PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072967

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072967

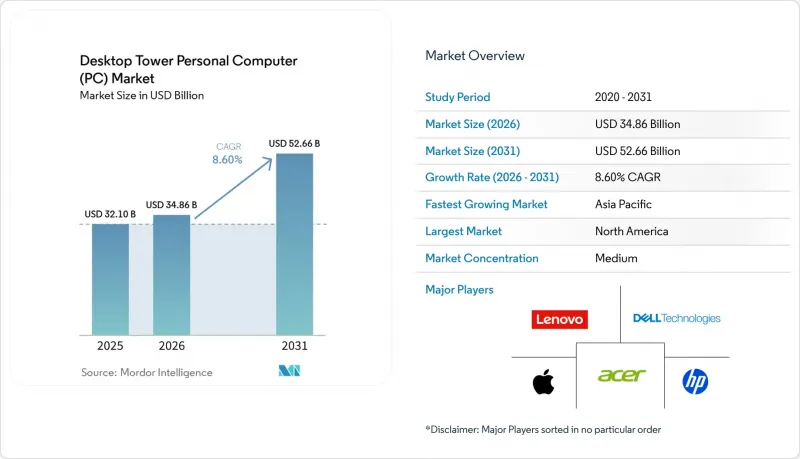

Desktop Tower Personal Computer (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the desktop tower personal computer(PC) market size is projected to be USD 34.86 billion in 2026 and reach USD 52.66 billion by 2031, growing at an 8.60% CAGR over 2026-2031.

This report is Segmented by Form Factor (Full-Tower, Mid-Tower, Mini-Tower, Small Form Factor), Processor Vendor (Intel-Based, AMD-Based, ARM-Based, Other), End User (Gaming, Enterprise, Home, and More), Price Band (Entry, Mid-Range, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Desktop Tower Personal Computer (PC) Market Trends and Insights

Growing Demand for High-Performance Gaming Rigs

Desktop tower gaming PCs retained 73.4% share of the gaming PC universe in 2025 because multi-GPU support and liquid-cooling compatibility still outclass laptop thermals. Esports operators require standardized mid- or full-tower footprints to simplify servicing, as seen in T1's 120-location PC-cafe network across Asia-Pacific. Intel's Arrow Lake Refresh CPUs, launched in March 2026, added efficiency cores and native DDR5-7200 support to lift gaming frame rates by up to 15% in tower builds. AMD's Zen 5 refresh, expected later in 2026, further raises competitive pressure, forcing tower OEMs to diversify SKUs and hold higher inventories while catering to enthusiasts' appetite for frequent upgrades.

Enterprise Refresh Cycles Post-Pandemic

Deferred upgrades from 2020-2022 unleashed a synchronized refresh after Windows 10 support ended, with China's desktop shipments jumping to 42.1 million units in 2025 before normalizing in 2026. Enterprises fast-tracked towers carrying NPUs rated at 40 TOPS to cut cloud inference fees and address sovereignty mandates. Dell's Client Solutions Group pivoted by integrating NVIDIA's RTX PRO Blackwell GPUs inside tower workstations that promise 12x faster vector indexing versus legacy setups. Lenovo seized share in China through localized supply and 3-year on-site service contracts, highlighting how tower reliability still underpins large-fleet deployments.

Substitution Threat from High-End Gaming Laptops

Gaming laptops accounted for 26.6% of gaming-PC volumes in 2025 and are projected to grow at a 15.4% CAGR, driven by advancements in mobile GPUs that now deliver 80%-85% of tower performance. This trend is particularly prominent in space-constrained Asian households, where portability and compact designs are highly valued. Dell's XPS 16, for instance, offers 27 hours of Netflix playback on a single charge, reshaping consumer perceptions from viewing laptops as a compromise to recognizing them as a value-added bundle. In response, tower vendors emphasize features like tool-less expandability and multi-GPU configurations, which primarily appeal to gaming enthusiasts. However, entry-level towers face challenges in maintaining market share, especially in regions where competitive laptop pricing has compressed the value gap.

Other drivers and restraints analyzed in the detailed report include:

- Declining Average Selling Prices of Discrete GPUs

- Expansion of Esports Venues and LAN Cafes in Emerging Economies

- Supply Chain Volatility for Critical Semiconductors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Small form factor towers captured 8.5% of the desktop tower PC market in 2025 and will outstrip the overall 8.60% market CAGR by growing 10.40% through 2031. The segment benefits from a tool-less chassis that integrates snap-fit panels and cable channels, enabling first-time builders to finish assembly in under 30 minutes. Mid-towers remain indispensable for enterprise fleets because IT departments favor standardized layouts and can deploy hot-swappable drive cages that reduce downtime. Full-tower systems, while niche, house 360 mm radiators and 1,600-watt PSUs that premium AI rigs require, ensuring continued demand among creators and AI researchers who need multi-GPU slots.

Corsair, NZXT, and Lian Li are pushing chassis kits that include pre-installed RGB strips and reversible front panels, expanding the small-form-factor addressable market beyond enthusiasts. Dell debuted a fanless Pro Desktop tower aimed at healthcare cleanrooms, proving how compact designs can meet specialized acoustic or particulate-control specs. Improved vapor-chamber baseplates and graphene thermal pads mitigate airflow constraints, allowing 200-watt GPUs inside sub-13-liter cases without throttling. Collectively, these advances reinforce why compact towers will keep gaining share within the broader desktop tower PC market.

Intel-based systems still hold the dominant 70.90% share, yet ARM-based towers are scaling fastest at 12.60% CAGR because Snapdragon X Elite integrates 45 TOPS NPUs that run local LLMs without discrete accelerators. Qualcomm cornered roughly 10% of the over-USD 800 bracket by late 2025 via ASUS, Dell, and Lenovo partnerships. Intel's Arrow Lake Refresh restored some momentum by offering 24 cores for USD 299, a cores-per-dollar pitch that resonates with enterprise tower buyers who value multi-threaded throughput. AMD counters with Ryzen 9850X3D inside Alienware's Area-51 Desktop, harnessing 3D V-Cache for gaming-first latency gains.

The desktop tower PC market size for ARM towers remains relatively small; however, advancements in power efficiency and integrated AI co-processors are driving significant changes in the market. These developments are pressuring x86 incumbents to accelerate their refresh cycles to remain competitive. Tower OEMs that provide processor flexibility within a single chassis SKU are better positioned to address fluctuating demand while meeting the diverse needs of enterprises. This approach enables them to secure fleet-wide service contracts across varying CPU architectures, which is becoming increasingly important for multinational corporations. Additionally, the growing adoption of ARM-based towers highlights a shift in enterprise preferences, emphasizing the need for innovation and adaptability in the market.

Complete Report Scope:

- By Form Factor

- Full-Tower

- Mid-Tower

- Mini-Tower

- Small Form Factor

- By Processor Vendor

- Intel-Based Systems

- AMD-Based Systems

- ARM-Based Systems

- Other Architectures

- By End User

- Gaming Consumers

- Enterprise and Corporate

- Government and Education

- Home and Personal

- By Price Band

- Entry-Level

- Mid-Range

- High-End

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific will exhibit the quickest 9.40% CAGR as esports arenas multiply and disposable incomes climb, especially in India, Indonesia, and Vietnam. China's shipments spiked in 2025 because corporate buyers front-loaded refreshes, then retreated 10% in 2026 as pent-up demand normalized. Japan logged 90,000 desktop tower units in January 2026, more than doubling year over year, illustrating that tower adoption can remain healthy in mature markets when corporate fleets refresh.

North America, at 28.80% share, benefits from cybersecurity mandates that favor tower endpoints with removable storage and BIOS-level controls. DIY culture supports vibrant custom-builder ecosystems, sustaining higher-margin sales for Corsair, NZXT, and CyberPowerPC. Europe is wrestling with tighter Ecodesign rules. Standby-power caps at 0.5 watts and pending recycled-content directives require PSU and chassis redesigns that elevate engineering costs. Vendors are amortizing these investments globally, marginally lifting ASPs in every region.

South America is smaller but benefits from Brazil's local assembly incentives, though grey-market parts erode brand premiums. The Middle East's entertainment diversification fuels tower deployments in esports venues, with turnkey service contracts raising switching costs and locking in vendor relationships. Africa remains nascent, constrained by import duties and patchy power infrastructure, yet pockets of demand are emerging in tech hubs like Nairobi and Lagos where co-working spaces host gaming events that prefer towers over laptops for reliability.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Acer Inc.

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- Apple Inc.

- Corsair Gaming, Inc.

- Falcon Northwest Computer Systems Inc.

- Maingear, Inc.

- NZXT, Inc.

- CyberPowerPC (CyberPower, Inc.)

- iBUYPOWER (HSI, Inc.)

- Origin PC Corp.

- Digital Storm Online Systems, Inc.

- Velocity Micro, Inc.

- Puget Systems, Inc.

- Zotac Technology Limited

- Huawei Technologies Co., Ltd.

- Shenzhou Computer Co., Ltd. (Hasee)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for High-Performance Gaming Rigs

- 4.2.2 Enterprise Refresh Cycles Post-Pandemic

- 4.2.3 Declining Average Selling Prices of Discrete GPUs

- 4.2.4 Expansion of Esports Venues and LAN Cafes in Emerging Economies

- 4.2.5 Adoption of AI-Optimised Workstations in SMB Segment

- 4.2.6 Modular and Tool-Less Chassis Innovations Reducing Upgrade Friction

- 4.3 Market Restraints

- 4.3.1 Substitution Threat from High-End Gaming Laptops

- 4.3.2 Supply Chain Volatility for Critical Semiconductors

- 4.3.3 Rising Energy-Efficiency Regulations in Europe

- 4.3.4 Grey-Market Component Imports Undermining Branded PCs

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form Factor

- 5.1.1 Full-Tower

- 5.1.2 Mid-Tower

- 5.1.3 Mini-Tower

- 5.1.4 Small Form Factor

- 5.2 By Processor Vendor

- 5.2.1 Intel-Based Systems

- 5.2.2 AMD-Based Systems

- 5.2.3 ARM-Based Systems

- 5.2.4 Other Architectures

- 5.3 By End User

- 5.3.1 Gaming Consumers

- 5.3.2 Enterprise and Corporate

- 5.3.3 Government and Education

- 5.3.4 Home and Personal

- 5.4 By Price Band

- 5.4.1 Entry-Level

- 5.4.2 Mid-Range

- 5.4.3 High-End

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dell Technologies Inc.

- 6.4.2 HP Inc.

- 6.4.3 Lenovo Group Limited

- 6.4.4 Acer Inc.

- 6.4.5 ASUSTeK Computer Inc.

- 6.4.6 Micro-Star International Co., Ltd.

- 6.4.7 Apple Inc.

- 6.4.8 Corsair Gaming, Inc.

- 6.4.9 Falcon Northwest Computer Systems Inc.

- 6.4.10 Maingear, Inc.

- 6.4.11 NZXT, Inc.

- 6.4.12 CyberPowerPC (CyberPower, Inc.)

- 6.4.13 iBUYPOWER (HSI, Inc.)

- 6.4.14 Origin PC Corp.

- 6.4.15 Digital Storm Online Systems, Inc.

- 6.4.16 Velocity Micro, Inc.

- 6.4.17 Puget Systems, Inc.

- 6.4.18 Zotac Technology Limited

- 6.4.19 Huawei Technologies Co., Ltd.

- 6.4.20 Shenzhou Computer Co., Ltd. (Hasee)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment