis centers market benefits from Medicare's ESKD coverage, ensuring a stable payment foundation. CMS projects nearly USD 6.9 billion in payments to 7,600 ESRD facilities in CY 2026, up from USD 6.6 billion to 7,700 facilities in 2025. The proposed CY 2026 base rate of USD 281.06 per treatment, reflecting a 1.9% market basket update, provides payment stability. This model supports care continuity, keeps facilities operational, and maintains demand even during economic challenges.

Staffing Scarcity and Wage Inflation

Staffing shortages are a critical challenge in the United States dialysis centers market, particularly in areas struggling to recruit nurses, technicians, and social workers. CMS regulations require a registered nurse to be present during dialysis, turning staffing gaps into compliance risks. Providers face rising wage demands, shift differentials, agency reliance, and burnout, while payment updates fail to match labor cost pressures. To address this, providers like U.S. Renal Care are building internal talent pipelines, such as their 2025 program to train nephrology nurses. Rural and smaller markets are most affected, limiting the ability to expand or stabilize treatment capacity.

Other drivers and restraints analyzed in the detailed report include:

- Home Dialysis Expansion by Leading Center Operators

- Medicare Advantage and Integrated Kidney-Care Adoption

- Government-heavy Payer Mix and Reimbursement Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, in-center dialysis dominated the United States dialysis centers market, capturing 77.89% of the revenue. This reflects the model's reliance on fixed clinics, scheduled chair capacities, and established workflows. In-home dialysis, projected to grow at a 7.00% CAGR through 2031, is the fastest-growing modality, supported by Medicare policy changes that ease financial burdens for providers expanding home programs. While clinic demand remains strong, home care is reshaping the care model with a focus on patient education, remote oversight, and supply logistics.

The in-center model retains advantages for patients needing close supervision or transportation support. Meanwhile, SNF-based dialysis serves as a transitional setting for frail patients, reducing hospital readmissions by 15%, as highlighted by DaVita. This diversification enhances the delivery capacity of the United States dialysis centers market.

Complete Report Scope:

- By Modality

- In-center

- In-Home

- SNF-based

- Dialysis Type

- Hemodialysis

- Peritoneal Dialysis

- By Facility Type

- Dialysis Chains

- Independent Facilities

- Hospital-based

List of Companies Covered in this Report:

- American Dialysis Centers

- American Renal Care

- Arizona Kidney Disease & Hypertension Centers, Ltd.

- Atlantic Dialysis Management Services, LLC

- Carolina Nephrology, PA

- Centers Health Care

- Concerto Renal Services

- DaVita

- Dialysis Care Center, LLC

- Dialysis Clinic, Inc.

- Dialyze Direct, LLC

- Fresenius Medical Care AG

- Home Dialysis Therapies of San Diego

- Innovative Renal Care, LLC

- Northwest Kidney Centers

- Premier Dialysis

- Rendevor Dialysis

- Satellite Healthcare, Inc.

- The Rogosin Institute

- U.S. Renal Care, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ESKD Prevalence from Diabetes, Hypertension, And Aging

- 4.2.2 Durable Medicare-Funded Treatment Demand Base

- 4.2.3 Home Dialysis Expansion by Leading Center Operators

- 4.2.4 Medicare Advantage and Integrated Kidney-Care Adoption

- 4.2.5 High-Volume Hemodiafiltration Rollout in U.S. Clinics

- 4.2.6 AKI Home-Dialysis Billing Expansion

- 4.3 Market Restraints

- 4.3.1 Staffing Scarcity and Wage Inflation

- 4.3.2 Government-Heavy Payer Mix and Reimbursement Pressure

- 4.3.3 ETC Model Termination Weakens Home-Dialysis Catalyst

- 4.3.4 Oral-Only Phosphate-Binder Bundling Pressure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 In-center

- 5.1.2 In-Home

- 5.1.3 SNF-based

- 5.2 Dialysis Type

- 5.2.1 Hemodialysis

- 5.2.2 Peritoneal Dialysis

- 5.3 By Facility Type

- 5.3.1 Dialysis Chains

- 5.3.2 Independent Facilities

- 5.3.3 Hospital-based

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 American Dialysis Centers

- 6.3.2 American Renal Care

- 6.3.3 Arizona Kidney Disease & Hypertension Centers, Ltd.

- 6.3.4 Atlantic Dialysis Management Services, LLC

- 6.3.5 Carolina Nephrology, PA

- 6.3.6 Centers Health Care

- 6.3.7 Concerto Renal Services

- 6.3.8 DaVita Inc.

- 6.3.9 Dialysis Care Center, LLC

- 6.3.10 Dialysis Clinic, Inc.

- 6.3.11 Dialyze Direct, LLC

- 6.3.12 Fresenius Medical Care AG

- 6.3.13 Home Dialysis Therapies of San Diego

- 6.3.14 Innovative Renal Care, LLC

- 6.3.15 Northwest Kidney Centers

- 6.3.16 Premier Dialysis

- 6.3.17 Rendevor Dialysis

- 6.3.18 Satellite Healthcare, Inc.

- 6.3.19 The Rogosin Institute

- 6.3.20 U.S. Renal Care, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment