PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072681

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072681

HR Knowledge Base And Self-Service Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

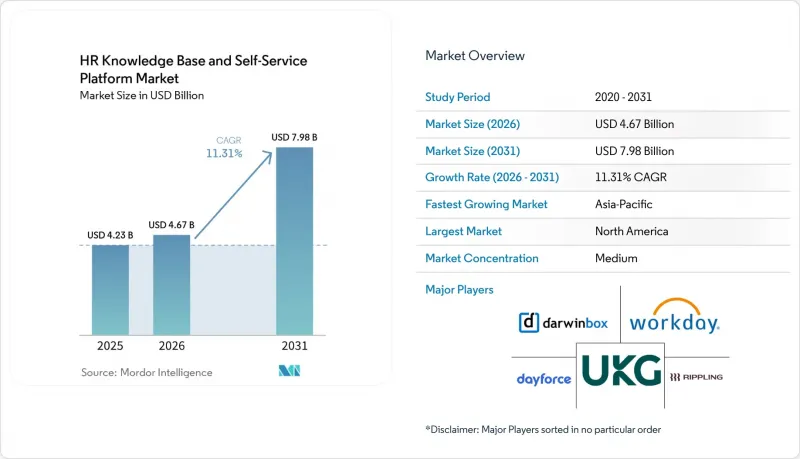

According to Mordor Intelligence, the HR knowledge base and self-service platform market size was valued at USD 4.23 billion in 2025 and is forecast to reach USD 7.98 billion by 2031, growing at a CAGR of 11.31% over 2026-2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Functionality (Knowledge Management, and More), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Global HR Knowledge Base And Self-Service Platform Market Trends and Insights

AI-Enabled HR Service Delivery Modernization

AI has shifted from being an optional feature to a core requirement in HR knowledge bases and self-service platforms. Enterprises now expect these systems to resolve complex HR queries while staying anchored to approved policy content. Workday's March 2026 rollout of Sana introduced a self-service agent with over 300 HR and finance skills, and one customer reported 90% user adoption within 40 days while retiring 400 unsanctioned AI licenses. This illustrates why governed platforms are replacing unapproved tools in HR service environments. Buyers are no longer focused only on ticket deflection; they are also testing whether a system can preserve a single source of policy truth across thousands of employee interactions. Vendors that ground retrieval in company-specific HR content are gaining an edge, since generic models without organizational context are harder to trust in regulated workflows.

Need For 24-7 Employee Self-Service Across Hybrid Workforces

Hybrid work has permanently changed when and how employees seek HR support in the HR knowledge base and self-service platform market. Questions now come from different time zones, devices, and worker types, and that pattern does not fit the design of older HR help desks. Microsoft's Employee Self-Service Agent has already demonstrated enterprise-scale viability, serving hundreds of thousands of employees and vendors across more than 100 countries through a single conversational interface. Mature deployments handle a large share of routine HR questions without human support, but adoption often stalls when knowledge content is incomplete or outdated. This shifts attention from portal access alone to content quality, freshness, and guided action completion. Platforms that combine proactive notifications, contextual retrieval, and step-by-step workflow support are performing better than passive portals built around static search.

Sensitive Employee Data Privacy And Explainability Requirements

Privacy and explainability rules are slowing parts of the HR knowledge base and self-service platform market, especially for employers handling sensitive employee records. These platforms process compensation data, leave information, performance history, disciplinary records, and immigration status, which raises the compliance bar. Explanation duties for automated decision-making remain a live issue in employment use cases, and the EU AI Act imposes documentation requirements on providers and deployers of high-risk systems, which can delay procurement when the documentation chain is incomplete. This burden is harder for mid-market buyers to absorb because they often lack dedicated privacy and legal teams. Vendors that ship explainability dashboards, audit logs, and compliant consent workflows as standard features are better positioned in regulated buying cycles.

Other drivers and restraints analyzed in the detailed report include:

- Cloud HR Suite Consolidation and Lower Total Cost of Ownership

- Rising Compliance Complexity Across Multi-Country HR Policies

- Legacy HRIS, Payroll, And Identity Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based platforms accounted for 68.41% of the HR knowledge base and self-service platform market size in 2025, making cloud the clear mainstream deployment choice. The segment benefited from SaaS pricing that can rise or fall with headcount, which is important for employers managing seasonal, global, or project-based workforces. It also benefited from the need for continuous model tuning and content updates, since cloud-native environments can push those changes more easily than on-premises systems. In the HR knowledge base and self-service platform market, this has made cloud the default option for buyers who want faster releases and lower day-to-day infrastructure effort. Large organizations in information technology and telecom, retail, and financial services accelerated cloud moves in 2024 and 2025 because AI-enabled search, natural language query resolution, and contextual policy retrieval are difficult to support in older deployments without major custom work.

Hybrid is the fastest-growing deployment option through 2031 because some employers still need tighter control over where sensitive employee data sits. This is especially relevant in regulated settings where data residency rules or internal security policies make full SaaS migration harder to approve. Vendors are responding with federated models that keep sensitive records in private or on-premises environments while letting retrieval and user interaction run through managed cloud layers. That approach helps preserve modern user experience without forcing a full infrastructure replacement at the start of the project. On-premises remains present in high-security public sector and defense settings, but its role is narrowing as the HR knowledge base and self-service platform market places more value on update speed, audit readiness, and lower maintenance effort.

Large enterprises held the largest share of revenue in 2025 because they had the scale to justify replacing or augmenting HR shared services with self-service platforms. In many of these organizations, HR teams manage thousands of monthly employee questions, so even modest automation can create meaningful savings in staff time and response quality. The HR knowledge base and self-service platform market has therefore seen large buyers favor broader platform contracts that combine knowledge management, virtual agents, service workflows, and analytics. Those deals often favor vendors that can deliver integrated capabilities on top of existing HCM systems. Large employers also tend to have stronger governance, change management, and compliance resources, which makes it easier to move from pilot programs to enterprise production use.

Small and medium-sized enterprises are projected to grow at a 15.82% CAGR from 2026 to 2031, which makes them the fastest-growing customer tier. This shift reflects lower implementation burdens, as cloud-native tools reduce the cost and effort that once kept advanced deployments out of reach for firms with fewer than 5,000 employees. Tiered packaging is also helping because buyers can start with knowledge management or employee self-service without replacing an entire HCM stack. In the HR knowledge base and self-service platform industry, that modular model is widening adoption among firms with 200 to 2,000 employees and among smaller regulated employers that need controlled HR content without enterprise-scale complexity.

Complete Report Scope:

- By Deployment Model

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Functionality

- Knowledge Management

- Knowledge Discovery and Search

- Employee Self-Service

- Conversational AI and Virtual Agents

- Service Automation

- Analytics and Governance

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 41.23% of the HR knowledge base and self-service platform market share in 2025, giving the region the largest global position. The region benefited from high enterprise SaaS penetration, larger HR shared services budgets, and faster early adoption of AI-assisted employee experience tools. The United States remained the anchor market because large employers there have been quicker to connect self-service with broader HCM and workflow modernization programs. The scale and maturity of enterprise workforce software demand, closely tied to North American vendor ecosystems, mean competition centers less on basic portal functions and more on AI quality, governance depth, and integration breadth.

Europe remains a major region in the HR knowledge base and self-service platform market, but regulatory and consultation rules more heavily shape it. GDPR, the EU AI Act, and national labor frameworks all influence how quickly employers can move from testing to scaled production use. Germany and France are especially important because works council consultation and employee oversight rules can add months to deployment timelines for HR AI systems. That has increased the appeal of vendors that can show stronger documentation, explainability, and local policy controls from the start.

Asia-Pacific is projected to grow at a 15.63% CAGR through 2031, the fastest regional pace in the HR knowledge base and self-service platform market. Demand is strong for mobile-first, multilingual support where deskless manufacturing, logistics, and retail workforces need it. Multilingual mobile-first HR systems in India have shown adoption improvements of more than 70% compared with English-only systems, highlighting the importance of language coverage in high-growth settings. South America, the Middle East, and Africa are at earlier adoption stages, but vendor expansion into hubs such as Mexico City shows that providers are preparing for broader enterprise demand across Mexico, Central America, and South America.

- Workday, Inc.

- UKG Inc.

- Dayforce Corporation

- Rippling, Inc.

- Bamboo HR LLC

- Personio SE and Co. KG

- Hi Bob Ltd.

- Darwinbox Digital Solutions Pte. Ltd.

- Everyday Software, S.L.

- Connecteam Ltd.

- Leena AI, Inc.

- Simpplr, Inc.

- Staffbase GmbH

- ITacit Inc.

- Trainual, Inc.

- Tettra, Inc.

- Axero Solutions, LLC

- Korra AI LTD.

- Public Sector Analytics Limited

- Humaans Software UK LTD

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 AI-Enabled HR Service Delivery Modernization

- 4.3.2 Need for 24-7 Employee Self-Service Across Hybrid Workforces

- 4.3.3 Cloud HR Suite Consolidation and Lower Total Cost of Ownership

- 4.3.4 Rising Compliance Complexity Across Multi-Country HR Policies

- 4.3.5 Shadow AI Governance Driving Demand for Controlled HR Knowledge Layers

- 4.3.6 Deskless and Multilingual Workforce Support Expanding Addressable Use Cases

- 4.4 Market Restraints

- 4.4.1 Sensitive Employee Data Privacy and Explainability Requirements

- 4.4.2 Legacy HRIS, Payroll, and Identity Integration Complexity

- 4.4.3 Works Council and AI Employment Law Review Slowing Production Rollouts

- 4.4.4 Low Content Governance Maturity and Over-Permissioned Repositories

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Enterprises

- 5.3 By Functionality

- 5.3.1 Knowledge Management

- 5.3.2 Knowledge Discovery and Search

- 5.3.3 Employee Self-Service

- 5.3.4 Conversational AI and Virtual Agents

- 5.3.5 Service Automation

- 5.3.6 Analytics and Governance

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 UKG Inc.

- 6.4.3 Dayforce Corporation

- 6.4.4 Rippling, Inc.

- 6.4.5 Bamboo HR LLC

- 6.4.6 Personio SE and Co. KG

- 6.4.7 Hi Bob Ltd.

- 6.4.8 Darwinbox Digital Solutions Pte. Ltd.

- 6.4.9 Everyday Software, S.L.

- 6.4.10 Connecteam Ltd.

- 6.4.11 Leena AI, Inc.

- 6.4.12 Simpplr, Inc.

- 6.4.13 Staffbase GmbH

- 6.4.14 iTacit Inc.

- 6.4.15 Trainual, Inc.

- 6.4.16 Tettra, Inc.

- 6.4.17 Axero Solutions, LLC

- 6.4.18 Korra AI LTD.

- 6.4.19 Public Sector Analytics Limited

- 6.4.20 Humaans Software UK LTD

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment