PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072807

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072807

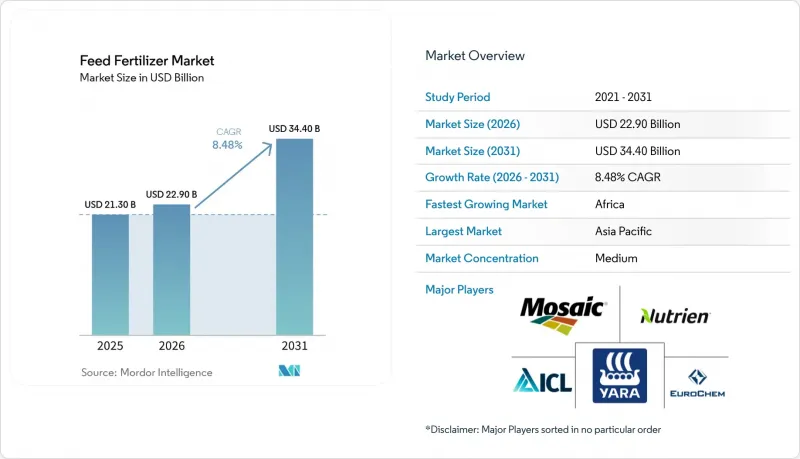

Feed Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the feed fertilizer market size is projected to expand from USD 21.3 billion in 2025 and USD 22.9 billion in 2026 to USD 34.4 billion by 2031, registering a CAGR of 8.48% during 2026-2031.

This report is Segmented by Product Type (Nitrogen-Based, Phosphate-Based, and More), by Form (Dry Granules, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Feed Fertilizer Market Trends and Insights

Government Mandates on Sustainable Livestock Productivity

In 2025, the European Union Common Agricultural Policy introduced mandatory nutrient budgeting rules, requiring farms to document fertilizer usage in accordance with soil threshold limits. Similarly, in the United States and Canada, compliance measures tie subsidy eligibility to nutrient audits, encouraging the adoption of precision-dosed products with full traceability. These regulatory frameworks have driven innovation in the agricultural sector, as seen with Yara International's launch of the YaraPlus platform in 2025, which provides real-time recommendations aligned with regulatory requirements and creates new service-based revenue opportunities. Complementing these global efforts, India introduced a fermented organic manure program in the same year, subsidizing 50% of setup costs for smallholder dairy farmers. Together, these initiatives highlight a global shift towards sustainable livestock practices, fostering increased demand for precision agriculture and organic inputs while aligning with environmental and economic goals.

Growing Demand for High-Protein Diets in Emerging Economies

Dietary shifts in the Asia-Pacific region toward higher consumption of meat, fish, and eggs are driving growth in compound feed volumes, subsequently impacting the feed fertilizer market. This trend is further supported by rising disposable incomes in countries such as Indonesia, Bangladesh, and Vietnam, which are fueling the expansion of intensive shrimp farming operations requiring precise nitrogen and phosphate applications. While poultry remains dominant, its growth is stabilizing in mature exporting countries like Thailand, prompting investors to redirect capital toward fish and shrimp value chains. Consequently, the increasing demand for protein is steering the market toward liquid concentrates optimized for closed-loop systems, marking a shift away from traditional broad-acre granules and aligning with the evolving needs of these emerging economies.

Price Volatility of Key Raw Materials

Fluctuations in phosphate and nitrate prices disrupt procurement planning and reduce operating margins for feed fertilizer suppliers. Nutrien's 2025 closure of its Trinidad nitrogen facility, cutting 0.7 million metric tons of ammonia production, underscores how sustained cost inflation forces capacity reductions. Simultaneously, China's 2025 phosphate export quota tightened global supply, driving price surges in Africa and South America. Smaller producers, lacking vertical integration or long-term contracts, face the full impact of these shocks, leading to reduced innovation spending and higher costs for livestock farmers, ultimately constraining market growth.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Aquaculture Requiring Water-Soluble Feed Fertilizers

- Rising Adoption of Precision Farming in Animal Husbandry

- Stringent Residue Limits in Animal-Source Foods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nitrogen-based feed fertilizers held the largest share, accounting for 42.5% of 2025 revenue in the feed fertilizer market, reflecting their critical role in protein synthesis and their linkage to global ammonia networks. Bio-based feed fertilizers held only a limited share yet posted the fastest 12.7% CAGR through 2026-2031, suggesting a rising appetite for carbon-friendly inputs. Phosphate-based feed fertilizers captured a prominent share of the market, driven by skeletal growth requirements in poultry and swine, while potash served ruminants. The segment narrative, therefore, revolves around nitrogen defending its dominant position while bio-based lines become premium niches.

Coromandel International recorded 18% specialty-nutrient growth in Q3 FY 2025 after the launch of Gromor Bio Organic, indicating tangible traction among Indian dairies. YaraBasa TURBO, launched in Brazil in 2025, integrates urease inhibitors that reduce ammonia loss by 30%, illustrating how incumbents defend their share via upgraded chemistries. China's export quotas pressure phosphate availability, widening price differentials, and nudging buyers toward nitrogen-potash blends. Over 2026-2031, the feed fertilizer market for nitrogen remains sturdy, but portfolio growth will tilt toward bio-based innovations that bundle carbon credit revenue.

Complete Report Scope:

- By Product Type

- Nitrogen-Based Feed Fertilizers

- Phosphate-Based Feed Fertilizers

- Potash-Based Feed Fertilizers

- Bio-Based Feed Fertilizers

- By Form

- Dry Granules

- Liquid Concentrates

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

In 2025, Asia-Pacific led the market with a 38.2% share, driven by concentrated poultry clusters in China, expanding dairy operations in India, and robust shrimp farming in Vietnam and Indonesia. Tightened phosphate-export quotas in China prompted diversification into nitrogen and bio-based blends, enhancing per-unit value. Africa is projected to grow at a 9.4% CAGR during 2026-2031, is advancing through government initiatives promoting protein self-sufficiency and feed infrastructure upgrades, with mobile payments and cooperative hubs improving distribution despite logistical challenges.

North America's steady growth is fueled by carbon-credit monetization supporting manure-derived fertilizers, while South America benefits from vertically integrated poultry and swine chains that optimize input costs. Europe's growth remains constrained by strict nutrient budgets, though premium enhanced-efficiency products mitigate tonnage declines. The Middle East is expanding through investments in domestic nutrient complexes for food security, while Russia's herd rebuilding efforts are tempered by limited access to precision-farming technologies due to sanctions.

Global demand is rising as sustainability mandates and protein consumption increase. Asia-Pacific's scale sets pricing benchmarks, Africa's rapid growth adds new volume opportunities, and innovation from North and South America spreads globally through partnerships. These interconnected regional dynamics, supported by synchronized policy incentives and digital platforms, are anticipated to narrow adoption gaps and drive the global feed fertilizer market forward.

- Yara International ASA

- Nutrien Ltd.

- The Mosaic Company

- ICL Group Ltd.

- EuroChem Group AG

- OCP S.A.

- Koch Agronomic Services, LLC (Koch Industries Inc.)

- CF Industries Holdings, Inc.

- Wilbur-Ellis Nutrition, LLC (Wilbur-Ellis Holdings, Inc.)

- Coromandel International Ltd. (Murugappa Group)

- Haifa Negev Technologies Ltd.

- Innophos Holdings, Inc. (One Rock Capital Partners)

- Phosphea (Groupe Roullier)

- J. R. Simplot Company

- Grupa Azoty S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government mandates on sustainable livestock productivity

- 4.2.2 Growing demand for high-protein diets in emerging economies

- 4.2.3 Expansion of aquaculture requiring water-soluble feed fertilizers

- 4.2.4 Rising adoption of precision farming in animal husbandry

- 4.2.5 Algae-based biofertilizers are improving feed conversion ratios

- 4.2.6 Carbon-credit monetization of manure-derived fertilizers

- 4.3 Market Restraints

- 4.3.1 Price volatility of key raw materials

- 4.3.2 Stringent residue limits in animal-source foods

- 4.3.3 Slow regulatory approvals for novel microbial fertilizers

- 4.3.4 Farm-level resistance to data-sharing for precision plans

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Nitrogen-Based Feed Fertilizers

- 5.1.2 Phosphate-Based Feed Fertilizers

- 5.1.3 Potash-Based Feed Fertilizers

- 5.1.4 Bio-Based Feed Fertilizers

- 5.2 By Form

- 5.2.1 Dry Granules

- 5.2.2 Liquid Concentrates

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Russia

- 5.3.3.4 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Yara International ASA

- 6.4.2 Nutrien Ltd.

- 6.4.3 The Mosaic Company

- 6.4.4 ICL Group Ltd.

- 6.4.5 EuroChem Group AG

- 6.4.6 OCP S.A.

- 6.4.7 Koch Agronomic Services, LLC (Koch Industries Inc.)

- 6.4.8 CF Industries Holdings, Inc.

- 6.4.9 Wilbur-Ellis Nutrition, LLC (Wilbur-Ellis Holdings, Inc.)

- 6.4.10 Coromandel International Ltd. (Murugappa Group)

- 6.4.11 Haifa Negev Technologies Ltd.

- 6.4.12 Innophos Holdings, Inc. (One Rock Capital Partners)

- 6.4.13 Phosphea (Groupe Roullier)

- 6.4.14 J. R. Simplot Company

- 6.4.15 Grupa Azoty S.A.

7 Market Opportunities and Future Outlook