PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073233

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073233

GCC Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

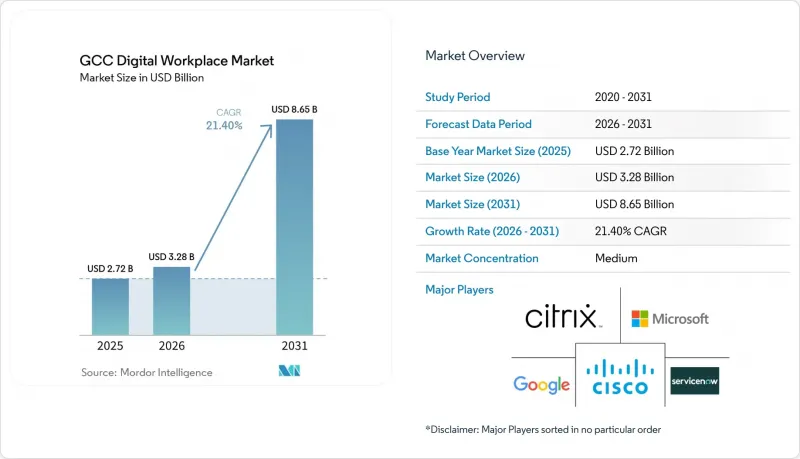

According to Mordor Intelligence, the GCC digital workplace market size is expected to increase from USD 2.72 billion in 2025 to USD 3.28 billion in 2026 and reach USD 8.65 billion by 2031, growing at a CAGR of 21.40% over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Government and Public Sector, Education, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

GCC Digital Workplace Market Trends and Insights

Accelerated Shift To Hybrid Work Operating Models

The GCC digital workplace market is being shaped by hybrid work becoming a standard operating model for knowledge-heavy roles across the region. This shift is expanding spending beyond collaboration software into identity management, endpoint security, device control, and remote access design. The GCC digital workplace market is also becoming more complex, as many enterprises manage teams across Saudi Arabia, the United Arab Emirates, and offshore delivery locations simultaneously. That operating model forces buyers to prioritize interoperability across different regulatory and administrative environments. Procurement cycles are therefore becoming broader because platform choices now affect governance, compliance, and service delivery together. This has kept recurring demand strong for integrators and managed service providers long after the first deployment phase is completed.

Greater Adoption of AI-Assisted Workflow Automation and Knowledge Retrieval

The GCC digital workplace market is seeing AI move quickly from experimentation to embedded, daily use within enterprise workflow tools. AI copilots, knowledge retrieval layers, and task automation tools are now being folded into broader workplace platforms rather than purchased as separate utilities. IBM stated that GCC enterprises are redesigning their operating models around AI, indicating that platform buying is shifting from feature-led decisions to integrated transformation programs. The GCC digital workplace market is also being pushed by the unusually large scale of deployments in government-linked organizations and sovereign wealth-backed enterprises. Those rollouts are often designed for very large employee populations, which speeds vendor expansion and raises the importance of governance, orchestration, and Arabic-language usability. As a result, the GCC digital workplace market is rewarding vendors that can integrate AI tools with communications, endpoint management, and employee experience functions within a single operating environment.

Integration of Complexity Across Legacy Identity, Device, And Collaboration Stacks

The GCC digital workplace market still faces a major friction point: legacy IT environments built over years of disconnected procurement. Many organizations operate several identity directories, overlapping endpoint tools, and parallel collaboration suites at the same time. That structure makes new deployments slower, because every digital workplace layer has to connect with existing access controls, devices, and governance rules. The GCC digital workplace market is especially exposed in public sector, banking, energy, and other sectors where older systems remain deeply embedded in daily operations. Audit and cybersecurity requirements often reveal these architecture gaps, but fixing them can require long transition periods and careful change control. Until identity and middleware environments become more unified, this issue will continue to moderate the pace of large-scale workplace transformation.

Other drivers and restraints analyzed in the detailed report include:

- Public Sector Digitization Programs and Workforce Modernization

- Cloud-First Workplace Modernization in Large GCC Enterprises

- Data Residency and Sovereignty Constraints on Cloud Workplace Rollouts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 71.42% of the GCC digital workplace market share in 2025, confirming that software platforms remained the main center of spending across the GCC digital workplace market. Unified communication and collaboration tools, unified endpoint management, and employee experience platforms formed the main demand base within this segment. The GCC digital workplace market is now pulling workflow automation and knowledge management into the same buying cycle as communications and device management. IBM's view of an AI-centered operating model redesign reflects this platform-consolidation pattern, in which enterprises are assessing workplace tools as part of a broader transformation. This has raised the strategic value of vendors that can connect productivity, governance, and workflow design within one operating environment.

The services segment held a smaller share, but its commercial importance continued to rise as the GCC digital workplace market became harder to deploy and govern at scale. Implementation support, architecture design, managed operations, and compliance documentation all gained weight as organizations worked through legacy integration challenges. The GCC digital workplace market also continued to create service demand through identity harmonization, rollout support, and post-deployment optimization. Virtual desktop infrastructure and cloud PC adoption added another service layer because many enterprises were shifting from device-led capital spending to per-seat operational models. Even so, solutions remained the primary demand anchor, because most vendor differentiation still centered on platform breadth, AI readiness, and integration depth.

Cloud accounted for 68.76% share of the GCC digital workplace market size in 2025, making it the dominant deployment mode across the GCC digital workplace market. This lead reflects enterprises' growing comfort with subscription-based delivery, reduced provisioning friction, and faster access to new AI-enabled workplace features. Microsoft's support for in-country data processing for Microsoft 365 Copilot in the United Arab Emirates and its Saudi Arabia datacenter rollout, scheduled for Q4 2026, directly addressed the localization concerns that had slowed some regulated buyers. The GCC digital workplace market, therefore, saw the old tradeoff between agility and compliance begin to weaken. On-premises deployment remains relevant in defense, intelligence, and critical infrastructure settings, where local control remains essential.

Hybrid deployment drew strong attention because the GCC digital workplace market still included many large enterprises that needed dual-mode operating models. These buyers often kept sensitive workloads in tightly controlled environments while moving broader collaboration and productivity layers into the cloud. That pattern created recurring work for integration partners because architecture, policy, and reporting standards had to function across both modes. The GCC digital workplace market also favored hybrid models in organizations where modernization was being phased by business unit, country, or data sensitivity tier. Over time, sovereign and in-country infrastructure is likely to shift more of these deployments toward cloud, but the hybrid path remains commercially important in the near term.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of GCC

List of Companies Covered in this Report:

- Microsoft Corporation

- Cisco Systems, Inc.

- ServiceNow, Inc.

- Citrix Systems, Inc.

- Google LLC

- Zoom Communications, Inc.

- IBM Corporation

- Dell Technologies Inc.

- Lenovo Group Limited

- SAP SE

- Oracle Corporation

- HCL Technologies Limited

- Accenture plc

- LumApps SAS

- Ivanti, Inc.

- TeamViewer SE

- Zoho Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Shift to Hybrid Work Operating Models

- 4.2.2 Rising Demand for Unified Employee Experience Platforms

- 4.2.3 Increased Need for Zero-Touch Endpoint Provisioning Across Distributed Workforces

- 4.2.4 Greater Adoption of AI-Assisted Workflow Automation and Knowledge Retrieval

- 4.2.5 Cloud-First Workplace Modernization in Large GCC Enterprises

- 4.2.6 Public Sector Digitization Programs and Workforce Modernization

- 4.3 Market Restraints

- 4.3.1 Integration Complexity Across Legacy Identity, Device, and Collaboration Stacks

- 4.3.2 Data Residency and Sovereignty Constraints on Cloud Workplace Rollouts

- 4.3.3 End User Change Resistance and Low Digital Process Maturity in Some Organizations

- 4.3.4 Talent Shortage in Digital Workplace Architecture and Managed Services

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Oman

- 5.5.6 Bahrain

- 5.5.7 Rest of GCC

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 ServiceNow, Inc.

- 6.4.4 Citrix Systems, Inc.

- 6.4.5 Google LLC

- 6.4.6 Zoom Communications, Inc.

- 6.4.7 IBM Corporation

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Lenovo Group Limited

- 6.4.10 SAP SE

- 6.4.11 Oracle Corporation

- 6.4.12 HCL Technologies Limited

- 6.4.13 Accenture plc

- 6.4.14 LumApps SAS

- 6.4.15 Ivanti, Inc.

- 6.4.16 TeamViewer SE

- 6.4.17 Zoho Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment