PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072834

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072834

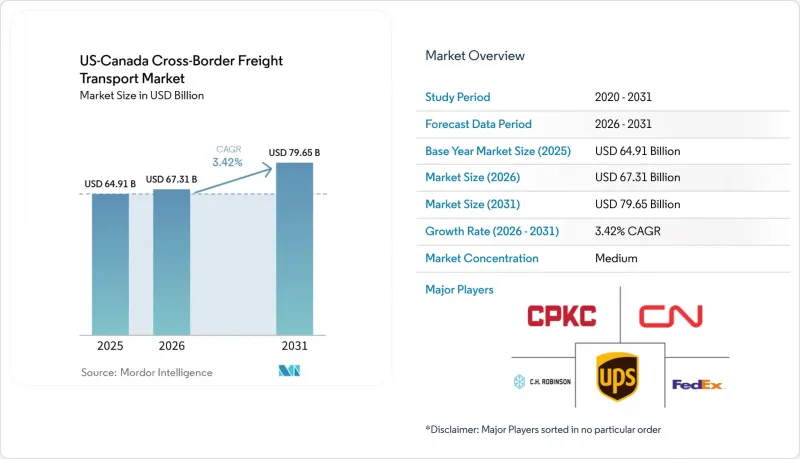

US-Canada Cross-Border Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the US-Canada cross-border freight transport market size is expected to grow from USD 64.91 billion in 2025 to USD 67.31 billion in 2026 and is forecast to reach USD 79.65 billion by 2031 at a 3.42% CAGR over 2026-2031.

Resilient consumer spending in both countries, together with CUSMA-driven tightening of the rule of origin, is keeping freight volumes on an upward trajectory even as supply chain managers redesign networks to cut inventory dwell time. This report is Segmented by Mode of Transportation (Road Freight Transport [Full Truckload, Less-Than-Truckload] Rail Freight Transport), by End-User Industry (Agriculture, Fishing, and Forestry, Construction, Distributive Trade, and More), and by Cross-Border Lane (United States To Canada, and Canada To the United States). The Market Forecasts are Provided in Terms of Value (USD).

US-Canada Cross-Border Freight Transport Market Trends and Insights

OEM Near-Shoring of Automotive Supply Chains

Automakers are relocating part and module production to plants that satisfy CUSMA's 75% regional value content threshold, concentrating freight into higher-volume corridors. In February 2026, General Motors invested USD 46 million to upgrade stamping operations for next-generation gas-powered pickups at its Oshawa, Ontario assembly plant, even as it trimmed shifts at the same facility earlier in the year, showing how re-investment and retrenchment can coexist. Stellantis likewise paused Brampton retooling in 2025 and redirected Jeep Compass production to the United States, shrinking northbound component moves while boosting southbound finished-vehicle hauls. Carriers with contract carriage and drop-and-hook fleets are better positioned to handle the surge-and-slump profile of parts demand, whereas spot-market players struggle to secure backhauls. Hours-of-Service limits imposed by the Federal Motor Carrier Safety Administration (FMCSA) still cap daily driving at 11 hours, making time-buffered relay points along the Ontario-Michigan corridor essential to maintaining just-in-time sequencing. Overall, near-shoring adds variability yet lifts total lane mileage, supporting incremental volume growth through 2031.

"E-Commerce North" Same-Day Delivery Guarantees

Consumer platforms now market two-day or even same-day delivery between major US and Canadian metros, forcing carriers to pre-position inventory in bonded facilities within 30 miles of high-volume crossings. Canada Post's parcel market share had already eroded to 24% by 2024, even prior to its late-year labor disruptions, enabling private integrators such as FedEx and United Parcel Service to absorb volumes and re-optimize hub-and-spoke routes. FedEx integrated its Canada Ground unit into FedEx Express in 2024, eliminating intra-company hand-offs that had inflated northbound transit time by up to a full day. CBP's forthcoming Electronic Truck Manifest mandate, scheduled for June 2026, allows compliant carriers to clear low-value shipments before arrival, compressing dwell time to below 15 minutes. Large integrators with proprietary brokerage systems will capture the lion's share of those gains, widening cost gaps relative to regional LTL providers. The driver pool, already strained, must support additional night-shift and cross-dock operations to uphold 24-hour delivery promises.

Driver Shortages and Hours-of-Service Caps

North America's driver pool is aging out faster than replacements enter, pushing median ages to 47 in the United States and 49 in Canada. FMCSA limits of 11 hours behind the wheel and mandated 10-hour rest breaks effectively shrink daily range on cross-border hauls, forcing carriers to set up relay nodes or deploy two-person teams that raise line-haul cost by as much as 30%. While the double-digit wage hikes of the pandemic era have plateaued, driver compensation remains structurally elevated, and these higher baselines have yet to reverse the overall shortfall. Meanwhile, tighter medical-fitness rules have disqualified a growing share of applicants. Carriers are experimenting with driver-assist systems and automated gear-shifting to ease the workload, but full autonomy remains beyond the forecast horizon. Until recruitment pipelines stabilize, capacity constraints will remain the most immediate ceiling on volume growth.

Other drivers and restraints analyzed in the detailed report include:

- CUSMA Rules-of-Origin Tightening

- Digitized E-Manifests and Single-Window Customs

- Border Inspection Capacity Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Road freight accounted for 91.09% of the US-Canada cross-border freight transport market size in 2025, and is projected to grow at 3.48% CAGR through 2031, eclipsing rail and pipeline alternatives. Trucking's supremacy stems from the just-in-time sequencing used by automotive and e-commerce supply chains, which cannot tolerate the 2- to 3-day dwell time typical of rail transloads. Major carriers like Old Dominion Freight Line and TFI International continue to expand their service centers near key crossings, such as the Ambassador and Peace Bridges, to strategically consolidate freight and minimize empty miles.

Rail remains the cost-efficient workhorse for grain, coal, and petroleum products moving through the mid-continent energy corridor. Canadian Pacific Kansas City's merger created the only single-line network linking Canada, the United States, and Mexico, providing one-stop service for Houston-to-Toronto plastic resin shippers. Concurrently, Canadian National continues to leverage its extensive cross-border network to compete for intermodal traffic feeding US Midwest manufacturing hubs. Even so, shippers cite 3- to 5-day transits and limited final-mile options as barriers to converting from truck. Unless rapid-reloading intermodal terminals proliferate near the border, rail's share will hover in the single digits.

Full Truckload (FTL) dominated road movements, accounting for 78.68% of value, due to contract-dedicated lanes that shuttle powertrain modules, stamped metal, and finished vehicles between Southern Ontario and the US Midwest. Less-than-Truckload (LTL) is the fastest-growing road sub-segment, expanding at a 3.84% CAGR through 2026-2031 as e-commerce sellers split orders into smaller, higher-frequency shipments. The push for 24-hour delivery is encouraging integrators such as FedEx and UPS to pre-position inventory in bonded hubs near major crossings, such as the Ambassador and Peace Bridges, leveraging Automated Commercial Environment (ACE) compliance to significantly reduce border dwell times. Driver shortages persist, yet fleets that guarantee home-daily routes near border crossings are filling seats faster and securing rate premiums that offset wage inflation.

Technology further widens performance gaps inside the road segment. Carriers that link transportation management systems directly to the CBSA single-window platform achieve highly expedited crossings even during seasonal peaks, whereas paper-manifest operators experience much longer idle times. Major LTL carriers continue to invest heavily in cross-dock facilities near key border gateways, consolidating northbound and southbound freight to optimize linehaul density and reduce empty-mile ratios. Furthermore, cross-border fleets increasingly utilize regional relay yards to shorten average haul lengths, strategically keeping trips within the FMCSA's 11-hour Hours-of-Service limit to maximize tractor utilization.

Complete Report Scope:

- By Mode of Transportation

- Road Freight Transport

- Full Truckload (FTL)

- Less-than-Truckload (LTL)

- Rail Freight Transport

- Road Freight Transport

- By End-User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Distributive Trade (Wholesale and Retail trade)

- Healthcare and Pharmaceutical

- Manufacturing and Automotive

- Oil and Gas, Mining and Quarrying

- Other End-user Industries

- By Cross-Border Lane

- United States to Canada

- Canada to United States

List of Companies Covered in this Report:

- FedEx

- United Parcel Service of America, Inc. (UPS)

- C.H. Robinson Worldwide, Inc.

- J.B. Hunt Transport, Inc.

- Canadian National Railway Company

- Canadian Pacific Kansas City Limited

- Schneider National, Inc.

- XPO, Inc.

- Canada Post Corporation (Including Purolator Inc.)

- TFI International Inc.

- Old Dominion Freight Line

- Knight-Swift Transportation Holdings INC.

- Bison Transport

- TransX

- Landstar System, Inc.

- Werner Enterprises.

- Ryder System, Inc.

- DSV A/S (Including DB Schenker)

- DHL Group

- Kuehne+Nagel International AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Market Drivers

- 4.2.2 OEM Near-Shoring of Automotive Supply Chains

- 4.2.3 "E-Commerce North" Same-Day Delivery Guarantees

- 4.2.4 CUSMA Rules-Of-Origin Tightening

- 4.2.5 Digitised E-Manifests and Single-Window Customs

- 4.2.6 Mid-Continent Trade Corridor Infrastructure Upgrades

- 4.2.7 Border Infrastructure Modernization and Capacity Expansion

- 4.3 Market Restraints

- 4.3.1 Driver Shortages & Hours-Of-Service Caps

- 4.3.2 Border Inspection Capacity Bottlenecks

- 4.3.3 Carbon-Pricing Surcharge Divergence

- 4.3.4 Geopolitical Trade Policy Uncertainty and Tariff Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Market Value in USD billion)

- 5.1 By Mode of Transportation

- 5.1.1 Road Freight Transport

- 5.1.1.1 Full Truckload (FTL)

- 5.1.1.2 Less-than-Truckload (LTL)

- 5.1.2 Rail Freight Transport

- 5.1.1 Road Freight Transport

- 5.2 By End-User Industry

- 5.2.1 Agriculture, Fishing, and Forestry

- 5.2.2 Construction

- 5.2.3 Distributive Trade (Wholesale and Retail trade)

- 5.2.4 Healthcare and Pharmaceutical

- 5.2.5 Manufacturing and Automotive

- 5.2.6 Oil and Gas, Mining and Quarrying

- 5.2.7 Other End-user Industries

- 5.3 By Cross-Border Lane

- 5.3.1 United States to Canada

- 5.3.2 Canada to United States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 FedEx

- 6.4.2 United Parcel Service of America, Inc. (UPS)

- 6.4.3 C.H. Robinson Worldwide, Inc.

- 6.4.4 J.B. Hunt Transport, Inc.

- 6.4.5 Canadian National Railway Company

- 6.4.6 Canadian Pacific Kansas City Limited

- 6.4.7 Schneider National, Inc.

- 6.4.8 XPO, Inc.

- 6.4.9 Canada Post Corporation (Including Purolator Inc.)

- 6.4.10 TFI International Inc.

- 6.4.11 Old Dominion Freight Line

- 6.4.12 Knight-Swift Transportation Holdings INC.

- 6.4.13 Bison Transport

- 6.4.14 TransX

- 6.4.15 Landstar System, Inc.

- 6.4.16 Werner Enterprises.

- 6.4.17 Ryder System, Inc.

- 6.4.18 DSV A/S (Including DB Schenker)

- 6.4.19 DHL Group

- 6.4.20 Kuehne+Nagel International AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment