PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072751

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072751

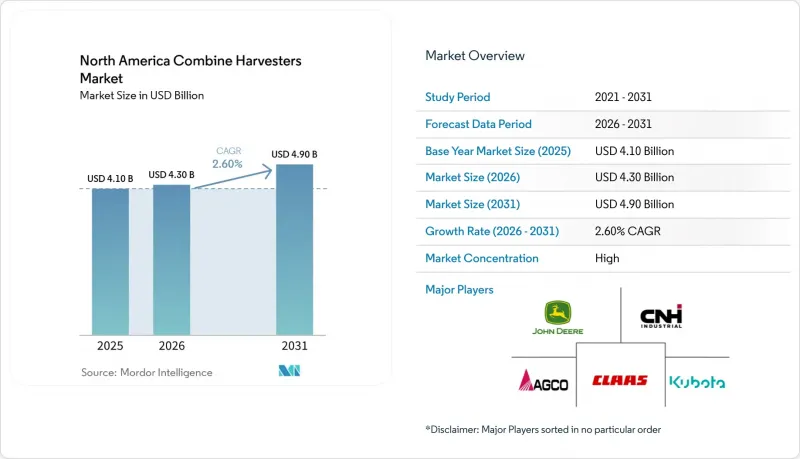

North America Combine Harvesters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america combine harvesters market size is projected to expand from USD 4.10 billion in 2025 and USD 4.30 billion in 2026 to USD 4.90 billion by 2031, registering a CAGR of 2.60% between 2026 and 2031.

This report is Segmented by Product Type (Conventional Straw-Walker Combines, Rotary Combines, Hybrid Combines, and Tracked Combines), by Power Class (Below 200 HP, 200 To 300 HP, 300 To 400 HP, and Above 400 HP), by Country (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

North America Combine Harvesters Market Trends and Insights

Rising Labor Costs and Labor Shortages

A decline in agricultural employment is accelerating the adoption of full mechanization across large grain farms, as indicated by World Bank data. Employment in agriculture decreased to 1.52% in 2025, compared to 1.56% in 2024. In 2024, Deere & Company introduced the S7 Series combines featuring Predictive Ground Speed Automation and automated harvest settings to improve harvesting consistency, productivity, and ease of operation. Regions such as North Dakota, Montana, Saskatchewan, and Alberta are experiencing significant labor shortages despite high hourly wages. This has led to wage inflation, enhancing the return on investment for autonomous and semi-autonomous harvesters, thereby reducing labor demand. Leasing rates for combines equipped with advanced automation are increasing, reflecting a willingness to invest in features that minimize workforce requirements. Consequently, labor constraints are driving premium pricing and supporting the ongoing shift toward advanced technology in the North America combine harvesters market.

Precision-Agriculture Adoption and Integration

Combines have evolved into rolling data centers that stream location-tagged yield, moisture, and protein metrics to cloud dashboards. Deere's 2025 SmartPan integration delivers grain-quality analytics before the truck reaches the elevator, locking operators into its ecosystem. Regulatory drivers such as the Environmental Protection Agency (EPA) nutrient-management rules in the Chesapeake Bay and Great Lakes regions heighten demand for traceable agronomic data. Embedded analytics also support variable-rate fertilizer planning, closing the loop between harvest and input application. These synergies intensify equipment stickiness, raise switching costs, and underpin long-run growth for the North America combine harvesters market.

High Upfront Capital Costs for Advanced Combines

High upfront capital costs for advanced combine harvesters significantly constrain the North America combine harvesters market, particularly impacting small and medium-sized farms, which constitute 90% of farming operations in the United States. AGCO Corporation reported approximately USD 2.5 billion in net sales in Q3 2024, reflecting a year-over-year decline amid weaker agricultural equipment demand as growers delayed machinery purchases because of tighter farm margins. Smaller operators increasingly favor used units or seasonal rentals, lengthening upgrade cycles. In Mexico, the average farm size is below 500 acres, rendering new machines uneconomical without cooperative models that are still nascent. This trend underscores the growing importance of alternative ownership models, such as equipment sharing and leasing, to address the economic constraints faced by smaller farming operations in the region.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies and Preferential Financing

- Original Equipment Manufacturer (OEM) Subscription-Based Autonomous Software Upgrades

- Rural Connectivity Gaps Limiting Real-Time Telematics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary combines led the largest segment, with 65% of the North America combine harvesters market share in 2025, owing to superior throughput in high-moisture corn. Conventional straw-walker models persist in drier wheat belts, but their share erodes as acreage tilts toward corn and soybeans. Hybrid architectures, championed by AGCO's Gleaner line, capture a small niche among custom harvesters that need multi-crop flexibility. Rotary dominance will remain intact, but the competitive narrative is shifting toward platform versatility, with Original Equipment Manufacturer (OEM) adding quick-attach axle kits that let growers convert between wheels and tracks in under four hours.

Tracked combines are the fastest-growing, forecast to post the fastest 7.8% CAGR through 2026 to 2031, outpacing all other product types as wetter autumns shorten harvest windows and soil-compaction risk climbs. Rising demand for tracks comes primarily from North Dakota, Minnesota, and eastern Canada, where clay soils saturate quickly. Larger contact patches lower ground pressure, preserving soil tilth for spring planting. Operators also value higher resale prices for tracked units, narrowing total cost-of-ownership gaps with wheeled alternatives.

Complete Report Scope:

- By Product Type

- Conventional Straw-Walker Combines

- Rotary Combines

- Hybrid Combines

- Tracked Combines

- By Power Class

- Below 200 HP

- 200 to 300 HP

- 300 to 400 HP

- Above 400 HP

- By Country

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- Deere & Company

- Case IH Agriculture

- CNH Industrial N.V.

- AGCO Corporation

- CLAAS KGaA mbH

- Kubota Corporation

- Rostselmash Joint-Stock Co.

- Sampo Rosenlew Oy

- Yanmar Holdings Co., Ltd.

- Same Deutz-Fahr Italia S.p.A.

- TRIBINE Harvester LLC

- Zoomlion Heavy Industry Science & Technology Co., Ltd.

- Oxbo International Corporation

- Preet Tractors Private Ltd.

- ISEKI & Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising labor costs and labor shortages

- 4.2.2 Precision-agriculture adoption and integration

- 4.2.3 Government subsidies and preferential financing

- 4.2.4 Accelerated fleet-replacement cycles on large farms

- 4.2.5 Original Equipment Manufacturer (OEM)subscription-based autonomous software upgrades

- 4.2.6 Interoperability standards for grain cart-combine automation

- 4.3 Market Restraints

- 4.3.1 High upfront capital costs for advanced combines

- 4.3.2 Commodity-price volatility impacting farm cash flow

- 4.3.3 Semiconductor and hydraulic component supply-chain constraints

- 4.3.4 Rural connectivity gaps limiting real-time telematics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Conventional Straw-Walker Combines

- 5.1.2 Rotary Combines

- 5.1.3 Hybrid Combines

- 5.1.4 Tracked Combines

- 5.2 By Power Class

- 5.2.1 Below 200 HP

- 5.2.2 200 to 300 HP

- 5.2.3 300 to 400 HP

- 5.2.4 Above 400 HP

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Case IH Agriculture

- 6.4.3 CNH Industrial N.V.

- 6.4.4 AGCO Corporation

- 6.4.5 CLAAS KGaA mbH

- 6.4.6 Kubota Corporation

- 6.4.7 Rostselmash Joint-Stock Co.

- 6.4.8 Sampo Rosenlew Oy

- 6.4.9 Yanmar Holdings Co., Ltd.

- 6.4.10 Same Deutz-Fahr Italia S.p.A.

- 6.4.11 TRIBINE Harvester LLC

- 6.4.12 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 6.4.13 Oxbo International Corporation

- 6.4.14 Preet Tractors Private Ltd.

- 6.4.15 ISEKI & Co., Ltd.

7 Market Opportunities and Future Outlook