PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073260

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073260

Thailand Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

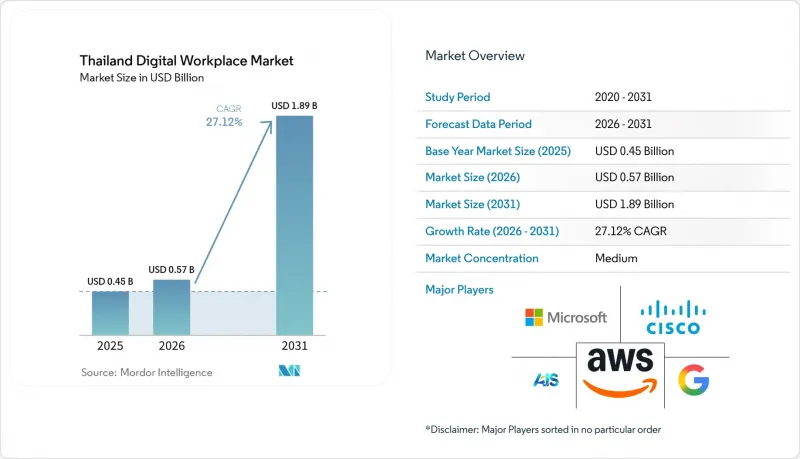

According to Mordor Intelligence, the thailand digital workplace market size was valued at USD 0.45 billion in 2025 and estimated to grow from USD 0.57 billion in 2026 to reach USD 1.89 billion by 2031, at a CAGR of 27.12% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, Energy and Utilities, and More). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Digital Workplace Market Trends and Insights

Rising Hybrid Work Standardization In Thai Enterprises

Hybrid work in Thailand has moved beyond a temporary arrangement and has become part of formal workforce policy in many organizations, which is creating a clear buying trigger for the Thailand digital workplace market. A 2025 survey of 702 Thai employers found that part-time permanent roles in large organizations rose from 20% to 42%, while contract part-time roles increased from 19% to 28%, which shows that flexible work structures are becoming embedded in the labor market. This shift means employers can no longer depend on informal tool use and now need unified platforms that support communication, device control, and workflow continuity across office and remote settings. Microsoft's Work Trend Index 2025 reported that 68% of Thai organizations had already started implementing AI agents to automate business processes, which places the workplace platform closer to an operating layer than a basic communication layer. Cathcart Technology also reported that 31% of Thai technology professionals preferred a 2-day onsite and 3-day remote pattern in 2025, which reinforces the need for stable digital workspace infrastructure across locations.

Cloud-First Workplace Refresh Cycles In Bangkok-Focused Enterprises

Bangkok's enterprise base is moving through a workplace refresh cycle that is closely tied to cloud migration, and this is strengthening demand in the Thailand digital workplace market. The launch of in-country cloud capacity by Amazon Web Services and Google Cloud, together with Microsoft's announced infrastructure investment, has reduced earlier concerns around latency and local data handling for enterprise workloads. Krungsri accelerated its cloud migration timeline by more than 50% through generative AI work with AWS, which shows that workplace modernization is now happening alongside core infrastructure change rather than after it. Google Cloud stated that Thai organizations migrating to its platform can cut unplanned downtime by over 50% and optimize technology spending by over 20% on average, which gives finance teams a direct case for broader platform renewal. As a result, many companies that have completed an initial cloud move are now in position to replace older collaboration, endpoint, and virtual desktop tools with more integrated platforms.

PDPA-Driven Security Review Delays

Thailand's PDPA continues to slow platform procurement when workplace tools handle employee monitoring data, attendance records, communication logs, or analytics outputs. Employers need to map each type of employee data to a lawful basis for collection and use, which adds legal and operational review work before a full deployment can proceed. Notifications on ROPA exemptions issued in January 2025 gave smaller firms some relief, but they did not remove the broader need for cross-functional compliance checks when organizations assess AI-enabled workplace tools. The PDPA Master Plan 2024-2027 signals that Thailand is still tightening its data protection framework rather than moving into a lighter enforcement phase. This keeps deployment speed uneven across the Thailand digital workplace market and can push buyers toward smaller point solutions instead of broad suite rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Public Sector Digitization And Thailand 4.0 Programs

- AI-Ready Collaboration And Employee Experience Demand

- Fragmented Legacy Application Estates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 72.43% of the Thailand digital workplace market in 2025, which shows that enterprises are putting more of their budgets into software-defined workplace architecture than into stand-alone service delivery. This lead reflects the shift toward integrated communication, endpoint, workflow, and employee experience platforms that can be deployed across hybrid work settings. Unified communication and collaboration tools are moving fastest within the solutions-based because companies are trying to consolidate separate voice, messaging, and meeting products into fewer environments. Local cloud capacity has supported this change because it removes a major reason for keeping fragmented tool stacks in place. In financial services, the Kasikorn Business-Technology Group's deployment of high-availability data center networking with Huawei shows how institutions are building the underlying backbone needed for cloud-delivered desktop and workforce continuity models.

The services segment remains smaller, but its role is growing as the Thailand digital workplace industry moves from initial adoption into migration, change management, compliance readiness, and optimization work. Professional services demand is rising because buyers often need help linking workplace platforms to legacy applications, security frameworks, and business process rules. Large integrators such as Accenture, IBM, Wipro, TCS, and Infosys are positioned around this layer because the work now reaches beyond tool deployment and into operating model redesign. Workflow automation and knowledge management tools are also moving up the priority list because organizations that have already deployed core collaboration platforms are now trying to improve process flow and information access across teams. At the same time, the Thailand digital workplace industry still leaves room for focused solutions that address specific workflow gaps in manufacturing, HR, or service operations without requiring a full suite replacement.

Cloud was the leading deployment model in the Thailand digital workplace market in 2025 with a 69.27% share, and the cloud in the Thailand digital workplace market size is projected to grow at a 21.99% CAGR through 2031. This position has become stronger because local hyperscale infrastructure now gives Thai enterprises access to global-grade cloud performance with local hosting options. Google Cloud's Bangkok region includes three availability zones and integration with the TalayLink subsea cable, which supports low-latency collaboration and virtual desktop workloads across Southeast Asia. Amazon Web Services also launched the AWS Asia Pacific (Thailand) Region as part of a long-term infrastructure commitment, which gives enterprises another local path for hosting workplace applications and data. These moves support a broader replacement cycle in which older hybrid or on-premises collaboration tools are being reconsidered as companies modernize their infrastructure base.

On-premises deployment still matters in regulated settings where organizations want stricter control over selected HR, communications, or monitoring data before they move further into cloud-based workplace operations. Hybrid architecture remains relevant because it lets companies keep sensitive control points on internal systems while running analytics, collaboration, and workflow tools in the cloud. This pattern is visible in manufacturing and utilities where shop-floor operations and operational continuity needs do not always line up with a full cloud-only move. Domestic cloud options are also shaping some buyer decisions because locally governed infrastructure can reduce hesitation in public sector and state-adjacent accounts. As a result, cloud leads clearly, but deployment choice in the Thailand digital workplace market is still influenced by security posture, operating complexity, and the pace of internal change.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- Deployment Mode

- Cloud

- On-Premises

- Hybrid

- Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

List of Companies Covered in this Report:

- Microsoft Corporation

- Google LLC

- Cisco Systems, Inc.

- Amazon Web Services, Inc.

- Cloud HM Company Limited

- AIS Business

- True Corporation Public Company Limited

- Broadcom Inc.

- Citrix Systems, Inc.

- Nutanix, Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Zoom Video Communications, Inc.

- RingCentral, Inc.

- 8x8, Inc.

- NEC Corporation

- Fujitsu Limited

- Accenture PLC

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- DXC Technology Company

- IBM Corporation

- SAP SE

- Oracle Corporation

- ServiceNow, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hybrid Work Standardization in Thai Enterprises

- 4.2.2 Cloud-First Workplace Refresh Cycles in Bangkok-Focused Enterprises

- 4.2.3 Public Sector Digitization and Thailand 4.0 Programs

- 4.2.4 AI-Ready Collaboration and Employee Experience Demand

- 4.2.5 Cross-Platform Migration Pressure From Legacy Messaging and Endpoint Tools

- 4.2.6 Sector-Specific Compliance and Auditability Requirements

- 4.3 Market Restraints

- 4.3.1 PDPA-Driven Security Review Delays

- 4.3.2 Fragmented Legacy Application Estates

- 4.3.3 SME Budget Sensitivity for Multi-Tool Suites

- 4.3.4 Shortage of Workplace Modernization Skills and Change Managers

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Amazon Web Services, Inc.

- 6.4.5 Cloud HM Company Limited

- 6.4.6 AIS Business

- 6.4.7 True Corporation Public Company Limited

- 6.4.8 Broadcom Inc.

- 6.4.9 Citrix Systems, Inc.

- 6.4.10 Nutanix, Inc.

- 6.4.11 Dell Technologies Inc.

- 6.4.12 Hewlett Packard Enterprise Company

- 6.4.13 Zoom Video Communications, Inc.

- 6.4.14 RingCentral, Inc.

- 6.4.15 8x8, Inc.

- 6.4.16 NEC Corporation

- 6.4.17 Fujitsu Limited

- 6.4.18 Accenture PLC

- 6.4.19 Tata Consultancy Services Limited

- 6.4.20 Infosys Limited

- 6.4.21 Wipro Limited

- 6.4.22 DXC Technology Company

- 6.4.23 IBM Corporation

- 6.4.24 SAP SE

- 6.4.25 Oracle Corporation

- 6.4.26 ServiceNow, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment