PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073600

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073600

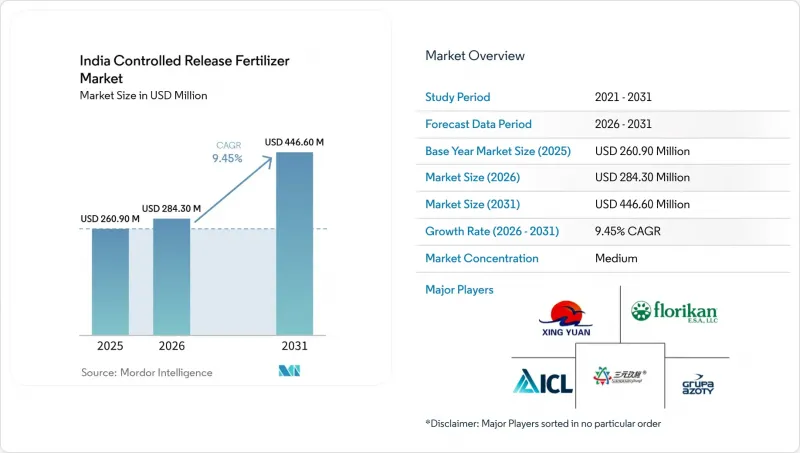

India Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india controlled release fertilizer market size is projected to increase from USD 260.90 million in 2025 to USD 284.30 million in 2026 and reach USD 446.60 million by 2031, growing at a CAGR of 9.45% over 2026-2031.

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others) and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

India Controlled Release Fertilizer Market Trends and Insights

Government Subsidies for Neem-Coated and Specialty Fertilizers

Direct Benefit Transfer keeps neem-coated urea affordable by the Maximum Retail Price (MRP) is legally set at a low level. For instance, USD 2.67 per 45 kg bag, excluding taxes and neem-coating charges. Since 2015, every domestic urea bag is neem-coated, familiarizing farmers with extended release concepts and creating a logistics backbone for specialty SKUs. The federal move is amplified by state add-on incentives in Punjab and Haryana that reward the use of biodegradable coatings to curb nitrate seepage into the region's heavily tapped aquifers. Economic Survey 2025-26 recommends converting blanket support to cash transfers, which could equalize the playing field by 2028. Firms in Uttar Pradesh and Madhya Pradesh bundle soil testing with neem-coated controlled release packs, converting a statutory coating cost into a customer acquisition lever. These visible labor and cost benefits are speeding word-of-mouth diffusion in wheat and rice belts where adoption resistance was historically high.

High Yield and Nutrient Use Efficiency (NUE) Targets

The National Mission for Sustainable Agriculture pegs a nutrient use efficiency target for 2030, a goal embedded in state action plans and backed by rising groundwater nitrate alarms. This linkage pressures local departments to promote controlled release fertilizers that boost nutrient recovery compared with standard prilled urea. Field trials by the Indian Council of Agricultural Research in 2025 showed 12-15% yield gains in basmati rice when polymer-coated urea replaced three split applications. Because the target is written into subsidy scorecards, district officials actively seek technology partners to conduct village-level trials, providing coated products with valuable on-farm validation. Over the next five years, this administrative nudge is anticipated to draw coated fertilizers more deeply into broad-acre crops, which still dominate input volumes. Adoption will accelerate once farmers are compensated for measured efficiency gains rather than per-bag purchases.

High Upfront Cost Versus Subsidized Urea

Controlled-release fertilizers are priced at INR 45-75 per kg (USD 0.54-0.90), compared to conventional urea, which costs INR 6 per kg (USD 0.07). This results in a nutrient cost per acre that is seven to twelve times higher for coated fertilizers. Smallholders cultivating less than one hectare find it difficult to justify this premium for low-value cereals. These farmers often depend on seasonal credit and avoid higher upfront costs, even if the long-term economics of coated products are favorable. Cooperative banks remain cautious, as the resale value of specialty inputs is lower, reducing their viability as collateral for microloans. Additionally, nano urea, priced at INR 240 (USD 2.88) for a 500ml bottle, offers comparable nitrogen use efficiency (NUE) improvements, further limiting the demand for coated fertilizers. While sachet packs and pay-per-use models reduce initial costs, they require intensive distribution efforts. Consequently, the adoption of coated fertilizers follows a pyramid structure, with top-tier commercial growers adopting them first and serving as proof points, while broader adoption at the base depends on either increased subsidies or innovative pay-as-you-use delivery mechanisms.

Other drivers and restraints analyzed in the detailed report include:

- Precision Agriculture and Fertigation Expansion

- Biodegradable-Coating Push Under Emerging Micro-Plastic Norms

- Low Farmer Awareness and Channel Reach

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-coated products accounted for 69.6% of the India controlled-release fertilizer market share in 2025. Sales are strongest in the drip-irrigated belts of Maharashtra, Gujarat, and Karnataka, where predictable nutrient-release curves align with fertigation schedules. Draft regulations on microplastic residues, however, are accelerating research into starch- and polyhydroxyalkanoate (PHA)-based coatings that decompose within 180 days. Early pilot programs indicate comparable agronomic performance, although these solutions still carry a cost premium over conventional polyolefin coatings.

Polymer sulfur-coated products are projected to be the fastest-growing coating type, expanding at a CAGR of 8.2% during 2026-2031. This growth is driven by increasing demand in sulfur-deficient soils across Punjab and Haryana, where these products provide both sulfur supplementation and controlled nitrogen release. Resin- and wax-coated products continue to serve niche markets, particularly in the turf and ornamental segments, which prioritize 9-12-month nutrient release and reduced labor requirements. The India controlled-release fertilizer market is anticipated to shift toward biodegradable materials as cost disparities narrow and standards governing acceptable residue levels become clearer. Companies with patented bio-coating technologies and renewable feedstock supply chains are likely to gain a competitive advantage as early adopters in this evolving market.

Complete Report Scope:

- By Coating Type

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- By Crop Type

- Field Crops

- Horticultural Crops

- Turf and Ornamental

List of Companies Covered in this Report:

- ICL Group Ltd

- Compo Expert GmbH (Grupa Azoty S.A.)

- Florikan ESA LLC (New Mountain Capital LLC)

- Coromandel International Limited (Murugappa Group)

- Nutrien Ltd

- Yara International ASA

- Haifa Negev Technologies Ltd (Haifa Group)

- Koch Agronomic Services LLC (Koch Industries Inc.)

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Sociedad Quimica y Minera de Chile S.A.

- Kingenta Ecological Engineering Co., Ltd.

- Chambal Fertilisers and Chemicals Limited (Adventz Group)

- Gujarat State Fertilizers & Chemicals Limited

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd (Hebei Sanyuan Agricultural Group)

- Zhongchuang Xingyuan Chemical Technology Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Government subsidies for neem-coated and specialty fertilizers

- 4.5.2 High yield and nitrogen use efficiency (NUE) targets

- 4.5.3 Precision agriculture and fertigation expansion

- 4.5.4 Corporate sustainability sourcing mandates

- 4.5.5 Biodegradable-coating push under emerging micro-plastic norms

- 4.5.6 Horticulture export clusters adopting controlled release fertilizers

- 4.6 Market Restraints

- 4.6.1 High upfront cost versus subsidized urea

- 4.6.2 Low farmer awareness and channel reach

- 4.6.3 Heat-driven release-rate variability

- 4.6.4 Potential ban on non-degradable polymer residues

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 By Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf and Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ICL Group Ltd

- 6.4.2 Compo Expert GmbH (Grupa Azoty S.A.)

- 6.4.3 Florikan ESA LLC (New Mountain Capital LLC)

- 6.4.4 Coromandel International Limited (Murugappa Group)

- 6.4.5 Nutrien Ltd

- 6.4.6 Yara International ASA

- 6.4.7 Haifa Negev Technologies Ltd (Haifa Group)

- 6.4.8 Koch Agronomic Services LLC (Koch Industries Inc.)

- 6.4.9 Deepak Fertilisers and Petrochemicals Corporation Limited

- 6.4.10 Sociedad Quimica y Minera de Chile S.A.

- 6.4.11 Kingenta Ecological Engineering Co., Ltd.

- 6.4.12 Chambal Fertilisers and Chemicals Limited (Adventz Group)

- 6.4.13 Gujarat State Fertilizers & Chemicals Limited

- 6.4.14 Hebei Sanyuanjiuqi Fertilizer Co., Ltd (Hebei Sanyuan Agricultural Group)

- 6.4.15 Zhongchuang Xingyuan Chemical Technology Co., Ltd

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS