PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072844

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072844

China Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

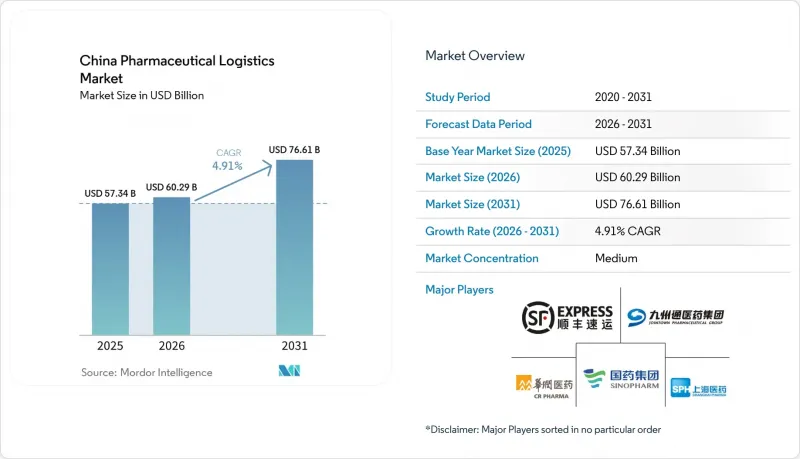

According to Mordor Intelligence, the china pharmaceutical logistics market size is projected to be USD 57.34 billion in 2025, USD 60.29 billion in 2026, and reach USD 76.61 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

The market is supported by steady demand for medicines from an aging population, a large domestic pharmaceutical production base, and a policy system that links distribution quality more directly to drug safety and service consistency. This report is Segmented by Logistics Function (Transportation, Warehousing and Distribution, Value-Added Services), by Mode of Operation (Cold-Chain, Non-Cold-Chain), by Product Type (Prescription Drugs, OTC, Biologics, Vaccines, Clinical Trial Materials, Cell and Gene Therapies, Medical Devices, Veterinary Medicine), and by Region (North, Northeast, and More). The Market Forecasts are in Value (USD).

China Pharmaceutical Logistics Market Trends and Insights

Expansion of the National Essential-Drug Distribution Network

The updated 2025 National Basic Medical Insurance Drug Directory widened the reimbursed product base and, for the first time, added a commercial health insurance category for innovative drugs, which directly increases the flow of covered medicines through licensed distribution channels. That change matters for the China pharmaceutical logistics market because reimbursed access expands throughput at both the hospital and retail ends of the chain. It underscores the need for additional ambient capacity, but also for qualified cold-chain infrastructure as innovative therapies enter broader circulation. The policy direction under the 15th Five-Year Plan also supports larger national distributors, which strengthens scale advantages in compliance, route density, and procurement execution. For the China pharmaceutical logistics market, the result is a larger national flow base paired with a higher minimum service standard. Smaller operators that cannot fund traceability, serialization, and temperature-controlled assets are therefore under more pressure as the distribution network broadens.

Rapid Growth in Biologics and Temperature-Controlled Demand

Biologics and other temperature-sensitive products are shifting the operating center of the China pharmaceutical logistics market, as they require tighter controls, stronger validation, and more robust exception management than ambient generics. Pharmaceutical cold-chain logistics costs in China reached CNY 26.78 billion (USD 3.79 billion) in 2025, while cold storage capacity rose 5.43% to 4.525 million cubic meters, a faster rate than growth in ambient warehousing. The technical shift is even greater in the cell and gene therapy lanes, where transport can shift from the established 2 °C to 8 °C range toward cryogenic conditions of -150 °C to -196 °C for certain products. That requirement narrows the field to operators with specialized equipment, validated handling protocols, and staff training that general freight firms do not usually maintain. It also allows qualified providers to defend higher pricing than they can in ambient, procurement-led flows. In the China pharmaceutical logistics market, this pushes capital toward premium cold-chain corridors even when broader price pressure affects standard medicine distribution.

Fragmented Rural Last-Mile Infrastructure

Rural last-mile weakness remains one of the clearest operating limits in the China pharmaceutical logistics market. China's pharmaceutical vehicle fleet reached 46,416 units in 2025, but investment still clustered around stronger urban corridors, which left lower-tier markets with thinner certified capacity and less route redundancy. That imbalance matters more in western and mountainous provinces, where road-only delivery can conflict with temperature stability windows and time-sensitive replenishment needs. A 2025 Frontiers in Public Health study also showed that access to essential medicines still varies across regions, with socio-economic conditions continuing to shape actual availability despite broad policy efforts. Providers serving centralized procurement contracts in rural areas often face underpriced last-mile costs, which reduces the funds available for asset upgrades and service expansion. Drone pilots in Hainan, Yunnan, Xinjiang, and Chongqing show that the constraint can be reduced, but the China pharmaceutical logistics market still lacks broad commercial coverage in many difficult inland routes.

Other drivers and restraints analyzed in the detailed report include:

- Rise of E-Commerce Pharmacies and 24-Hr Delivery Expectations

- Stricter GDP Audit and Licensing Enforcement

- Escalating Cold-Chain Energy Costs Under Carbon Caps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation held 52.46% of the China pharmaceutical logistics market share in 2025, making it the largest functional segment across the operating chain. The segment's scale reflects the central role of road movement in intercity transfers, urban replenishment, hospital delivery, and pharmacy restocking. Air freight remains relevant for urgent biologics, high-value samples, and selected clinical shipments where speed and temperature control matter more than cost. Inland waterway and sea transport still support bulk ambient flows in selected corridors where delivery windows are less strict, and unit economics favor larger-volume movement. Total warehousing capacity reached 93.816 million cubic meters in 2025, which shows that the transport layer continues to work in close coordination with a large national storage base.

The second half of this segment tells a different story, because value-added services are forecast to grow at a 7.74% CAGR through 2031 and are now becoming central to differentiation. Pharmaceutical manufacturers increasingly want third parties to handle serialization, GDP-compliant temperature monitoring, DTP pharmacy fulfillment, and cold-chain-as-a-service instead of building those capabilities alone. That shift changes the economics of the China pharmaceutical logistics industry, because margins move away from pure transport yield and toward compliance-heavy service overlays. SF Holding's formal creation of a supply chain business group for life sciences and pharmaceuticals in late 2025 reflects that repositioning and helped drive more than 20% revenue growth in the vertical. Warehousing and distribution therefore remain important as a stable middle layer, but growth is increasingly tied to digital integration, validated handling, and outsourced service depth rather than storage space alone.

Complete Report Scope:

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services and Others

- Transportation

- By Mode of Operation

- Cold-Chain Logistics

- Non-Cold-Chain Logistics

- By Product Type

- Prescription Drugs

- OTC Drugs

- Biologics and Biosimilars

- Vaccines and Blood Products

- Clinical Trail Materials

- Cell and Gene Therapies

- Medical Devices and Diagnostics

- Veterinary Medicine

- Others

- By Region

- North

- Northeast

- East

- Central

- South

- Southwest

- Northwest

List of Companies Covered in this Report:

- Sinopharm Logistics

- SF Express

- JD Logistics

- DHL Group

- United Parcel Service of America, Inc. (UPS)

- Kuehne+Nagel

- DSV A/S (Including DB Schenker)

- FedEx

- Cencora

- CJ Rokin Logistics

- Nippon Express Holdings

- Yamato Holdings

- ZTO Express

- YTO Express

- STO Express

- China Post EMS

- Cainiao Smart Logistics Network

- CMA CGM Group (Including CEVA Logistics)

- DCH Auriga

- Sinotrans Limited

- China Resources Pharmaceutical Commercial

- Jointown Pharmaceutical Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Logistics in Pharmaceutical

- 4.2 Pharmaceutical Spending Trends

- 4.3 Market Drivers

- 4.3.1 Expansion of the National Essential-Drug Distribution Network

- 4.3.2 Rapid Growth in Biologics and Temperature-Controlled Demand

- 4.3.3 Rise of E-Commerce Pharmacies and 24-Hr Delivery Expectations

- 4.3.4 Stricter GDP Audit and Licensing Enforcement

- 4.3.5 Centralized-Procurement Hubs Drive Regional Consolidation

- 4.3.6 Pilots of Drones/AVs for Western-Province Mid-Mile Routes

- 4.4 Market Restraints

- 4.4.1 Fragmented Rural Last-Mile Infrastructure

- 4.4.2 Escalating Cold-Chain Energy Costs Under Carbon Caps

- 4.4.3 Dry-Ice Supply Rules for MRNA Vaccines

- 4.4.4 Urban Hospital Traffic-Control Delivery Curfews

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Pharmaceutical Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics and Biosimilars

- 5.3.4 Vaccines and Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell and Gene Therapies

- 5.3.7 Medical Devices and Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Northeast

- 5.4.3 East

- 5.4.4 Central

- 5.4.5 South

- 5.4.6 Southwest

- 5.4.7 Northwest

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Sinopharm Logistics

- 6.4.2 SF Express

- 6.4.3 JD Logistics

- 6.4.4 DHL Group

- 6.4.5 United Parcel Service of America, Inc. (UPS)

- 6.4.6 Kuehne+Nagel

- 6.4.7 DSV A/S (Including DB Schenker)

- 6.4.8 FedEx

- 6.4.9 Cencora

- 6.4.10 CJ Rokin Logistics

- 6.4.11 Nippon Express Holdings

- 6.4.12 Yamato Holdings

- 6.4.13 ZTO Express

- 6.4.14 YTO Express

- 6.4.15 STO Express

- 6.4.16 China Post EMS

- 6.4.17 Cainiao Smart Logistics Network

- 6.4.18 CMA CGM Group (Including CEVA Logistics)

- 6.4.19 DCH Auriga

- 6.4.20 Sinotrans Limited

- 6.4.21 China Resources Pharmaceutical Commercial

- 6.4.22 Jointown Pharmaceutical Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment