PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072791

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072791

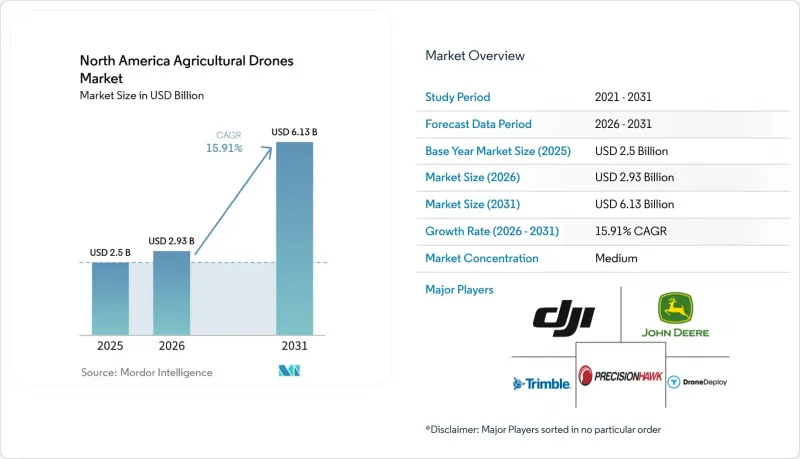

North America Agricultural Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america agricultural drones market size is projected to grow from USD 2.50 billion in 2025 and USD 2.93 billion in 2026 to USD 6.13 billion by 2031, registering a CAGR of 15.91% between 2026 and 2031.

This report is Segmented by Drone Type (Multi-Rotor, Fixed-Wing, and More), by Application (Crop Monitoring and Scouting, Precision Spraying and Fertilization, and More), by Component (Hardware, Software, and More), by Autonomy Level (Remote-Controlled, Semi-Autonomous, and More), and by Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Agricultural Drones Market Trends and Insights

Rapid Precision-Agriculture Adoption Across Large United States and Canadian Farms

Large-scale farms in the United States and Canada are increasingly adopting digital farming technologies to enhance field efficiency, optimize input usage, and improve crop monitoring. According to the United States Department of Agriculture Economic Research Service report published in December 2024, guidance autosteering systems and other equipment were utilized on 70% of large-scale crop-producing farms in the United States. The expanding use of precision agriculture systems is fostering favorable conditions for the adoption of agricultural drones, particularly for applications such as multispectral imaging, crop scouting, and variable-rate application in major row-crop-producing regions across North America.

Falling Costs and Better Performance of Multi-Rotor and Fixed-Wing Drones

Declining drone costs, combined with significant advancements in payload capacity, battery efficiency, and field productivity, are driving the adoption of agricultural drones across North America. In February 2026, XAG launched the P150 Max agricultural drone in the United States, featuring a maximum payload capacity of 176 pounds and an average spraying productivity of 50-60 acres per hour . Its swarm-control capability allows a single operator to manage two drones simultaneously. Furthermore, DJI Technology Co. Ltd.'s DB1560 Intelligent Flight Battery offers up to 1,500 charge cycles and nine-minute fast charging, minimizing downtime during critical application periods.

Data-Platform Compatibility Gaps With Legacy Machinery

Older tractors and sprayers from CNH Industrial, AGCO Corporation, and early John Deere series do not have built-in compatibility with drone-generated shapefiles, necessitating manual data transfers or expensive display upgrades. Middleware solutions like agrirouter are being introduced to enable automated synchronization between the John Deere Operations Center and third-party software. However, full bidirectional telemetry and prescription data exchange are not projected until late 2026. While AcreConnect currently supports exporting application maps compatible with DJI, XAG, and Exedy drones, many mixed fleets continue to depend on USB sticks, increasing the likelihood of errors.

Other drivers and restraints analyzed in the detailed report include:

- Easier Federal Aviation Administration Beyond Visual Line of Sight (FAA BVLOS) Approvals Boosting Acreage Coverage

- Tariff-Driven Domestic Drone Assembly Strengthening Supply Resilience

- High Upfront and Maintenance Costs for Small Growers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-rotor accounted for the largest 49.0% of the North America agricultural drones market share in 2025. This segment benefits from features such as vertical take-off capability, maneuverability in irregular field layouts, and suitability for targeted spraying and crop monitoring. Farmers in the United States Midwest and Canadian prairie provinces are increasingly adopting multi-rotor systems for applications like fungicide spraying, crop scouting, and nutrient assessment. These drones are favored for their simplified operation and compatibility with precision agriculture workflows.

The North America agricultural drones market size for hybrid (VTOL) is projected to expand at the fastest 17.4% CAGR from 2026 to 2031. This segment combines the cruising efficiency of fixed-wing drones with the vertical take-off flexibility of multi-rotor systems, making it ideal for large-acre farms requiring extended coverage and operational efficiency. Factors such as increasing interest in beyond visual line of sight (BVLOS) operations, advancements in battery charging speed, and swarm-control capabilities are driving the adoption of hybrid drones in broadacre farming.

Crop monitoring and scouting held the largest 38.0% market share in 2025. Agricultural producers are increasingly utilizing drone-based imaging systems to detect nutrient deficiencies, pest infestations, irrigation inconsistencies, and crop stress conditions before visible damage occurs in the field. Multispectral and thermal imaging technologies play a critical role in precision farming by enabling growers to optimize fertilizer application, enhance yield forecasting, and monitor crop health across extensive farming areas. Adoption is particularly strong in regions producing corn, soybean, wheat, and specialty crops, where labor shortages and rising operational costs drive the use of automated aerial monitoring solutions for field management and agronomic assessments.

Precision spraying and fertilization are projected to grow at the fastest 16.9% CAGR from 2026 to 2031. This growth is driven by the increasing adoption of drone-based pesticide application, the rising use of variable-rate technologies, and the demand for reduced chemical wastage in commercial farming operations. Agricultural drones equipped with centrifugal atomizers and precision application systems are enhancing spray consistency, reducing input consumption, and minimizing field compaction. Regulatory approvals for multi-drone operations and the integration of prescription mapping technologies are further boosting demand for precision spraying services, particularly among large farms and agricultural contractors aiming to improve operational efficiency and reduce per-acre treatment costs.

Complete Report Scope:

- By Drone Type

- Multi-rotor

- Fixed-wing

- Hybrid (VTOL)

- By Application

- Crop Monitoring and Scouting

- Precision Spraying and Fertilization

- Soil and Field Analysis

- Irrigation Management

- Planting and Seeding

- Livestock Monitoring

- By Component

- Hardware

- Frame and Airframe

- Propulsion System

- Batteries and Power

- Sensors and Payloads

- Software

- Flight Planning and Control

- Data Analytics and AI

- Fleet Management

- Services

- Drone-as-a-Service

- Training and Support

- Maintenance and Repair

- Hardware

- By Autonomy Level

- Remote-Controlled

- Semi-Autonomous

- Fully Autonomous

- By Country

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- DJI Technology Co. Ltd.

- Deere and Company

- Trimble Inc.

- PrecisionHawk Inc.

- DroneDeploy Inc.

- Sentera Inc.

- AgEagle Aerial Systems Inc.

- Raptor Maps Inc.

- XAG Co. Ltd.

- Hylio Inc.

- Skydio Inc.

- Parrot SA

- AeroVironment Inc.

- Delair SAS

- Terra Drone Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid precision-agriculture adoption across large United States and Canadian farms

- 4.2.2 Falling costs and better performance of multi-rotor and fixed-wing drones

- 4.2.3 Easier Federal Aviation Administration beyond visual line of sight (FAA BVLOS) approvals boosting acreage coverage

- 4.2.4 Tariff-driven domestic drone assembly strengthening supply resilience

- 4.2.5 Carbon-credit revenue from variable-rate input reduction

- 4.2.6 Drone-as-a-Service expansion in Mexico's specialty crop belt

- 4.3 Market Restraints

- 4.3.1 Data-platform compatibility gaps with legacy machinery

- 4.3.2 High upfront and maintenance costs for small growers

- 4.3.3 Shortage of licensed remote pilots with agronomic analytics expertise

- 4.3.4 Stricter lithium-battery shipping regulations affecting field logistics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Drone Type

- 5.1.1 Multi-rotor

- 5.1.2 Fixed-wing

- 5.1.3 Hybrid (VTOL)

- 5.2 By Application

- 5.2.1 Crop Monitoring and Scouting

- 5.2.2 Precision Spraying and Fertilization

- 5.2.3 Soil and Field Analysis

- 5.2.4 Irrigation Management

- 5.2.5 Planting and Seeding

- 5.2.6 Livestock Monitoring

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.1.1 Frame and Airframe

- 5.3.1.2 Propulsion System

- 5.3.1.3 Batteries and Power

- 5.3.1.4 Sensors and Payloads

- 5.3.2 Software

- 5.3.2.1 Flight Planning and Control

- 5.3.2.2 Data Analytics and AI

- 5.3.2.3 Fleet Management

- 5.3.3 Services

- 5.3.3.1 Drone-as-a-Service

- 5.3.3.2 Training and Support

- 5.3.3.3 Maintenance and Repair

- 5.3.1 Hardware

- 5.4 By Autonomy Level

- 5.4.1 Remote-Controlled

- 5.4.2 Semi-Autonomous

- 5.4.3 Fully Autonomous

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DJI Technology Co. Ltd.

- 6.4.2 Deere and Company

- 6.4.3 Trimble Inc.

- 6.4.4 PrecisionHawk Inc.

- 6.4.5 DroneDeploy Inc.

- 6.4.6 Sentera Inc.

- 6.4.7 AgEagle Aerial Systems Inc.

- 6.4.8 Raptor Maps Inc.

- 6.4.9 XAG Co. Ltd.

- 6.4.10 Hylio Inc.

- 6.4.11 Skydio Inc.

- 6.4.12 Parrot SA

- 6.4.13 AeroVironment Inc.

- 6.4.14 Delair SAS

- 6.4.15 Terra Drone Corporation

7 Market Opportunities and Future Outlook