PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073612

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073612

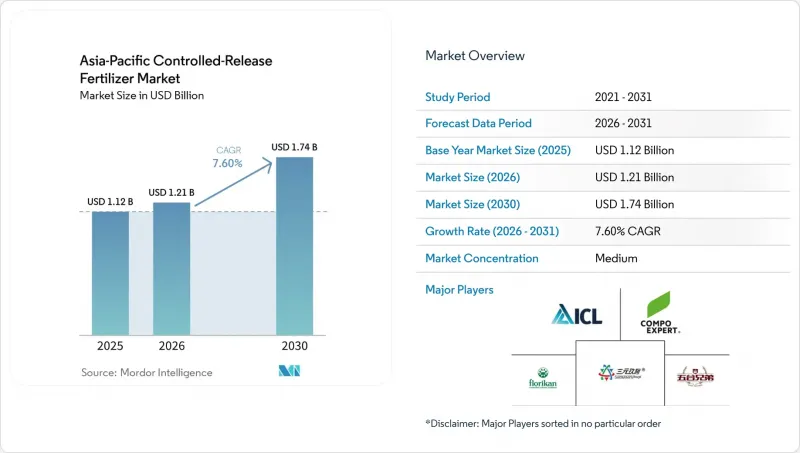

Asia-Pacific Controlled-Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific controlled-release fertilizer market size reached USD 1.12 billion in 2025, is estimated to reach USD 1.21 billion in 2026, and is projected to rise to USD 1.74 billion by 2031, expanding at a 7.60% CAGR during 2026 to 2031.

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others), by Crop Type (Field Crops, Horticultural Crops, and Turf & Ornamental), and by Country (Australia, Bangladesh, China, India, Indonesia, Japan, Pakistan, Philippines, Thailand, Vietnam, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Asia-Pacific Controlled-Release Fertilizer Market Trends and Insights

Surge in Government Subsidies for Eco-Efficient Fertilizers

Targeted fiscal support is reshaping fertilizer economics across much of the Asia-Pacific. India's nutrient-based subsidy scheme now covers controlled-release formulations, lowering farmer switching costs by up to 40% and driving significant sales volume in Uttar Pradesh, Punjab, and Tamil Nadu. China deploys a mix of direct input subsidies and reduced value-added tax on eco-efficient fertilizers, providing twin price and liquidity advantages for growers. Agricultural banks in Indonesia and Vietnam are adding preferential credit lines that specifically earmark funds for controlled-release purchases, signaling sustained public-sector commitment. As a result, manufacturers are expanding capacity closer to demand centers to satisfy subsidy-driven orders, while distributors intensify extension services to capture emerging rural demand.

Rapid Expansion of Protected Cultivation Acreage

Protected cultivation systems are growing rapidly across the Asia-Pacific region, driven by urbanization and the demand for year-round high-value crop production. Australia's greenhouse sector has grown by 15% annually since 2024, with controlled environment agriculture requiring precise nutrient management that favors controlled-release fertilizers over conventional types. The growth is significant in hydroponic and aeroponic systems, where nutrient solution management reduces total fertilizer consumption by up to 60% through automated dosing and recycling systems. Thailand's GAP 9001-2021 standards for hydroponic vegetable production require regular water quality monitoring and chemical residue testing, creating a regulatory need for controlled-release technologies that reduce leaching and environmental contamination . This expansion of protected cultivation increases the demand for specialized controlled-release formulations for soilless media, as traditional granular fertilizers cannot provide precise nutrient timing. Consumers' willingness to pay higher prices for greenhouse-grown produce supports the economic viability of advanced nutrient management systems.

High Upfront Cost Versus Conventional NPK

Controlled-release fertilizers still carry a 1.8 times price premium over standard urea in most Asia-Pacific markets, a hurdle magnified for smallholders who dominate rice and wheat acreage. While subsidies offset part of the gap, out-of-pocket expenses remain high, and many growers defer adoption until clear seasonal paybacks are validated through neighbor demonstration plots. In China, the cost of equipment, such as drip or sprinkler systems essential for precise application, can surpass USD 1,400 per mu (equivalent to USD 93.3 per ha). Limited access to agricultural credit and risk-averse farming practices further constrain adoption among smallholders who cannot afford the higher initial investment despite potential long-term benefits.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Precision-Fertigation in High-Value Crops

- Introduction of Enzyme-Embedded Coatings Lowers Release Variability

- Limited Retailer Education Outside Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-coated products held the largest Asia-Pacific controlled-release fertilizer market share at 71.2% in 2025, reflecting the technology's maturity and effectiveness across diverse agricultural systems. Their widespread adoption is driven by robust manufacturing capabilities in countries like China and Japan, coupled with demonstrated benefits in nutrient-use efficiency and controlled nutrient release. Ongoing advancements in coating formulations continue to enhance performance under diverse climatic conditions, further solidifying the segment's leading position.

Polymer sulfur-coated products are anticipated to be the fastest-growing coating type, with a projected CAGR of 8.9% through 2031. This growth is attributed to rising demand for cost-effective controlled-release solutions and advancements in coating technologies that improve nutrient delivery consistency. Concurrently, polymer-coated fertilizers maintain their appeal due to their ability to enhance crop productivity, minimize nutrient losses, and facilitate precision nutrient management across key crops in the region.

Complete Report Scope:

- Coating Type

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

- Country

- Australia

- Bangladesh

- China

- India

- Indonesia

- Japan

- Pakistan

- Philippines

- Thailand

- Vietnam

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- ICL Group Ltd

- Grupa Azoty S.A. (Compo Expert)

- New Mountain Capital (Florikan)

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Kingenta Ecological Engineering Group Co., Ltd.

- Compo Expert GmbH

- Haifa Chemicals Ltd.

- Nutrien Ltd.

- Yara International ASA

- Koch Agronomic Services, LLC

- SQM S.A.

- Shandong Hualu-Hengsheng Chemical Co., Ltd.

- Hubei Xinyangfeng Fertilizer Co., Ltd.

- Shandong Luxi Fertilizer Co., Ltd.

- Florikan-E.S.A., LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Surge in government subsidies for eco-efficient fertilizers

- 4.6.2 Rapid expansion of protected cultivation acreage

- 4.6.3 Shift toward precision-fertigation in high-value crops

- 4.6.4 Introduction of enzyme-embedded coatings lowers release variability

- 4.6.5 Mandatory nutrient-runoff caps adopted by island economies

- 4.6.6 Emergence of bio-based polyurethane coatings from palm-kernel oil

- 4.7 Market Restraints

- 4.7.1 High upfront cost versus conventional NPK

- 4.7.2 Limited retailer education outside Tier-1 cities

- 4.7.3 Supply risk of specialty coating polymers

- 4.7.4 Regional bans on micro-plastic coated granules

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 Bangladesh

- 5.3.3 China

- 5.3.4 India

- 5.3.5 Indonesia

- 5.3.6 Japan

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 ICL Group Ltd

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 New Mountain Capital (Florikan)

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Compo Expert GmbH

- 6.4.7 Haifa Chemicals Ltd.

- 6.4.8 Nutrien Ltd.

- 6.4.9 Yara International ASA

- 6.4.10 Koch Agronomic Services, LLC

- 6.4.11 SQM S.A.

- 6.4.12 Shandong Hualu-Hengsheng Chemical Co., Ltd.

- 6.4.13 Hubei Xinyangfeng Fertilizer Co., Ltd.

- 6.4.14 Shandong Luxi Fertilizer Co., Ltd.

- 6.4.15 Florikan-E.S.A., LLC.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS