PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072838

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072838

Germany Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

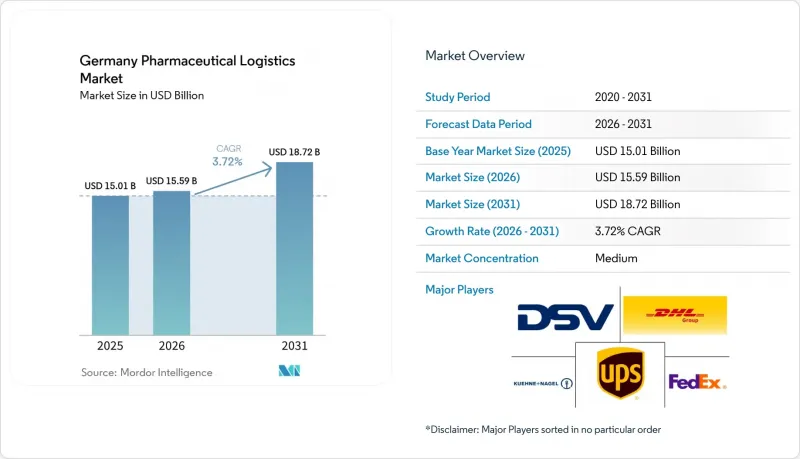

According to Mordor Intelligence, the germany pharmaceutical logistics market size is expected to increase from USD 15.01 billion in 2025 to USD 15.59 billion in 2026 and reach USD 18.72 billion by 2031, growing at a CAGR of 3.72% over 2026-2031.

The Germany pharmaceutical logistics market is expanding in a period when Germany's wider economy remains subdued, with GDP rising only 0.2% in 2025 and energy price risks still weighing on near-term industrial output. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, and Value-Added Services), by Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), by Product Type (Prescription Drugs, OTC Drugs, Biologics, Vaccines and Blood Products, and More), and by Region (North Rhine-Westphalia, and More). The Market Forecasts are Provided in Value (USD).

Germany Pharmaceutical Logistics Market Trends and Insights

Expanding Biologics and Biosimilars Pipeline Adoption

The Germany pharmaceutical logistics market is seeing a sharper shift toward cold-chain complexity as biologics and biosimilars move deeper into routine dispensing. Germany's pharmacy substitution framework for biosimilars took effect from April 1, 2026, which increased the need for precise lot tracking, controlled handovers, and clear chain-of-custody records at the pharmacy level. That change matters because it does not simply add volume to established wholesale lanes, it shifts more shipments into smaller and more frequent pharmacy-level consignments that are harder to manage with standard networks. The Germany pharmaceutical logistics market is therefore rewarding providers that can manage +2 °C to +8 °C, frozen, and cryogenic ranges inside one validated operating model. This is especially relevant in Bavaria and Baden-Wurttemberg, where biologics production, plasma handling, and specialty manufacturing are pushing demand for more specialized storage and transport. The commercial pipeline for advanced therapies is also raising the bar, as operators must demonstrate they can document every handoff and maintain temperature integrity throughout the full route in line with EU GDP requirements.

Nation-Wide Roll-Out of Germany's E-Prescription System (eRezept)

The Germany pharmaceutical logistics market is being reshaped by eRezept because prescription fulfillment is now more digital, faster, and easier to route into home delivery and mail-order channels. Germany crossed 1 billion cumulative eRezept redemptions on October 17, 2025, demonstrating how quickly the digital prescription system had scaled since the mandatory rollout began in 2024. This shift is changing the mix of shipments from larger scheduled wholesale drops toward higher-frequency parcel flows that still need GDP-compliant handling. It is also improving demand visibility because pharmacy and prescription data are now available much earlier in the ordering cycle than they were in the paper-based model. That earlier signal allows logistics operators and specialty pharmacies to pre-position stock nearer to high-demand urban districts and reduce replenishment lead times. The Germany pharmaceutical logistics market is therefore seeing stronger value in warehouse management systems that can connect prescription data with stock planning, route scheduling, and temperature-specific inventory allocation.

Escalating Energy Costs for Cold-Chain Warehousing

The Germany pharmaceutical logistics market remains exposed to high energy prices because cold-chain warehouses consume far more electricity than ambient facilities. Germany continues to have some of the highest industrial power costs in Europe, placing a direct burden on operators of refrigerated and frozen pharmaceutical sites. This cost issue is becoming more serious as facilities also prepare for refrigerant transition requirements, which add capital spending for low-GWP systems and related equipment upgrades. A reported example from the sector showed that switching to a blended power procurement model with wind PPA exposure reduced costs and avoided 1,900 tons of CO2 in one reporting period. Even so, hedging and energy transition programs compete for the same capital that operators need for GDP upgrades, monitoring systems, and new cold rooms. The Germany pharmaceutical logistics market, therefore, gives a clear edge to providers with stronger balance sheets, because they can fund energy adaptation and compliance investment at the same time.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Enforcement of EU GDP 2022/993 Compliance Audits

- Growth of Specialty Pharmacies Pushing Same-Day Delivery Models

- Shortage of GDP-Certified Drivers and Warehouse Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 58.14% of Germany pharmaceutical logistics market share in 2025, which kept it as the largest logistics function in the Germany pharmaceutical logistics market. Road distribution remained the core because Germany's pharmacy, hospital, wholesale, and manufacturing networks require dense domestic coverage and frequent replenishment runs. Air freight kept its role in high-value and time-critical shipments such as advanced therapies, clinical trial materials, and short-stability biologics that need rapid airport-to-care-site movement. Rail and sea-linked flows remained more relevant for import-side handling of bulk materials and selected upstream pharmaceutical inputs.

Warehousing and distribution continued to hold a stable middle position because GDP-certified multi-temperature sites near Autobahn corridors are still central to national service design. The fastest shift came from value-added services, which are projected to expand at a 6.55% CAGR and therefore show the fastest growth in the Germany pharmaceutical logistics market through 2031. Pharmaceutical shippers are increasingly outsourcing serialization aggregation, returns control, deviation handling, artwork support, and patient-specific kitting to providers that can combine compliance systems with physical handling. DHL's EUR 2 billion (USD 2.35 billion) investment in the health logistics underlined how strongly large operators are backing clinical, biopharma, and advanced therapy support services inside the Germany pharmaceutical logistics market.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North Rhine-Westphalia

- Bavaria (Bayern)

- Baden-Wurttemberg

- Rest of States

List of Companies Covered in this Report:

- DHL Group

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- United Parcel Service of America, Inc. (UPS)

- FedEx

- World Courier

- NYK Line (Including Yusen Logistics)

- CMA CGM Group (Including CEVA Logistics)

- GEODIS

- DACHSER

- Hellmann Worldwide Logistics

- Fiege Logistics

- Cencora

- LOXXESS Pharma

- UNITAX-PHARMALOGISTIK GMBH

- PharmLog Pharma Logistik GmbH

- Transpharm Logistik GmbH

- Pharmaserv GmbH and Co. KG

- Arvato SE

- Lufthansa Cargo

- Noerpel Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Expanding Biologics and Biosimilars Pipeline Adoption

- 4.3.2 Nation-Wide Roll-Out of Germany's E-Prescription System (eRezept)

- 4.3.3 Stringent Enforcement of EU GDP 2022/993 Compliance Audits

- 4.3.4 Growth of Specialty Pharmacies Pushing Same-Day Delivery Models

- 4.3.5 Hydrogen-Powered Temperature-Controlled Truck Pilots on Autobahn

- 4.3.6 Blockchain-Enabled Serialization Pilots Beyond FMD Mandates

- 4.4 Market Restraints

- 4.4.1 Escalating Energy Costs for Cold-Chain Warehousing

- 4.4.2 Complex Multi-Agency Permitting for Last-Mile Urban Deliveries

- 4.4.3 Shortage of GDP-Certified Drivers and Warehouse Technicians

- 4.4.4 Limited Regulatory Pathways for Medical-Grade Drone Corridors

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North Rhine-Westphalia

- 5.4.2 Bavaria (Bayern)

- 5.4.3 Baden-Wurttemberg

- 5.4.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne+Nagel

- 6.4.3 DSV A/S (Including DB Schenker)

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 FedEx

- 6.4.6 World Courier

- 6.4.7 NYK Line (Including Yusen Logistics)

- 6.4.8 CMA CGM Group (Including CEVA Logistics)

- 6.4.9 GEODIS

- 6.4.10 DACHSER

- 6.4.11 Hellmann Worldwide Logistics

- 6.4.12 Fiege Logistics

- 6.4.13 Cencora

- 6.4.14 LOXXESS Pharma

- 6.4.15 UNITAX-PHARMALOGISTIK GMBH

- 6.4.16 PharmLog Pharma Logistik GmbH

- 6.4.17 Transpharm Logistik GmbH

- 6.4.18 Pharmaserv GmbH and Co. KG

- 6.4.19 Arvato SE

- 6.4.20 Lufthansa Cargo

- 6.4.21 Noerpel Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment