PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073226

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073226

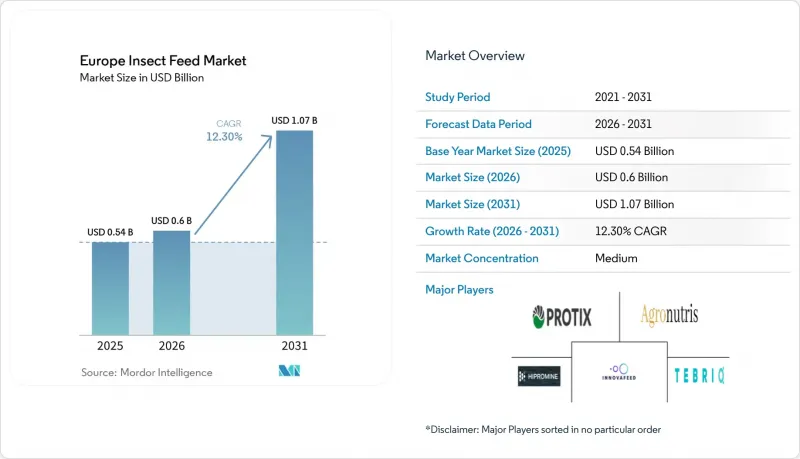

Europe Insect Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe insect feed market was valued at USD 0.54 billion in 2025 and is projected to grow from USD 0.60 billion in 2026 to USD 1.07 billion by 2031, registering a CAGR of 12.3% during the forecast period (2026-2031).

This report is Segmented by Insect Species (Black Soldier Fly, Mealworm, Housefly, and Others), by Product Form (Protein Meal, Whole Dried Larvae, Insect Oil, and Frass Fertilizer), by Animal Type (Aquaculture, Poultry, Swine, and More), by End User (Commercial Feed Mills and More), and by Geography (Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Insect Feed Market Trends and Insights

EU Feed Authorizations Expand Insect Protein Addressable Demand

The Europe insect feed market has benefited directly from the stepwise expansion of EU feed rules over the past several years. Regulation (EU) 2017/893 first allowed insect-processed animal proteins in aquaculture feed, and the 2021 amendment extended that permission to swine and poultry, which opened much larger livestock categories for commercial use. A 2024 regulatory clarification also confirmed that live insects can be used as feed materials for swine, poultry, and aquaculture, which gives smaller operators a lower processing route than full PAP production. Each authorization has widened the customer base for producers across aquaculture, poultry, swine, and pet food, and this has made industrial scaling more commercially rational. The Europe insect feed market is also supported by the formal adoption of the International Platform of Insects for Food and Feed (IPIFF) good hygiene guidance in 2025, which improves traceability and reduces procurement concerns for feed mills entering the category for the first time. Growth is still limited by the continued exclusion of ruminants, but monogastric and aquaculture categories already represent the clearest short-term route for scale in the Europe insect feed market.

Aquaculture Feed Seeks Fishmeal and Fish Oil Replacement

Aquaculture remains one of the strongest demand anchors for the Europe insect feed market because fishmeal supply is constrained while aquaculture feed demand keeps increasing. EU aquatic food self-sufficiency fell to 38.1% in 2023, and the bloc imports a large share of the feed proteins it consumes, which raises both supply security and sustainability concerns. Research in species such as rainbow trout, Atlantic salmon, European perch, and totoaba shows that insect meals can replace a meaningful share of fishmeal without damaging growth, digestibility, or product quality when inclusion is managed correctly. Norway is especially important because salmon farming has high feed-related emissions, which makes insect ingredients relevant not only as protein substitutes but also as carbon reduction tools inside existing feed systems. The Europe insect feed market is therefore drawing support from both performance validation and policy pressure in aquaculture. That combination becomes more important as industry groups push for formal inclusion targets in aquafeed over the next several years.

Demand Remains Concentrated in Premium Applications

Demand concentration is one of the major restraints shaping the Europe insect feed market. In practice, the strongest adoption still sits in aquaculture starter feeds, salmonid diets, premium pet food, and other higher-value channels rather than in broad poultry and swine formulations. Poultry and swine together make up most of the European compound feed tonnage, but those applications require much tighter price parity with soybean meal than the category can yet provide. Socio-economic research also suggests that mainstream economics remain tight even under significant scale increases, which means broad-based penetration is more likely to be gradual than sudden. This concentration matters because premium channels can be subject to reformulation cycles and brand positioning shifts. The Europe insect feed market, therefore, needs continued progress in cost reduction and industrial reliability before it can move from selective adoption into true mass-market inclusion.

Other drivers and restraints analyzed in the detailed report include:

- Pet Food Premiumization Lifts Demand for Novel Insect Ingredients

- Functional Lipids, Chitin, and Bioactive Fractions Broaden Value Capture

- EU-Approved Feedstock List Constrains Substrate Flexibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Black soldier fly accounted for 49.5% of the Europe insect feed market in 2025, driven by its scalability, nutritional benefits, and processing flexibility. These larvae are highly preferred due to their efficient feed conversion, production of usable protein and oil fractions, and compatibility with industrial side-stream sourcing models. Consequently, the Europe insect feed market has predominantly adopted black soldier fly larvae as the primary platform for large-scale commercialization. Research has further validated this trend, demonstrating that black soldier fly meal can effectively replace a significant portion of fishmeal in carnivorous species without negatively impacting growth performance.

Black soldier fly also aligns well with current European plant economics, as producers can extract meal, oil, and fertilizer from a single biomass stream. This enhances revenue potential and allows producers to adjust their product mix across feed and related markets. Meanwhile, mealworms are rapidly gaining traction, with a projected CAGR of 13.6% through 2031. Mealworms are particularly appealing in premium pet food and other specialized applications where digestibility and hypoallergenic properties are prioritized over large-scale production. The EU's authorization of UV-treated mealworm powder in January 2025 has further expanded processing opportunities and facilitated facility-sharing for mealworm production. Other insect types, such as houseflies and crickets, currently occupy smaller niches within the Europe insect feed market, catering to more specific feed applications rather than large-scale industrial use.

Insect meal accounted for 58.0% of the Europe insect feed market in 2025, making it the core commercial product at this stage. Its prominence is attributed to its direct applicability in aquafeed and compound feed formulations, where protein concentration and digestibility are key purchasing factors. The market continues to rely on insect meal, as it is the most straightforward substitute for existing protein sources in established feed formulations. Technical data further supports its role, with insect meals demonstrating strong digestibility and amino acid profiles, making them increasingly suitable for specialized formulations. As a result, insect meal remains the most widely utilized product, even as the overall product portfolio diversifies.

Insect oil is the fastest-growing product form in the market, with a projected CAGR of 14.4% from 2026 to 2031. This growth is driven by rising demand for black soldier fly oil in pet food and monogastric feed, particularly for its lauric acid content and antimicrobial properties. Whole dried insects, while a smaller segment, are primarily used for treats, exotic animals, and niche specialty applications. Other product forms, such as puree and hydrolysates, are also gaining traction, especially in wet pet food and aquaculture starter feed applications, where functional formats are increasingly valued. The Europe insect feed industry is shifting toward higher-margin products like oils and specialty formats to mitigate the cost constraints associated with commodity protein sales. Companies such as HiProMine and Nasekomo illustrate that product strategy is becoming as critical as scale strategy in the Europe insect feed market.

Complete Report Scope:

- By Insect Species

- Black Soldier Fly

- Mealworm

- Housefly

- Others

- By Product Form

- Protein Meal

- Whole Dried Larvae

- Insect Oil

- Frass Fertilizer

- By Animal Type

- Aquaculture

- Poultry

- Swine

- Ruminants

- Pets

- By End User

- Commercial Feed Mills

- Integrated Livestock Producers

- Smallholder/On-farm Systems

- By Geography

- Germany

- France

- United Kingdom

- Netherlands

- Spain

- Italy

- Poland

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- InnovaFeed SAS

- Protix B.V.

- nextProtein SAS

- HiProMine S.A.

- Tebrio (Tebrio Group S.L.)

- Agronutris

- Volare

- Nasekomo

- BioflyTech

- Better Origin (Entomics Biosystems Limited)

- Hermetia Baruth

- Illucens

- Insectius

- FarmInsect

- EntoGreen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU feed authorizations expand insect protein addressable demand

- 4.2.2 Aquaculture feed seeks fishmeal and fish oil replacement

- 4.2.3 Circular feed sourcing and Scope 3 reduction targets support adoption

- 4.2.4 Pet food premiumization lifts demand for novel insect ingredients

- 4.2.5 Co-location with side streams and waste heat improves plant economics

- 4.2.6 Functional lipids, chitin, and bioactive fractions broaden value capture

- 4.3 Market Restraints

- 4.3.1 Production costs remain above incumbent protein alternatives

- 4.3.2 EU-approved feedstock list constrains substrate flexibility

- 4.3.3 Risk repricing after scale-up failures tightens financing access

- 4.3.4 Demand remains concentrated in premium applications

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Insect Species

- 5.1.1 Black Soldier Fly

- 5.1.2 Mealworm

- 5.1.3 Housefly

- 5.1.4 Others

- 5.2 By Product Form

- 5.2.1 Protein Meal

- 5.2.2 Whole Dried Larvae

- 5.2.3 Insect Oil

- 5.2.4 Frass Fertilizer

- 5.3 By Animal Type

- 5.3.1 Aquaculture

- 5.3.2 Poultry

- 5.3.3 Swine

- 5.3.4 Ruminants

- 5.3.5 Pets

- 5.4 By End User

- 5.4.1 Commercial Feed Mills

- 5.4.2 Integrated Livestock Producers

- 5.4.3 Smallholder/On-farm Systems

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 United Kingdom

- 5.5.4 Netherlands

- 5.5.5 Spain

- 5.5.6 Italy

- 5.5.7 Poland

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 InnovaFeed SAS

- 6.4.2 Protix B.V.

- 6.4.3 nextProtein SAS

- 6.4.4 HiProMine S.A.

- 6.4.5 Tebrio (Tebrio Group S.L.)

- 6.4.6 Agronutris

- 6.4.7 Volare

- 6.4.8 Nasekomo

- 6.4.9 BioflyTech

- 6.4.10 Better Origin (Entomics Biosystems Limited)

- 6.4.11 Hermetia Baruth

- 6.4.12 Illucens

- 6.4.13 Insectius

- 6.4.14 FarmInsect

- 6.4.15 EntoGreen

7 Market Opportunities and Future Outlook