PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073076

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073076

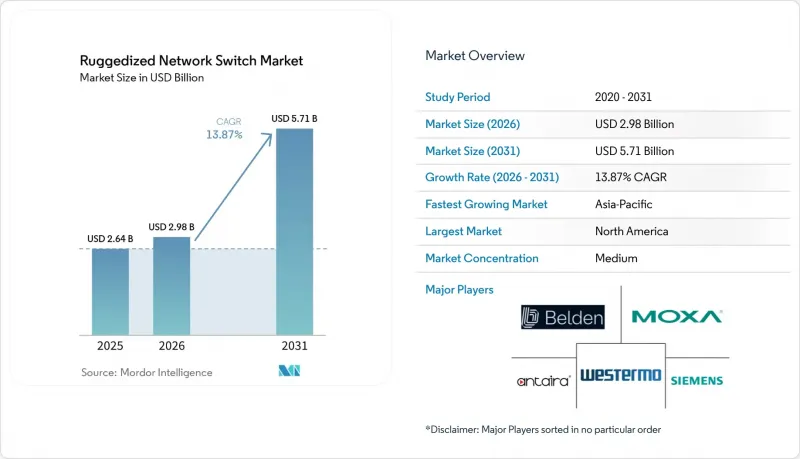

Ruggedized Network Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the ruggedized network switch market size is projected to expand from USD 2.64 billion in 2025 and USD 2.98 billion in 2026 to USD 5.71 billion by 2031, registering a CAGR of 13.87% between 2026 and 2031.

This report is Segmented by Management Type (Managed Ruggedized Switches, and Unmanaged Ruggedized Switches), Port Speed (1 GbE and Below, 2. 5/5 GbE, and More), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Installation Type (DIN-Rail Mounted, and More), End-User Industry (Industrial, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Ruggedized Network Switch Market Trends and Insights

Integration of Time-Sensitive Networking Standards

TSN protocols, notably IEEE 802.1AS for time synchronization and 802.1Qbv for traffic scheduling, enable deterministic Ethernet that replaces proprietary fieldbus systems in factory automation. Siemens introduced TSN-enabled SCALANCE XM-400 switches that deliver sub-1 µs jitter, unlocking precision motion control on automotive assembly lines. The unified IEC/IEEE 60802 profile published in 2024 guarantees multi-vendor interoperability, lowering integration risk for plant operators IEC.CH. Moxa's EDS-4000 series couples TSN with IEC 62443-4-2 security to meet dual determinism and cyber-resilience requirements in critical infrastructure. In-vehicle Ethernet adoption for battery management and advanced driver-assistance systems extends TSN demand into the transportation backbone.

Expansion of Rail Transit Infrastructure Worldwide

China already operates 46,000 km of high-speed rail and targets 70,000 km by 2035, each trainset requiring EN 50155-graded switches for passenger information, signaling, and diagnostics. India has 945 km of metro lines in service and more than 1,200 km under construction, including Delhi Metro Phase IV valued at INR 600 billion (USD 7.2 billion). Indonesia's Jakarta-Bandung route, operational since 2023, is spurring parallel projects across Southeast Asia. Mature markets are also refreshing installed bases; Scotland's 2026 audit listed 1,017 ruggedized IP switches due for end-of-life replacement. Middle-East megaprojects such as Riyadh Metro and Turkey's Bosphorus tunnel specify fanless, desert-rated switches to ensure reliability under extreme heat.

High Initial Capital Expenditure

Price premiums ranging from 300% to 500% over commercial Ethernet hardware discourage cash-constrained operators, even though failure rates and maintenance spending favor ruggedized equipment over a decade. Municipalities frequently defer switch upgrades despite the verified cyber threats flagged in Scotland's 2026 asset review. Small manufacturers often prolong legacy gear through patchwork firmware lifts rather than full refreshes, widening the cyber-exposure window. Although leasing models and subscription purchasing reduce initial outlay, their adoption outside large enterprises remains early stage. Bridging this funding gap is essential for broad-based market acceleration.

Other drivers and restraints analyzed in the detailed report include:

- Rising Defense Modernization Budgets

- Growing Demand for Edge Computing at the Rugged Edge

- Complex Certification and Compliance Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The managed tier seized 76.82% of 2025 revenue as operators adopted IEC 62443-4-2 security baselines, VLAN segmentation, and role-based authentication. This dominance continues, with a 14.22% CAGR that lifts the segment's ruggedized network switch market size throughout the forecast. Managed switches also anchor Time-Sensitive Networking rollouts, because 802.1Qbv and 802.1AS require centralized scheduling and clock distribution. Unmanaged models still serve isolated conveyor systems and brownfield sites, but the risk calculus is tilting firmly toward managed infrastructure. Vendors have responded with zero-touch provisioning and cloud dashboards that lower the skills barrier for smaller plants, helping managed penetration deepen across emerging economies.

Unmanaged devices retain tactical relevance where deterministic traffic, air-gapped architectures, or budget ceilings prevail. However, ransomware campaigns targeting industrial control systems and regulatory scrutiny under the European Union's Network and Information Security Directive 2 are pushing operators toward visibility and control. As managed functionality becomes table stakes, price erosion is narrowing the premium, further swinging preference in its favor.

Ports of 1 Gbps and below accounted for 47.36% of the installed base in 2025, but the 25 Gbps and 40 Gbps classes are expanding fastest at 18.73% through 2031 as edge modules process video analytics, digital-twin telemetry, and lidar streams. This speed tier accounts for the highest incremental ruggedized network switch market share gain in the period. Autonomous mining trucks generate several terabits daily, necessitating 25 Gbps uplinks between pit switches and surface hubs. The intermediate 2.5 Gbps and 5 Gbps lanes provide cost-effective upgrades over existing Cat5e cabling, bridging the gap without immediate fiber investment.

Ten-gigabit uplinks remain the workhorse for metro-rail Wi-Fi and smart-grid substations, balancing bandwidth with manageable thermal envelopes in fanless casings. Higher brackets, such as 100 Gbps and 400 Gbps, are technically feasible but hampered by heat dissipation and the scarcity of wide-temperature optics. Research into heat-pipe substrates and nano-porous coatings aims to ease these constraints, paving the way for the gradual introduction in offshore wind control rooms and forward command posts.

Complete Report Scope:

- By Management Type

- Managed Ruggedized Switches

- Unmanaged Ruggedized Switches

- By Port Speed

- 1 GbE and Below

- 2.5/5 GbE Multi-Gig

- 10 GbE

- 25/40 GbE

- 100 GbE

- 400 GbE and Above

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Installation Type

- DIN-Rail Mounted

- Rack-Mounted

- Embedded / Board-Level

- By End-User Industry

- Industrial

- Transportation

- Military and Defense

- Oil and Gas

- Mining and Metals

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America generated 35.92% of 2025 revenue due to the United States' USD 3.46 billion Grid Resilience program and Dominion Energy's USD 9.8 billion grid plan that rolled out thousands of IEC 61850-3 substations. Federal Highway Administration guidance issued in 2026 extends ruggedized equipment into temporary work-zone ITS, broadening addressable volume. Defense spending tied to the Joint Cyber Warfighting Architecture continues to favor locally sourced, MIL-STD-qualified vendors.

Asia-Pacific is the fastest growing, recording a 16.18% CAGR that builds on China's 70,000 km high-speed rail goal, India's metro pipeline, and Australia's automation-heavy mining sector. Japan and South Korea advance TSN-infused automotive lines and defense initiatives, while Indonesia's Jakarta-Bandung opening has nudged Thailand and Malaysia to progress their own corridors. Private 5G trials in ports across Singapore, Busan, and Ningbo require TSN-capable switches that interwork with RedCap radios.

Europe combines mature industrial estates with policy-driven digital infrastructure. The European Union's January 2026 delegated act mandates 5G underlay along Trans-European Transport Network corridors by 2030, accelerating roadside unit rollouts. Germany's automotive OEMs, Spain's metro clusters, Poland's freight-rail upgrades, and North Sea offshore wind farms all contribute diversified demand. Supply-chain sovereignty concerns are spurring localized production, such as ECRIN Systems' France-built Quartz switch. The Middle East pushes ruggedized switching into harsh desert metros and Gulf port expansions, while Latin America's mining and near-shoring factories provide steady, if smaller, opportunities. Africa remains nascent but shows traction in South African port automation and Nigerian free-trade-zone logistics.

- Moxa Inc.

- Westermo Network Technologies AB

- Antaira Technologies, LLC

- Belden Inc.

- Siemens AG

- Advantech Co., Ltd.

- RuggedCom Inc.

- EtherWAN Systems, Inc.

- Lantech Communications Global, Inc.

- ACKSYS Communications and Systems

- Kyland Technology Co., Ltd.

- Hirschmann Automation and Control GmbH

- Red Lion Controls, Inc.

- ORing Industrial Networking Corp.

- Trend Communications Ltd.

- Teldat Group S.A.

- GarrettCom, Inc.

- Perle Systems Limited

- Sealevel Systems, Inc.

- Weidmuller Interface GmbH & Co. KG

- Korenix Technology Co., Ltd.

- 3onedata Co., Ltd.

- B+B SmartWorx Inc.

- NETIO Products a.s.

- Crystal Group, Inc.

- Westek Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Industrial IoT in Harsh Environments

- 4.2.2 Growing Demand for Edge Computing at the Rugged Edge

- 4.2.3 Expansion of Rail Transit Infrastructure Worldwide

- 4.2.4 Rising Defense Modernization Budgets

- 4.2.5 Integration of Time-Sensitive Networking (TSN) Standards

- 4.2.6 Emergence of 5G-Enabled Rugged Edge Devices

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure

- 4.3.2 Complex Certification and Compliance Requirements

- 4.3.3 Supply Chain Vulnerabilities for Hardened Components

- 4.3.4 Thermal Management Challenges in Compact Designs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Management Type

- 5.1.1 Managed Ruggedized Switches

- 5.1.2 Unmanaged Ruggedized Switches

- 5.2 By Port Speed

- 5.2.1 1 GbE and Below

- 5.2.2 2.5/5 GbE Multi-Gig

- 5.2.3 10 GbE

- 5.2.4 25/40 GbE

- 5.2.5 100 GbE

- 5.2.6 400 GbE and Above

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Installation Type

- 5.4.1 DIN-Rail Mounted

- 5.4.2 Rack-Mounted

- 5.4.3 Embedded / Board-Level

- 5.5 By End-User Industry

- 5.5.1 Industrial

- 5.5.2 Transportation

- 5.5.3 Military and Defense

- 5.5.4 Oil and Gas

- 5.5.5 Mining and Metals

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Moxa Inc.

- 6.4.2 Westermo Network Technologies AB

- 6.4.3 Antaira Technologies, LLC

- 6.4.4 Belden Inc.

- 6.4.5 Siemens AG

- 6.4.6 Advantech Co., Ltd.

- 6.4.7 RuggedCom Inc.

- 6.4.8 EtherWAN Systems, Inc.

- 6.4.9 Lantech Communications Global, Inc.

- 6.4.10 ACKSYS Communications and Systems

- 6.4.11 Kyland Technology Co., Ltd.

- 6.4.12 Hirschmann Automation and Control GmbH

- 6.4.13 Red Lion Controls, Inc.

- 6.4.14 ORing Industrial Networking Corp.

- 6.4.15 Trend Communications Ltd.

- 6.4.16 Teldat Group S.A.

- 6.4.17 GarrettCom, Inc.

- 6.4.18 Perle Systems Limited

- 6.4.19 Sealevel Systems, Inc.

- 6.4.20 Weidmuller Interface GmbH & Co. KG

- 6.4.21 Korenix Technology Co., Ltd.

- 6.4.22 3onedata Co., Ltd.

- 6.4.23 B+B SmartWorx Inc.

- 6.4.24 NETIO Products a.s.

- 6.4.25 Crystal Group, Inc.

- 6.4.26 Westek Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment