PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073071

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073071

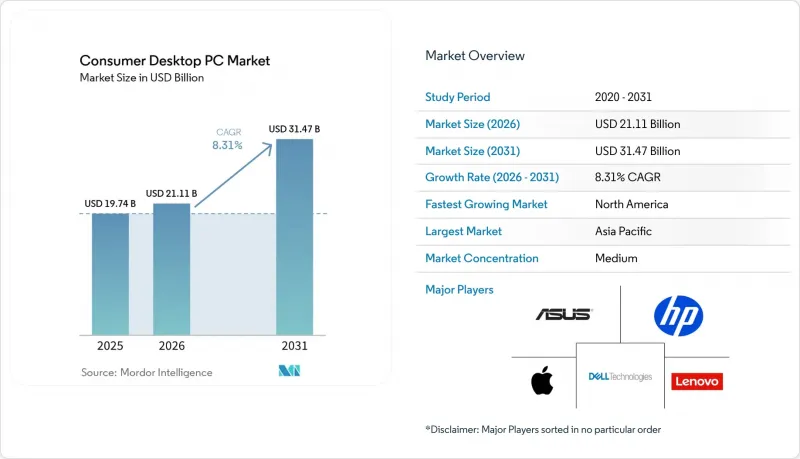

Consumer Desktop PC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the consumer desktop PC market size is projected to be USD 19.74 billion in 2025, USD 21.11 billion in 2026, and reach USD 31.47 billion by 2031, growing at a CAGR of 8.31% from 2026 to 2031.

This report is Segmented by Form Factor (Tower/Traditional Desktop, All-In-One, and More), Processor Architecture (x86, ARM, and RISC-V), Price Band (Entry-Level, Mid-Range, and Premium), End-User Industry (Home Users, Gamers, and More), Sales Channel (Online Retail, Offline Retail, Direct-To-Consumer, and Value-Added Resellers), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Consumer Desktop PC Market Trends and Insights

Windows 10 End-of-Support-Driven Replacement Cycle

Microsoft terminated mainstream support for Windows 10 in October 2025, leaving over 1 billion consumer and enterprise devices vulnerable to rising Extended Security Update fees. This shift has prompted many enterprises, particularly those with stringent compliance requirements, to expedite their hardware refresh cycles. These organizations aim to avoid the escalating security surcharges, which are set to double annually, by transitioning to serviceable tower desktops that allow for easier component replacements. The resulting surge in device replacements is expected to peak through 2026 before gradually declining. However, this trend is already driving significant growth in the market, with North America and Western Europe experiencing the most notable impact.

Rising Demand for High-Performance Gaming PCs

NVIDIA's RTX 5090, priced at USD 1,999, and RTX 5070, available at USD 549, have established new performance benchmarks for 4K and 8K gaming, catering to high-end gaming enthusiasts. Similarly, AMD's Radeon RX 9070 XT, priced at USD 649, has made AI-enhanced upscaling technology more accessible to a broader audience. The growing popularity of esports venues in South Korea and Japan, along with the increasing demand for streaming workstations capable of encoding 4K60 video, continues to drive consumers toward desktops equipped with multi-slot GPUs and advanced cooling systems. Furthermore, the global ITX gaming case segment, projected to reach USD 745 million by 2025, underscores the ongoing trend toward compact yet high-performance gaming rigs.

Rising Component Costs Due to Memory Realignment

DRAM prices surged 171% year-over-year in 2025, driven by fabricators reallocating production capacity to high-bandwidth modules for AI servers. This shift in focus has led memory to now account for 35% of the total bill of materials for a typical desktop. As a result, OEMs are facing tighter profit margins, and rising costs have pushed the prices of entry-level desktop systems above USD 650 in several emerging economies, making affordability a growing concern in these markets.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Adoption of AI-Capable Desktops for On-Device Processing

- Growth in Remote and Hybrid Work Models Sustaining Desktop Demand

- Intensifying Competition from High-End Laptops with Desktop-Class Performance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tower and traditional systems accounted for 48.32% of the consumer desktop PC market share in 2025. However, mini and small-form-factor models are projected to grow at a compound annual growth rate (CAGR) of 10.21%. Urban buyers in cities like Tokyo, Seoul, and Shanghai increasingly prefer compact designs due to space constraints and aesthetic preferences. The latest mini-ITX motherboards have advanced to support flagship CPUs and dual-slot GPUs without experiencing thermal throttling, making them a viable option for high-performance computing in smaller setups.

ASUS's relaunch of the Intel NUC range and the growing popularity of boutique gaming rigs featuring tempered-glass micro-ATX cases further highlight this trend. On the other hand, all-in-one desktops continue to face challenges due to their perceived lack of upgradeability, which limits their appeal to specific enterprise niches where maintaining clean and organized workspaces is prioritized over lifecycle flexibility. Meanwhile, workstation towers remain a lucrative high-margin segment, particularly for CAD and 3D rendering applications, driven by the performance capabilities of Threadripper PRO and Xeon W CPUs.

The consumer desktop PC market for x86 machines significantly outperformed alternatives in 2025, maintaining its dominance. However, ARM-based desktops are projected to grow at a robust 9.12% CAGR, driven by strategic government initiatives in countries like China and India. These nations are implementing procurement incentives, offering up to 20% of bid value to promote the adoption of homegrown silicon. Notable players such as Loongson, with its 3C6000 processors, and Zhaoxin, with its KX-7000 series, have already secured early government contracts, demonstrating their market potential. Additionally, advancements in Windows on ARM, particularly in x86 emulation, are addressing compatibility concerns, making these systems more appealing to buyers in sectors like education and civil service.

Despite these advancements, broader commercial adoption of ARM-based desktops remains contingent on the development and maturity of the software ecosystem. Nevertheless, the growth of ARM highlights a deliberate effort by governments and industries to achieve supply-chain sovereignty and reduce reliance on external technologies. Meanwhile, RISC-V architecture, though promising, is still in its prototype phase, with no mass-market desktop launch expected before 2029. This delay limits its immediate influence on the desktop PC market, keeping its impact minimal in the short term.

Complete Report Scope:

- By Form Factor

- Tower / Traditional Desktop

- All-in-One (AIO)

- Mini / Small Form Factor

- Gaming / Performance Rigs

- Workstation Desktops

- By Processor Architecture

- x86

- ARM

- RISC-V

- By Price Band

- Entry-Level (USD 1,200)

- By End-User Industry

- Home Users

- Gamers

- Professionals & Creators

- Small & Medium Businesses

- Enterprises

- By Sales Channel

- Online Retail

- Offline Retail

- Direct-to-Consumer

- Value-Added Resellers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific is on course for an 8.94% CAGR through 2031, supported by India's INR 170 billion (approximately USD 2.05 billion) incentive program for IT hardware and China's USD 70 billion AI and chip subsidy package. Production footprints in Tamil Nadu and Karnataka expand sharply as Foxconn and Flex localize assembly to capture duty benefits. Municipal procurement policies in China, granting a 20% price advantage to domestic CPUs, accelerate ARM desktop adoption in government offices.

North America remains the largest single market, with a 42.84% share in 2025. Section 301 tariffs on Chinese semiconductors were raised to 50% in late 2024, prompting inventory pulls, but ongoing diversification into Mexico and Vietnam eases longer-term risk. Hybrid work patterns are driving demand for home-office towers that pair multi-monitor support with local AI acceleration. Europe ranks second by revenue. EU Ecodesign mandates taking effect in 2027 will raise power-supply costs, yet sustainability labeling could steer eco-conscious consumers toward desktops that promise lower standby draws. Regional gaming hubs in Germany, Poland, and the Nordics continue to see steady upgrades as 240 Hz monitors proliferate.

South America is highly price-sensitive and remains susceptible to fluctuations in foreign exchange rates. However, a niche market of enthusiasts in Brazil continues to support a modest yet resilient boutique-builder scene, catering to specific consumer demands. Meanwhile, the Middle East and Africa are still in the early stages of market development, with procurement efforts primarily focused on public-sector digitization initiatives. These include Saudi Vision 2030, which aims to diversify the economy and enhance public services, and the UAE Smart Government initiatives, which focus on leveraging technology to improve governance and citizen engagement.

- Lenovo Group Limited

- HP Inc.

- Dell Technologies Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Acer Inc.

- Micro-Star International Co., Ltd.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Fujitsu Limited

- NEC Corporation

- Tongfang Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Zotac International (M) Limited

- Razer Inc.

- Corsair Gaming, Inc.

- Origin PC Corporation

- CyberPowerPC Inc.

- System76, Inc.

- Shuttle Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Windows 10 End-of-Support-Driven Replacement Cycle (2025-2027)

- 4.2.2 Rising Demand for High-Performance Gaming PCs

- 4.2.3 Growth in Remote and Hybrid Work Models Sustaining Desktop Demand

- 4.2.4 Enterprise Adoption of AI-Capable Desktops for On-Device Processing

- 4.2.5 Government Subsidies for Domestic CPU Ecosystems Boosting ARM-Based Desktops in Asia

- 4.2.6 Surge in Creative Workstation Builds Fueled by Generative Content Workflows

- 4.3 Market Restraints

- 4.3.1 Rising Component Costs Due to Memory Supply Shift to AI Servers

- 4.3.2 Intensifying Competition from High-End Laptops with Desktop-Class Performance

- 4.3.3 Import Tariff Volatility Prompting Inventory Distortions in North America

- 4.3.4 Limited Upgradeability Perception Deterring Adoption of All-in-One Desktops

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form Factor

- 5.1.1 Tower / Traditional Desktop

- 5.1.2 All-in-One (AIO)

- 5.1.3 Mini / Small Form Factor

- 5.1.4 Gaming / Performance Rigs

- 5.1.5 Workstation Desktops

- 5.2 By Processor Architecture

- 5.2.1 x86

- 5.2.2 ARM

- 5.2.3 RISC-V

- 5.3 By Price Band

- 5.3.1 Entry-Level (<USD 600)

- 5.3.2 Mid-Range (USD 600- USD 1,200)

- 5.3.3 Premium (>USD 1,200)

- 5.4 By End-User Industry

- 5.4.1 Home Users

- 5.4.2 Gamers

- 5.4.3 Professionals & Creators

- 5.4.4 Small & Medium Businesses

- 5.4.5 Enterprises

- 5.5 By Sales Channel

- 5.5.1 Online Retail

- 5.5.2 Offline Retail

- 5.5.3 Direct-to-Consumer

- 5.5.4 Value-Added Resellers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Lenovo Group Limited

- 6.4.2 HP Inc.

- 6.4.3 Dell Technologies Inc.

- 6.4.4 Apple Inc.

- 6.4.5 ASUSTeK Computer Inc.

- 6.4.6 Acer Inc.

- 6.4.7 Micro-Star International Co., Ltd.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Fujitsu Limited

- 6.4.11 NEC Corporation

- 6.4.12 Tongfang Co., Ltd.

- 6.4.13 Gigabyte Technology Co., Ltd.

- 6.4.14 Zotac International (M) Limited

- 6.4.15 Razer Inc.

- 6.4.16 Corsair Gaming, Inc.

- 6.4.17 Origin PC Corporation

- 6.4.18 CyberPowerPC Inc.

- 6.4.19 System76, Inc.

- 6.4.20 Shuttle Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment