PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072713

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072713

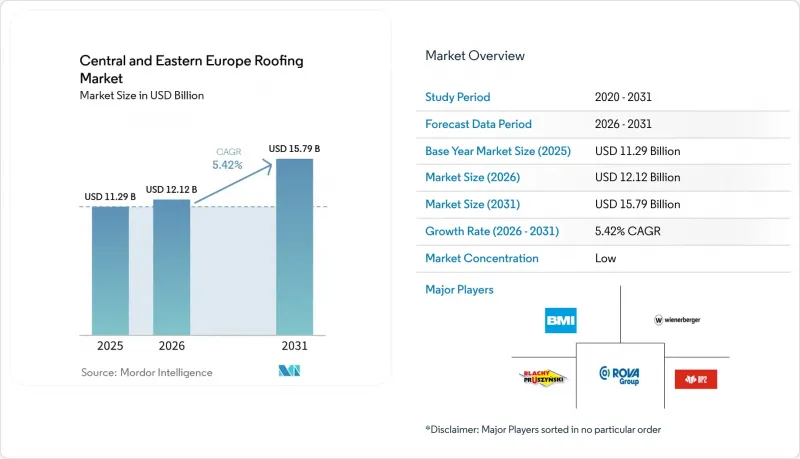

Central and Eastern Europe Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the central and eastern europe roofing market size is projected to be USD 11.29 billion in 2025, USD 12.12 billion in 2026, and reach USD 15.79 billion by 2031, growing at a CAGR of 5.42% from 2026 to 2031.

This report is Segmented by Material Type (Asphalt Shingles, Clay & Concrete Tiles, Metal Roofing, Bituminous / Modified Bitumen Membranes, and More), Construction Type (New Construction, Reroofing), Application (Residential, and More), and Geography (Poland, Romania, Czech Republic, Hungary, and Rest of Central and Eastern Europe). The Market Forecasts are Provided in Terms of Value (USD).

Central and Eastern Europe Roofing Market Trends and Insights

EPBD Renovation Mandates Create a Durable, Policy-Anchored Demand Pipeline

The Central and Eastern Europe roofing market is being reshaped by the recast of the Energy Performance of Buildings Directive (EPBD), which is one of the strongest policy drivers influencing roof renovation decisions over the forecast period. The directive requires renovating the 16% worst-performing non-residential buildings by 2030 and 26% by 2033, while also targeting a 16% reduction in average primary energy use in residential buildings by 2030. This matters more in Central and Eastern Europe because more than 50% of the building stock does not meet current performance expectations, and much of the residential base predates 1990. In practice, many properties will not be able to comply solely through minor repairs, so roof replacement, insulation upgrades, and related envelope work will increasingly be specified together. That bundling effect makes roofing demand less discretionary and more tied to mandatory compliance schedules, which improves visibility for suppliers and installers serving the Central and Eastern Europe roofing market. It also raises the value of technically certified systems, because buyers now need proof that the finished roof meets energy performance targets rather than just restoring weather protection.

Thermal Modernization Subsidy Programs Activate Household Reroofing at Scale

Household subsidy programs are expanding the addressable base for renovation work and making the Central and Eastern European roofing market more resilient to short-term price pressure. Poland's Czyste Powietrze program secured PLN 10 billion (USD 2.5 billion) from the European Union (EU) Modernization Fund in March 2025, including support for roof insulation as part of wider household energy upgrades. In the Czech Republic, the New Green Savings Programme directly supports roof and ceiling insulation for family houses and apartment buildings, which helps convert policy demand into actual roof replacement activity. The effect is especially strong at the lower-income end, where high grant coverage reduces the sensitivity of repair decisions to movements in metal or bitumen prices. That keeps reroofing pipelines more stable than they would be in a purely unsubsidized consumer market, particularly in countries with older housing stock and low heating efficiency. As a result, the Central and Eastern Europe roofing market is seeing more projects where insulation, covering replacement, and future solar compatibility are considered in a single homeowner decision rather than in separate phases.

Volatile Steel, Bitumen, and Energy Input Costs

Steel and bitumen price volatility remains a direct headwind for the Central and Eastern Europe roofing market, particularly in product groups that depend on imported feedstock or energy-intensive production. EUROMETAL reported late May 2026 hot-rolled coil prices at EUR 700 to EUR 770 per tonne, equivalent to USD 756 to USD 831.6 per tonne, while the July 2026 safeguard changes are expected to keep pricing for steel-based products uncertain. That uncertainty affects metal roofing manufacturers, fabricators, and distributors because quoting windows and procurement timing become harder to manage. Bitumen-related pressure also matters for flat roofing systems, as disruptions in raw material availability can delay project schedules and compress margins. Energy costs add another layer of strain on clay tile, membrane, and other manufactured roofing products that depend on stable plant economics. The burden falls more heavily on smaller regional players, which may accelerate share gains for larger businesses with broader sourcing options and stronger balance sheets.

Other drivers and restraints analyzed in the detailed report include:

- Nearshoring Industrial Construction Sustains Single-Ply and Panel Roofing Demand

- Metal Roofing Substitution in Renovation for Lightweight, Faster Installation

- Skilled Roofer Shortages and Ageing Installer Base

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clay & Concrete Tiles held a 36.20% market share in 2025, making them the largest material category in the Central and Eastern Europe roofing market. This leading position reflects long-established preferences for pitched roofs across Poland, Hungary, and the Czech Republic, where tile roofs remain closely tied to mainstream residential construction. The category also benefits from replacement demand, as many renovated homes were originally built with pitched roofs that are well-suited to tile systems. In practical terms, that installed base keeps tile relevant even as performance expectations rise. End-2025 investment also showed that manufacturers still view this category as strategically important, with Wienerberger commissioning a new concrete roof tile plant in Hungary with an annual capacity of 3 million square meters and an investment of EUR 30 million (USD 32.4 million). The decision supports the view that scale, product continuity, and regional supply remain important in the Central and Eastern Europe roofing industry.

Metal Roofing is the fastest-growing material segment, with the Central and Eastern Europe roofing market size for this category projected to expand at a 6.40% CAGR from 2026 to 2031. Its growth is tied to two practical advantages that matter more each year: lighter structural loading on older buildings and faster installation under tight labor conditions. That makes metal especially attractive in renovation projects where legacy roof frames cannot easily support heavier replacement systems. It also fits projects where installers need to complete more area in fewer site days because certified labor is limited. Bituminous and modified bitumen membranes remain essential for flat commercial roofs, although cost and supply volatility can complicate procurement planning. Single-ply membranes are gaining ground in large industrial applications due to their compatibility with drainage design and rooftop solar integration. At the same time, asphalt shingles retain a niche role, and wood remains concentrated in heritage and premium uses. Across the Central and Eastern Europe roofing industry, the shift toward certified system solutions is becoming clearer as owners place more value on compliance, service life, and integration than on low-end material substitution alone.

Complete Report Scope:

- By Material Type

- Asphalt Shingles

- Clay & Concrete Tiles

- Metal Roofing

- Bituminous / Modified Bitumen Membranes

- Single-Ply Membranes (TPO, EPDM, and PVC)

- Wood

- Others

- By Construction Type

- New Construction

- Reroofing and Replacement

- By Application

- Residential

- Commercial

- Industrial

- Institutional

- Others

- By Geography

- Poland

- Romania

- Czech Republic

- Hungary

- Rest of Central and Eastern Europe

List of Companies Covered in this Report:

- BMI Group

- Wienerberger

- Pruszynski

- BP2

- ROVA Group

- Lindab

- Ruukki Construction

- Kingspan Group

- Soprema

- Bilka

- Metigla

- Wetterbest

- Balex Metal

- swissporTON

- Terran Group

- Onduline Group

- PREFA Aluminiumprodukte

- Gerard Roofing System

- Nelskamp

- Bauder

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EPBD-Led Deep Renovation of Worst-Performing Buildings

- 4.2.2 Thermal Modernization Subsidies Supporting Reroofing Demand

- 4.2.3 Nearshoring-Led Warehouse and Light-Industrial Roof Build-Out

- 4.2.4 Metal Roofing Substitution in Renovation for Lightweight, Faster Installation

- 4.2.5 Solar-Ready and Rooftop PV Permit Triggers Increasing Roof-System Upgrades

- 4.2.6 Hail and Convective Storm Damage Accelerating Reroofing Cycles

- 4.3 Market Restraints

- 4.3.1 Volatile Steel, Bitumen, and Energy Input Costs

- 4.3.2 Skilled Roofer Shortages and Ageing Installer Base

- 4.3.3 Renovation Underperformance and Weak Building-Level Execution Controls

- 4.3.4 Fragmented Installer Quality and Uneven Code Enforcement

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Trend and Impacts of Roofing Replacements

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 Asphalt Shingles

- 5.1.2 Clay & Concrete Tiles

- 5.1.3 Metal Roofing

- 5.1.4 Bituminous / Modified Bitumen Membranes

- 5.1.5 Single-Ply Membranes (TPO, EPDM, and PVC)

- 5.1.6 Wood

- 5.1.7 Others

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Reroofing and Replacement

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 Poland

- 5.4.2 Romania

- 5.4.3 Czech Republic

- 5.4.4 Hungary

- 5.4.5 Rest of Central and Eastern Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BMI Group

- 6.4.2 Wienerberger

- 6.4.3 Pruszynski

- 6.4.4 BP2

- 6.4.5 ROVA Group

- 6.4.6 Lindab

- 6.4.7 Ruukki Construction

- 6.4.8 Kingspan Group

- 6.4.9 Soprema

- 6.4.10 Bilka

- 6.4.11 Metigla

- 6.4.12 Wetterbest

- 6.4.13 Balex Metal

- 6.4.14 swissporTON

- 6.4.15 Terran Group

- 6.4.16 Onduline Group

- 6.4.17 PREFA Aluminiumprodukte

- 6.4.18 Gerard Roofing System

- 6.4.19 Nelskamp

- 6.4.20 Bauder

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment