PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073269

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073269

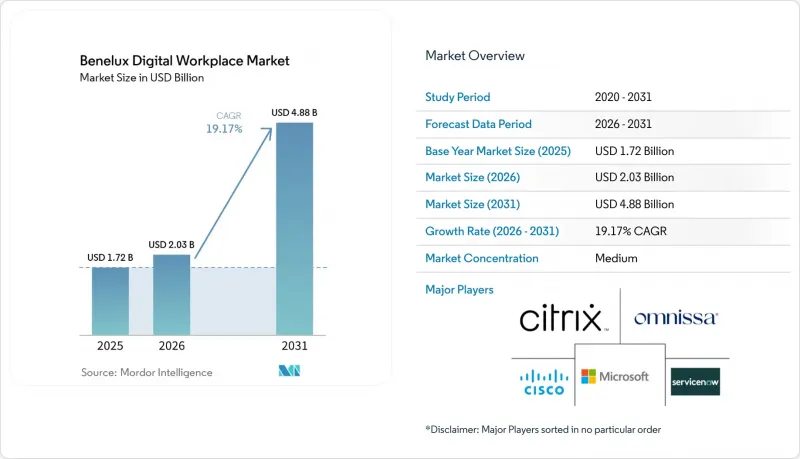

Benelux Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the benelux digital workplace market size is expected to grow from USD 1.72 billion in 2025 to USD 2.03 billion in 2026 and is forecast to reach USD 4.88 billion by 2031 at 19.17% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, Healthcare, Manufacturing, Government and Public Sector, Education, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Benelux Digital Workplace Market Trends and Insights

Hybrid Work Normalization Across Benelux Enterprises

Hybrid work has moved from an emergency response to a durable operating model, and that shift keeps the Benelux digital workplace market on a firm growth path. Belgium reported that 34.8% of employees worked from home in 2025, far above the 18.9% recorded in 2019. In the Netherlands, 80% of businesses with 10 or more employees offered telework in 2025, indicating that remote and flexible work practices are already embedded in day-to-day business activity. This kind of normalization raises the need for tools that can manage devices, identities, collaboration, and secure access across distributed teams without raising complexity for employers. As a result, workplace spending is less tied to one-off projects and more tied to recurring operating needs across the Benelux digital workplace market.

AI-Augmented Workflow Automation In Knowledge-Heavy Workplaces

AI-led automation is gaining traction because many employers in the region rely on knowledge-heavy work that benefits from structured, repeatable digital workflows. The Benelux digital workplace market is seeing this most clearly in Luxembourg, where the CSSF and Banque centrale du Luxembourg reported that local entities expected AI investment growth in 2025 and 2026 to outpace group-level growth as firms applied broader AI strategies within their own operations. The early focus on back-office and controlled workflow use cases aligns well with digital workplace platforms that combine collaboration, knowledge access, and task routing in a single environment. The EU AI Act is also shaping demand because deployers of high-risk AI systems face governance obligations that increase the value of platforms with logging, oversight, and clear controls. ServiceNow strengthened that direction in 2026 through launches such as Autonomous Workforce and Otto, which showed how vendors are packaging AI automation as part of broader workplace platforms rather than as isolated tools.

Fragmented Legacy Application Estates

Legacy application sprawl continues to slow modernization, as many organizations still run mixed environments that were not designed to function as a single system. This remains a clear friction point for the Benelux digital workplace market because workplace upgrades often depend on identity links, endpoint policies, and secure integrations across older and newer software layers. The challenge is sharper in regulated and operational settings, where firms cannot retire important systems quickly even when those systems create duplication and manual work. As cloud, on-premises, and hybrid layers remain active simultaneously, integration costs rise and project timelines stretch. The result is that enterprises often spend more time rationalizing old estates than scaling new workplace capabilities across the organization.

Other drivers and restraints analyzed in the detailed report include:

- Microsoft 365 And Teams Ecosystem Lock-In

- Data Sovereignty and Compliance-Driven Cloud Modernization

- Skills Shortage in Workplace Transformation and VDI Architecture

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 68.12% of the Benelux digital workplace market share in 2025, which showed that software-led spending was already ahead of pure services demand. Unified communication and collaboration remained the largest sub-segment within solutions because enterprises needed a common environment for meetings, messaging, files, and task coordination. Unified endpoint management and enterprise mobility management also gained ground as employers tried to manage Windows, macOS, and mobile estates through fewer administrative layers. Ivanti's 2026 launch of Neurons for MDM Sovereign Edition EU reflected this shift by linking endpoint control with sovereignty and compliance needs in regulated environments.

Virtual desktop infrastructure and cloud PC tools also remained relevant as employers sought secure desktop delivery with reduced endpoint data exposure. Employee experience platforms and intranet tools gained attention because organizations increasingly judged value by adoption and day-to-day usability rather than solely by deployment status. Workflow automation and knowledge management tools moved closer to the center of the Benelux digital workplace market as AI features made it easier to route tasks, summarize activity, and surface information inside one workspace. Services still mattered for integration, support, and change programs, but the revenue mix showed that the core of demand sat with the platforms themselves.

Cloud held a 65.37% share of the Benelux digital workplace market in 2025 and is projected to expand at a 20.73% CAGR through 2031, making it both the largest and the fastest-growing deployment model. This growth reflected a more mature wave of adoption, in which enterprises sought compliant, controllable cloud models rather than just cheaper infrastructure. Microsoft's April 2026 launch in Belgium strengthened that case by giving regional customers a clearer in-region option under the EU Data Boundary framework. Ivanti's 2026 sovereign endpoint management release showed the same demand pattern on both the device and administration sides.

On-premises deployments still mattered in defense-adjacent, public sector, and tightly regulated financial settings where full cloud migration was not yet practical. Hybrid models, therefore, maintained an important role because they allowed employers to separate sensitive workloads from less critical ones without abandoning modernization. This balance is likely to remain important in the Benelux digital workplace market as buyers continue to choose cloud services, while exercising stricter control over data location and governance. In practice, cloud growth in the region now means sovereign-by-design and policy-aware deployment, not a simple shift to fully public cloud environments.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Belgium

- Netherlands

- Luxembourg

List of Companies Covered in this Report:

- Microsoft Corporation

- Cisco Systems, Inc.

- ServiceNow, Inc.

- Citrix Systems, Inc.

- Omnissa, LLC

- Google LLC

- Zoom Communications, Inc.

- Atlassian Corporation

- IBM Corporation

- Salesforce, Inc.

- Unily Group Limited

- Workvivo Limited

- Ivanti, Inc.

- Accenture plc

- Capgemini SE

- Atos SE

- Cognizant Technology Solutions Corporation

- Wipro Limited

- Tata Consultancy Services Limited

- Infosys Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid Work Normalization Across Benelux Enterprises

- 4.2.2 Microsoft 365 and Teams Ecosystem Lock-In

- 4.2.3 Rising Demand for Digital Employee Experience Platforms

- 4.2.4 Data Sovereignty and Compliance-Driven Cloud Modernization

- 4.2.5 AI-Augmented Workflow Automation in Knowledge-Heavy Workplaces

- 4.2.6 Security Consolidation Across Endpoint, Identity, and Workspace Layers

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy Application Estates

- 4.3.2 Skills Shortage in Workplace Transformation and VDI Architecture

- 4.3.3 Integration Complexity Across Multi-Vendor Collaboration Stacks

- 4.3.4 High Change-Management Burden for SME Adoption

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Belgium

- 5.5.2 Netherlands

- 5.5.3 Luxembourg

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 ServiceNow, Inc.

- 6.4.4 Citrix Systems, Inc.

- 6.4.5 Omnissa, LLC

- 6.4.6 Google LLC

- 6.4.7 Zoom Communications, Inc.

- 6.4.8 Atlassian Corporation

- 6.4.9 IBM Corporation

- 6.4.10 Salesforce, Inc.

- 6.4.11 Unily Group Limited

- 6.4.12 Workvivo Limited

- 6.4.13 Ivanti, Inc.

- 6.4.14 Accenture plc

- 6.4.15 Capgemini SE

- 6.4.16 Atos SE

- 6.4.17 Cognizant Technology Solutions Corporation

- 6.4.18 Wipro Limited

- 6.4.19 Tata Consultancy Services Limited

- 6.4.20 Infosys Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment