PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072837

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072837

India Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

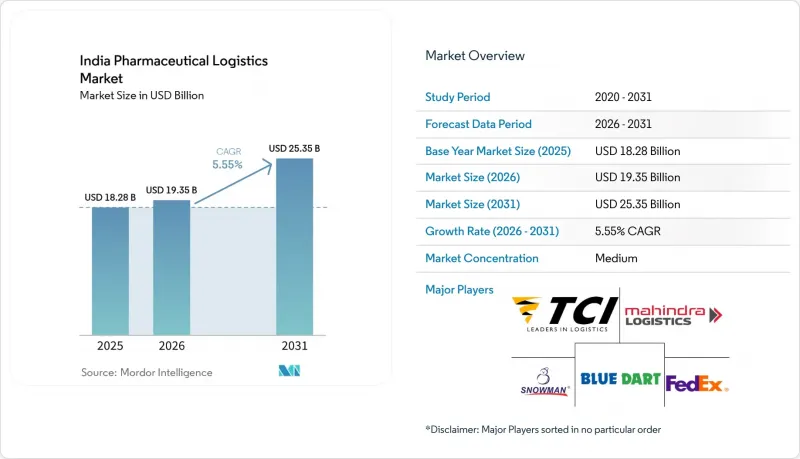

According to Mordor Intelligence, the india pharmaceutical logistics market size is expected to increase from USD 18.28 billion in 2025 to USD 19.35 billion in 2026 and reach USD 25.35 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

India's role as the world's largest supplier of generic medicines, accounting for 20% of global generic drug exports by volume, continues to expand the scale and complexity of domestic and export distribution flows. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Mode of Operation (Cold-Chain, Non-Cold-Chain), by Product Type (Prescription Drugs, OTC, Biologics, Vaccines, Clinical Trial Materials, Cell and Gene Therapies, Medical Devices, Veterinary Medicine), and by Region (North, Central, and More). The Market Forecasts are in Value (USD).

India Pharmaceutical Logistics Market Trends and Insights

Government Production-Linked Incentive Schemes

India pharmaceutical logistics market demand is rising with the scale-up created by the pharmaceutical and bulk drug PLI programs. As of December 2025, cumulative investment under these schemes reached INR 41,943 crores (USD 4.66 billion) and was more than double the initial commitment target of INR 17,275 crores (USD 1.92 billion). Cumulative sales under both schemes reached INR 3,35,036 crores (USD 37.28 billion) across 1,988 products, including exports worth INR 2,15,248 crores (USD 23.95 billion), indicating that production-linked incentives are already driving higher logistics volumes across domestic and export channels. The more important shift is in the product mix, as the program favors biopharmaceuticals, complex generics, and autoimmune therapies that require tighter thermal and handling controls than conventional oral solids. Union Budget 2026-27 also backed the Biopharma SHAKTI initiative with INR 10,000 crores (USD 1.11 billion) over 5 years and a target of more than 1,000 accredited clinical trial sites, which points to a longer cycle of specialized transport and compliant warehousing demand.

Rising Demand for Temperature-Controlled Biologics and Vaccines

India's pharmaceutical logistics market is being driven by a faster shift toward temperature-sensitive medicines. India supplies 60% of UNICEF's global vaccine procurement and meets 40%-70% of global demand for DPT and BCG vaccines, keeping vaccine handling capacity central to logistics planning. At the same time, the patent cliff for more than 40 major branded drugs between 2026 and 2030 is steering Indian manufacturers toward biologics, GLP-1 analogs, and specialty injectables that usually require 2 °C-8 °C control. This is putting pressure on a cold chain built primarily for bulk oral solids rather than for sensitive therapies. Kuehne+Nagel added HealthChain-certified cross-docks in Bengaluru in December 2025 and in Hyderabad in May 2026 to support API and vaccine exporters, indicating that providers are redesigning assets around this new mix.

Fragmented Cold-Chain Infrastructure Beyond Metros

India pharmaceutical logistics market expansion is still limited by the uneven spread of compliant cold infrastructure. The network remains concentrated in a small group of metros and manufacturing hubs, while Tier 2, Tier 3, and rural corridors stay underserved for temperature-controlled transport and storage. More than 3,500 cold-chain operators exist in India, yet only 8%-10% meet WHO-GDP standards, leaving a large share of the network below the quality level required for sensitive pharmaceutical handling. Blue Dart's National Operations Head stated in 2026 that temperature-controlled transport and storage remain limited across Tier II, Tier III, and rural regions, even as biologics, insulin, and vaccines move beyond urban demand centers. Smaller regional operators often cannot absorb the cost of validation, backup power, and continuous monitoring systems, which slows network quality improvement outside the main corridors.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of E-Pharmacy and D2C Drug Distribution

- RFID-Based Track-and-Trace Mandates by CDSCO

- High Compliance Cost of Evolving GDP Audits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 54.07% of the India pharmaceutical logistics market share in 2025, which confirms that road freight remains the core movement layer for domestic pharmaceutical distribution. Trucks remain essential because India's 6.3 million km of road network supports deliveries to more than 750 districts, where direct reach matters more than modal substitution. Air freight carries lower volume but earns much higher revenue per kilogram for biologics, clinical trial materials, and urgent API shipments, especially on export lanes to the United States, Europe, and ASEAN markets. Sea and inland waterways remain limited for pharmaceutical use because long transit windows make temperature control and monitoring harder to sustain at the required standards.

Value-added services are projected to record the fastest growth at 8.38% CAGR, which shows that the India pharmaceutical logistics industry is moving beyond pure transport and storage contracts. Pharmaceutical customers are increasingly combining packaging, kitting, serialization support, reverse logistics, and documentation management inside integrated agreements. Warehousing and distribution is also becoming more active because humidity control, batch segregation, temperature mapping, and GDP-compliant SOP execution are now part of routine operations rather than optional services. Rail remains small, but the weekly Maersk-CONCOR reefer corridor from Hyderabad to Nhava Sheva launched in May 2026 shows that dedicated pharma rail routes can work where shipment density is high enough.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North

- Central

- West

- East

- South

List of Companies Covered in this Report:

- DHL Group

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Blue Dart Express Pvt. Ltd.

- Allcargo Logistics Pvt. Ltd.

- TCI Express

- Mahindra Logistics, Ltd.

- Snowman Logistics

- ColdEx Logistics

- Safexpress Pvt. Ltd.

- Gati-KWE

- FM Logistic

- CMA CGM Group (Including CEVA Logistics)

- NYK Line (Including Yusen Logistics)

- TVS Supply Chain Solutions

- Stellar Value Chain Solutions

- Crystal Logistic Cool Chain

- ColdStar Logistics

- Celcius Logistics

- Life Care Logistic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Growth of Domestic Pharmaceutical Manufacturing Clusters

- 4.3.2 Government Production-Linked Incentive (PLI) Schemes

- 4.3.3 Rising Demand for Temperature-Controlled Biologics and Vaccines

- 4.3.4 Expansion of E-Pharmacy and D2C Drug Distribution

- 4.3.5 RFID-Based Track-and-Trace Mandates by CDSCO

- 4.3.6 Surge in Reverse Logistics Due to Expiry-Date Compliance

- 4.4 Market Restraints

- 4.4.1 Fragmented Cold-Chain Infrastructure Beyond Metros

- 4.4.2 High Compliance Cost of Evolving GDP Audits

- 4.4.3 Scarcity of Rail-Side Pharma-Grade Warehouses

- 4.4.4 Prospective Carbon-Tax on Diesel Reefer Fleets

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Central

- 5.4.3 West

- 5.4.4 East

- 5.4.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne+Nagel

- 6.4.3 DSV A/S (Including DB Schenker)

- 6.4.4 FedEx

- 6.4.5 United Parcel Service of America, Inc. (UPS)

- 6.4.6 Blue Dart Express Pvt. Ltd.

- 6.4.7 Allcargo Logistics Pvt. Ltd.

- 6.4.8 TCI Express

- 6.4.9 Mahindra Logistics, Ltd.

- 6.4.10 Snowman Logistics

- 6.4.11 ColdEx Logistics

- 6.4.12 Safexpress Pvt. Ltd.

- 6.4.13 Gati-KWE

- 6.4.14 FM Logistic

- 6.4.15 CMA CGM Group (Including CEVA Logistics)

- 6.4.16 NYK Line (Including Yusen Logistics)

- 6.4.17 TVS Supply Chain Solutions

- 6.4.18 Stellar Value Chain Solutions

- 6.4.19 Crystal Logistic Cool Chain

- 6.4.20 ColdStar Logistics

- 6.4.21 Celcius Logistics

- 6.4.22 Life Care Logistic

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment