PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073158

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073158

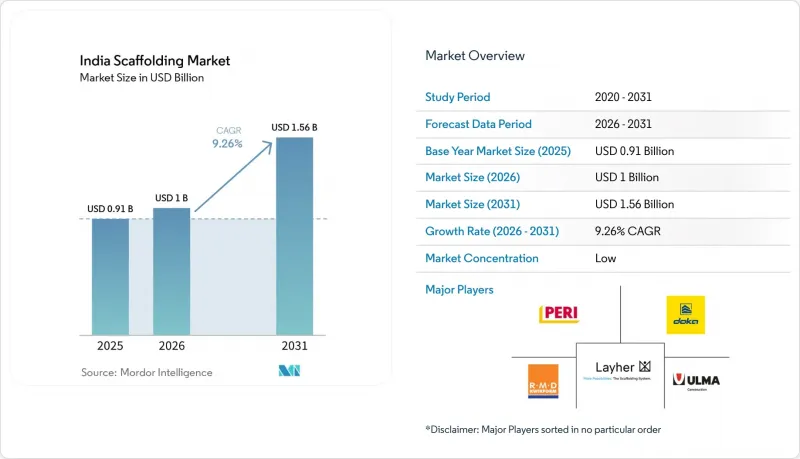

India Scaffolding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india scaffolding market size is expected to increase from USD 0.91 billion in 2025 to USD 1 billion in 2026 and reach USD 1.56 billion by 2031, growing at a CAGR of 9.26% over 2026-2031.

This report is Segmented by Type (Supported, Suspended, and Mobile Scaffold), System (Tube & Coupler, Cuplock, and More), Business Model (Sales and Rental), Material Type (Timber / Plywood, Steel, Aluminum, and More), Sector (Residential, Commercial, and More), and City (Mumbai Metropolitan Region, Delhi NCR, Pune, Bengaluru, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Scaffolding Market Trends and Insights

Rising Commercial and Infrastructure Construction Boosts Scaffolding Demand

Public capital spending gives the India scaffolding market a strong base over the forecast period. Union Budget 2026-27 raised capital expenditure to USD 145 billion, including USD 35 billion for road transport and highways, and USD 33 billion for railways. Housing construction remains active as well, with Pradhan Mantri Awas Yojana Urban 2.0 having sanctioned 1.36 million additional urban housing units by February 2026. The project mix is also getting heavier in data centers, metro structures, and large urban transport schemes, which require dense access systems during civil works and fit-out stages. India's construction sector is projected to record 8-10% revenue growth in fiscal year 2027, following 6-8% growth in fiscal year 2026, suggesting continued order flow for access equipment suppliers.

Industrial Maintenance and Shutdown Projects Increase Scaffolding Usage

Industrial shutdown work provides the India scaffolding market with a demand stream that is not dependent on new building starts. Refineries and petrochemical plants must complete periodic maintenance turnarounds, and those events require safe access to elevated pipework, vessels, and internal process units. Haldia Petrochemicals completed a 45-day turnaround in 2025 at its West Bengal facility, Indian Oil's Gujarat refinery carried out a phased shutdown through mid-2025, and Reliance shut a crude unit for 21 days at Jamnagar in 2025. Bharat Petroleum is also scheduled to shut a crude unit at its Mumbai refinery for 3-4 weeks in November 2026. Because these events are tied to safety and operating rules, they help organized contractors keep utilization and pricing firmer than the broader construction cycle alone would suggest.

Unorganized Market Competition Creates Pricing Pressure

A large informal supply base remains one of the main brakes on the Indian scaffolding market. Small local operators often use non-certified material, skip testing records, and compete on low prices that organized suppliers cannot easily match. This pressure is strongest in residential and mid-scale commercial work, where site managers often choose nearby vendors who can deliver quickly and offer flexible credit terms. That makes price competition harder to solve with scale alone, because local relationships still matter in many cities. The result is a slower shift toward higher quality fleets and a lower average selling price in parts of the India scaffolding market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Safety Compliance Drives Adoption of Standardized Scaffolding Systems

- Shift Toward Modular and Reusable Systems Enhances Market Growth

- Safety Compliance Gaps Restrict Adoption of Quality Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Supported scaffolds accounted for 63.0% of the market in 2025, making it the largest type in the India scaffolding market. Its lead comes from broad use across residential towers, office projects, industrial structures, and bridge substructure work. It remains the default choice on many sites because it is familiar, flexible, and easier to source at scale across cities. Suspended scaffolds are the fastest-growing type and are forecast to expand at a 9.1% CAGR through 2031, as facade work, bridge rehabilitation, and tall industrial assets require access where ground support is less practical.

Supported systems should keep their lead because most construction volume in India still comes from applications where ground-based access works well. Housing, standard commercial buildings, and many industrial additions continue to favor simple and proven setups over highly specialized equipment. The faster growth in suspended systems does not change that base, but it does show that the India scaffolding market is becoming more balanced across new construction and maintenance work. Older high-rise stock is also entering repair cycles, increasing the need for facade access over time. Storage terminals and tank farms add another recurring use case, since inspection and repainting work often depend on suspended access methods during scheduled maintenance.

Cuplock accounted for 38.0% of the value in 2025, maintaining its leading position in the India scaffolding market. Its strength comes from wide contractor familiarity, broad availability, and competitive pricing on standard building work. Cuplock is still well-suited to residential blocks, commercial shells, and many repetitive layouts where speed and cost matter more than custom engineering. Modular / ringlock is the fastest-growing category, projected to grow at a 10.4% CAGR through 2031, as complex infrastructure projects require greater flexibility and clearer load documentation.

The shift is most visible on metro rail corridors, elevated expressways, and bridge contracts where geometry changes from span to span. On those jobs, rosette-based systems help crews adapt faster without relying on improvised site modifications. The India scaffolding industry is therefore moving toward a two-speed system mix, with cuplock staying strong in mainstream work and modular systems taking a growing share of high-value contracts. Regulatory pressure also supports this shift, because formal infrastructure procurement increasingly prefers systems with tested performance and documented load ratings.

Complete Report Scope:

- By Type

- Supported Scaffold

- Suspended Scaffold

- Mobile Scaffold

- By System

- Tube & Coupler

- Cuplock

- Modular / Ringlock

- Frame / H-Frame

- By Business Model

- Sales

- Rental

- By Material Type

- Timber / Plywood

- Steel

- Aluminum

- Plastic / Fibreglass

- Others

- By Sector

- Residential

- Commercial

- Industrial & Logistics

- Infrastructure

- By City

- Mumbai Metropolitan Region

- Delhi NCR

- Pune

- Bengaluru

- Hyderabad

- Rest of India

List of Companies Covered in this Report:

- PERI India Pvt. Ltd.

- Doka India Pvt. Ltd.

- Layher Scaffolding Systems Pvt Ltd

- ULMA Formwork Systems India Pvt. Ltd

- RMD Kwikform India

- Technocraft Industries, India Ltd.

- JRS Scaffoldings

- Finomax Scaffolding (I) Pvt. Ltd.

- Expee Engineering Private Limited

- Iron Ridge Scaffolding and Engineering (I) Pvt. Ltd.

- AMCO Exports

- Wheels Scaffolding (India) Ltd.

- Winntus Formwork Private Limited

- Ananta Formwork Private Limited

- Nexrise India Infra Pvt. Ltd.

- Hindustan Scaffolding and Formwork Pvt. Ltd.

- Safeway Scaffolding and Formwork Pvt. Ltd.

- BSL Scaffolding Ltd

- Bharat Scaffolding Co.

- Shreeji Scaffolding Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Commercial and Infrastructure Construction Boosts Scaffolding Demand

- 4.2.2 Industrial Maintenance and Shutdown Projects Increase Scaffolding Usage

- 4.2.3 Stricter Safety Compliance Drives Adoption of Standardized Scaffolding Systems

- 4.2.4 Shift Toward Modular and Reusable Systems Enhances Market Growth

- 4.2.5 Rental Model Expansion Improves Access to Scaffolding Equipment

- 4.2.6 Growing Urban Development Expands Scaffolding Requirements Across Cities

- 4.3 Market Restraints

- 4.3.1 Unorganized Market Competition Creates Pricing Pressure

- 4.3.2 Safety Compliance Gaps Restrict Adoption of Quality Systems

- 4.3.3 Fluctuating Raw Material Prices Increase Equipment Costs

- 4.3.4 High Initial Cost of Advanced Scaffolding Systems Limits Uptake

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Cost Structure Analysis

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Geopolitics

- 4.9.1 Raw Material Price Volatility

- 4.9.2 Supply Chain Disruptions and Longer Lead Times

- 4.9.3 Rising Energy and Logistics Costs

- 4.9.4 Infrastructure, Energy Security, and Defense-Led Demand

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Supported Scaffold

- 5.1.2 Suspended Scaffold

- 5.1.3 Mobile Scaffold

- 5.2 By System

- 5.2.1 Tube & Coupler

- 5.2.2 Cuplock

- 5.2.3 Modular / Ringlock

- 5.2.4 Frame / H-Frame

- 5.3 By Business Model

- 5.3.1 Sales

- 5.3.2 Rental

- 5.4 By Material Type

- 5.4.1 Timber / Plywood

- 5.4.2 Steel

- 5.4.3 Aluminum

- 5.4.4 Plastic / Fibreglass

- 5.4.5 Others

- 5.5 By Sector

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial & Logistics

- 5.5.4 Infrastructure

- 5.6 By City

- 5.6.1 Mumbai Metropolitan Region

- 5.6.2 Delhi NCR

- 5.6.3 Pune

- 5.6.4 Bengaluru

- 5.6.5 Hyderabad

- 5.6.6 Rest of India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PERI India Pvt. Ltd.

- 6.4.2 Doka India Pvt. Ltd.

- 6.4.3 Layher Scaffolding Systems Pvt Ltd

- 6.4.4 ULMA Formwork Systems India Pvt. Ltd

- 6.4.5 RMD Kwikform India

- 6.4.6 Technocraft Industries, India Ltd.

- 6.4.7 JRS Scaffoldings

- 6.4.8 Finomax Scaffolding (I) Pvt. Ltd.

- 6.4.9 Expee Engineering Private Limited

- 6.4.10 Iron Ridge Scaffolding and Engineering (I) Pvt. Ltd.

- 6.4.11 AMCO Exports

- 6.4.12 Wheels Scaffolding (India) Ltd.

- 6.4.13 Winntus Formwork Private Limited

- 6.4.14 Ananta Formwork Private Limited

- 6.4.15 Nexrise India Infra Pvt. Ltd.

- 6.4.16 Hindustan Scaffolding and Formwork Pvt. Ltd.

- 6.4.17 Safeway Scaffolding and Formwork Pvt. Ltd.

- 6.4.18 BSL Scaffolding Ltd

- 6.4.19 Bharat Scaffolding Co.

- 6.4.20 Shreeji Scaffolding Pvt. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment