PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072788

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072788

US-Mexico Cross-Border Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

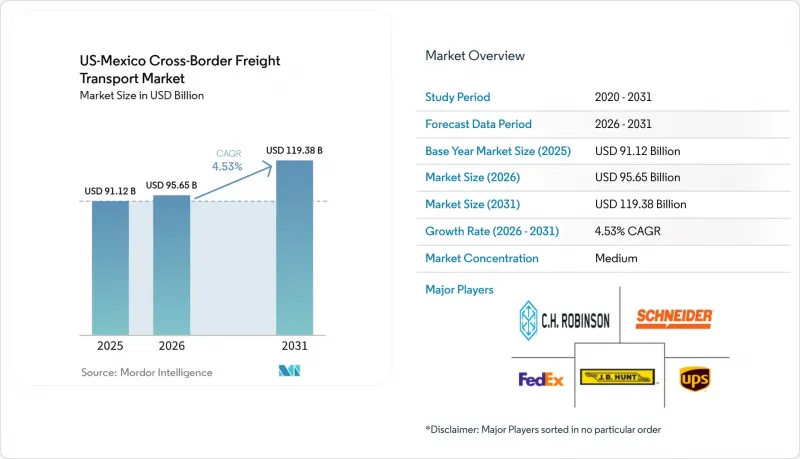

According to Mordor Intelligence, the US-Mexico cross-border freight transport market size is projected to expand from USD 91.12 billion in 2025 and USD 95.65 billion in 2026 to USD 119.38 billion by 2031, registering a CAGR of 4.53% between 2026 and 2031.

Capacity additions, nearshoring investments, and e-commerce parcel density are broadening the service mix and boosting pricing power for carriers that can guarantee reliable door-to-door delivery. This report is Segmented by Mode of Transportation (Road Freight Transport [Full Truckload, Less-Than-Truckload], Rail Freight Transport), by End-User Industry (Agriculture, Fishing, and Forestry, Construction, Healthcare and Pharmaceutical, and More), and by Cross-Border Lane (United States To Mexico, Mexico To United States). The Market Forecasts are Provided in Terms of Value (USD).

US-Mexico Cross-Border Freight Transport Market Trends and Insights

Nearshoring of electronics and machinery supply chains

Original-equipment manufacturers are relocating final assembly from Asia to Mexico, compressing lead times from 30-45 days to as few as five days. Flex's USD 1 billion investment aims to supply hyperscale cloud clients from hubs like Jalisco and Chihuahua, while Yazaki's USD 66 million wire-harness expansion in Nuevo Leon feeds EV lines for Kia and General Motors. DHL Global Forwarding recorded a 76.2% spike in Mexico-origin electronics exports in October 2025, confirming the sectoral pivot. FTL carriers benefit from higher-value, time-sensitive loads, yet rising shipment frequency also accelerates LTL uptake. Vendor-managed inventory programs inside bonded warehouses cut working capital needs by up to 20%.

USMCA Rules of Origin and Regional Sourcing Incentives

A mandatory 75% regional-value content threshold and labor-value benchmarks of USD 16 per hour deepen supply-chain localization. The United States International Trade Commission notes that while the vast majority of Mexican automotive exports still clear duty-free, the stricter USMCA regulations have marginally reduced the qualification rate compared to the near-total compliance seen under the former NAFTA regime. Kia's USD 600 million EV expansion in Nuevo Leon includes battery-module assembly to meet these stricter thresholds and avoid 2.5% most-favored-nation duties. Tighter verification could raise compliance costs, but the duty-savings dividend continues to outweigh marginal production premiums. Demand therefore gravitates toward cross-border carriers that offer integrated brokerage and documentation support.

Tariff Volatility (Section 122/301) and Policy Uncertainty

The February 2025 proposal for a blanket 25% tariff on Mexican imports, though paused, spurred shipment surges ahead of the possible start date and abrupt order halts afterward, leaving a lingering chill on the market. Section 232 duties on steel and aluminum persist, raising costs for Mexican producers while allowing finished assemblies to travel duty-free under USMCA, distorting sourcing decisions. Furthermore, ongoing friction over the USMCA's automotive rules of origin following the contentious 2023 panel ruling continues to pose the persistent threat of tighter verification and retroactive penalties. Heavy-duty truck tariffs introduced by the US in October 2025 severely cut Mexican exports to the United States within weeks. Ultimately, the looming July 2026 USMCA joint review threatens further structural rule changes, heavily deterring long-horizon capital deployment.

Other drivers and restraints analyzed in the detailed report include:

- High-Frequency Cross-Border E-Commerce Shipments

- Digital Customs Platforms Accelerating Clearances

- Infrastructure Bottlenecks and Congestion at Key Crossings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Road freight accounted for 92.44% of the US-Mexico cross-border freight transport market size in 2025, underscoring its door-to-door flexibility and ability to serve inland manufacturing clusters beyond rail terminals. While Canadian Pacific Kansas City's (CPKC) new twin-track bridge successfully doubled rail capacity in late 2024, inbound northbound truck volumes at Laredo alone still average roughly 8,500 per day to capture incremental nearshoring flows. The US-Mexico cross-border freight transport market size tied to road services is projected to grow at a 4.60% CAGR through 2031 as bonded cross-dock hubs multiply and customs digitization compresses dwell time.

Intermodal partnerships such as J.B.Hunt-BNSF-GMXT's 'Quantum de Mexico' promise one-day faster transits, yet they remain niche relative to ubiquitous trucking. E-commerce parcels, temperature-controlled pharmaceuticals, and machinery spares favor truckload flexibility, sustaining the segment's pricing power. Even with enhanced transcontinental rail capacity now fully online, customer preference for predictable pickup windows keeps road firmly ahead in the medium term.

FTL dominated road freight with a 79.74% US-Mexico cross-border freight transport market share in 2025, reflecting consolidated automotive and capital-goods loads. LTL, though smaller, is forecast to record the highest CAGR of 5.04% to 2031 as e-commerce package density rises and SMEs embrace consolidation programs.

C.H. Robinson's September 2025 service, which aggregates LTL parcels, yields up to 40% in cost savings, highlighting value for shippers moving under the USD 50 Mexican de minimis ceiling. Ryder's 228,000-square-foot Laredo hub dedicates sorting bays to LTL cross-docks, underscoring the modal shift. FTL still retains strategic relevance for automotive original-equipment manufacturers that dispatch complete trailer loads on tight schedules, but even these firms are trialing LTL for aftermarket parts to minimize stocking costs. Consequently, blended networks that can flex between FTL and LTL are well positioned to capture incremental margin.

Complete Report Scope:

- By Mode of Transportation

- Road Freight Transport

- Full Truckload (FTL)

- Less-than-Truckload (LTL)

- Rail Freight Transport

- Road Freight Transport

- By End-User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Distributive Trade (Wholesale and Retail trade)

- Healthcare and Pharmaceutical

- Manufacturing and Automotive

- Oil and Gas, Mining and Quarrying

- Other End-user Industries

- By Cross-Border Lane

- United States to Mexico

- Mexico to United States

List of Companies Covered in this Report:

- C.H. Robinson Worldwide, Inc.

- Schneider National, Inc.

- J.B. Hunt Transport Services, Inc.

- Knight-Swift Transportation Holdings, Inc.

- Landstar System, Inc.

- UPS Supply Chain Solutions (UPS Inc.)

- FedEx Logistics

- DHL Supply Chain & Global Forwarding

- Canadian Pacific Kansas City Ltd. (CPKC)

- Union Pacific Railroad Co.

- BNSF Railway Co.

- Grupo Mexico Transportes (Ferromex)

- Grupo Traxion, S.A.B. de C.V.

- Grupo Transportes Monterrey

- Uber Freight (Transplace)

- XPO, Inc.

- DSV A/S (DB Schenker)

- Ryder System, Inc.

- Trimac Transportation Ltd.

- Maverick Transportation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Nearshoring of Electronics & Machinery Supply Chains

- 4.2.2 USMCA Rules of Origin & Regional Sourcing Incentives

- 4.2.3 Digital Customs Platforms Accelerating Clearances

- 4.2.4 Laredo World Trade Bridge Capacity Expansion

- 4.2.5 High-Frequency Cross-Border E-Commerce Shipments

- 4.2.6 Rapid Growth of Bonded Cross-Dock Hubs In "Twin Triangles" Corridor

- 4.3 Market Restraints

- 4.3.1 Infrastructure Bottlenecks & Congestion at Key Crossings

- 4.3.2 Tariff Volatility (Section 122/301) & Policy Uncertainty

- 4.3.3 Security Risks & Cargo-Theft Corridors in Mexico

- 4.3.4 Cross-Border Driver Shortages & Aging Truck Fleet

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Mode of Transportation

- 5.1.1 Road Freight Transport

- 5.1.1.1 Full Truckload (FTL)

- 5.1.1.2 Less-than-Truckload (LTL)

- 5.1.2 Rail Freight Transport

- 5.1.1 Road Freight Transport

- 5.2 By End-User Industry

- 5.2.1 Agriculture, Fishing, and Forestry

- 5.2.2 Construction

- 5.2.3 Distributive Trade (Wholesale and Retail trade)

- 5.2.4 Healthcare and Pharmaceutical

- 5.2.5 Manufacturing and Automotive

- 5.2.6 Oil and Gas, Mining and Quarrying

- 5.2.7 Other End-user Industries

- 5.3 By Cross-Border Lane

- 5.3.1 United States to Mexico

- 5.3.2 Mexico to United States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market Level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 C.H. Robinson Worldwide, Inc.

- 6.4.2 Schneider National, Inc.

- 6.4.3 J.B. Hunt Transport Services, Inc.

- 6.4.4 Knight-Swift Transportation Holdings, Inc.

- 6.4.5 Landstar System, Inc.

- 6.4.6 UPS Supply Chain Solutions (UPS Inc.)

- 6.4.7 FedEx Logistics

- 6.4.8 DHL Supply Chain & Global Forwarding

- 6.4.9 Canadian Pacific Kansas City Ltd. (CPKC)

- 6.4.10 Union Pacific Railroad Co.

- 6.4.11 BNSF Railway Co.

- 6.4.12 Grupo Mexico Transportes (Ferromex)

- 6.4.13 Grupo Traxion, S.A.B. de C.V.

- 6.4.14 Grupo Transportes Monterrey

- 6.4.15 Uber Freight (Transplace)

- 6.4.16 XPO, Inc.

- 6.4.17 DSV A/S (DB Schenker)

- 6.4.18 Ryder System, Inc.

- 6.4.19 Trimac Transportation Ltd.

- 6.4.20 Maverick Transportation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment