PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073343

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073343

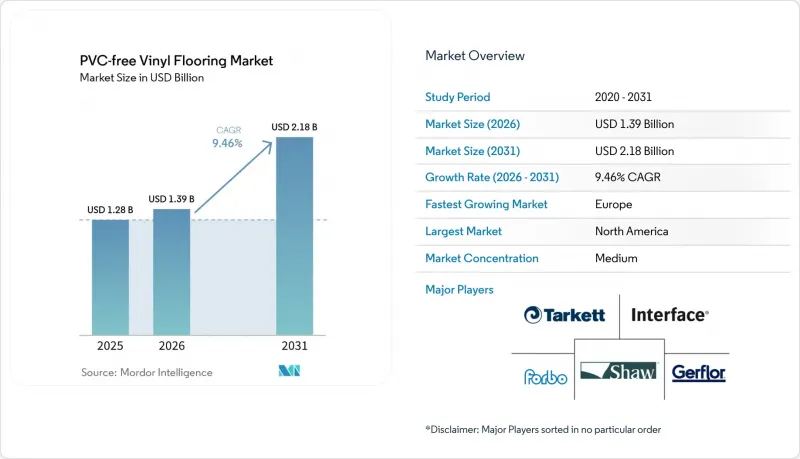

PVC-free Vinyl Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the PVC-free vinyl flooring market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.39 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 9.46% during the forecast period (2026-2031).

This report is Segmented by Format (Sheets, Tiles, Planks), Installation Method (Glue-Down, Loose-Lay, Click/Interlocking), End User (Residential, Commercial, Industrial & Specialized Vehicles), Distribution Channel (B2C/Retail, B2B/Contractors/Builders), and Geography (North America, South America, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD Billion).

Global PVC-free Vinyl Flooring Market Trends and Insights

Surge in Green-Building Certifications

LEED v5 sharpened its material transparency and embodied carbon expectations, which are influencing product selection in institutional and large commercial projects. Procurement teams are prioritizing products with verified EPDs and robust low-emission certifications that map to CDPH Section 01350 or equivalent, reinforcing demand for PVC-free resilient options in health-sensitive spaces. BREEAM guidance updated in 2025-2026 clarifies accepted emissions schemes for indoor products, which further standardizes testing and compliance in the United Kingdom and other adopting markets. As these frameworks spread across owner requirements, suppliers with third-party verified declarations and proven emissions performance are gaining specification preference. This shift supports a structural mix change in the PVC-free vinyl flooring market toward emission-verified platforms for offices, schools, and healthcare facilities.

Tightening Regulations on Chlorine and Ortho-Phthalates

United States regulatory actions under TSCA and CPSC prohibitions on certain phthalates continue to shape material decisions across interior finishes in education and childcare environments. EU REACH restrictions and SVHC authorizations continue to exert strong pressure on the use of ortho-phthalates, steering public tenders toward PVC-free chemistries when alternatives are available. The result is an expansion of chlorine-free, ortho-phthalate-free resilient offerings that avoid labeling burdens and reduce regulatory risk for public-sector buyers. These policy dynamics reinforce the case for PVC-free materials in sensitive occupancies, where health-related criteria are strongly weighted in scoring. The PVC-free vinyl flooring market, therefore, benefits from both direct chemical restrictions and buyer risk-management preferences that favor phthalate- and halogen-free platforms.

Adoption Barriers: Price Premium, Installer Acceptance, and Availability

PVC-free resilient products often cost more than commodity PVC-based alternatives, reflecting resin costs, certification investments, and smaller production runs that are still normalizing. Contractors trained on PVC-based LVT systems may need additional training on substrate preparation and adhesive compatibility when installing chlorine-free and ortho-phthalate-free platforms. Public specifications increasingly mandate emissions-compliant adhesives, which raises the importance of system-level guidance and documented compatibility to avoid warranty issues. Recognized installation and product testing standards are improving clarity for specifiers and installers by defining dimensional tolerances and performance verification. As capacity expands and training improves across regional networks, price and familiarity barriers are expected to ease in institutional and commercial channels that value verified low-VOC performance.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare and Education Demand for Low-VOC Interiors

- Bio-Polyolefin Breakthroughs Enable 100% Recyclability

- Feed-Stock Volatility for Bio-Based Polymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Planks accounted for 66.52% of revenue in 2025 and are expected to advance at 10.07% CAGR through 2031, supported by the preference for wood visuals and modularity in offices, retail, and education projects. This share confirms that architects and facility teams are adopting PVC-free alternatives that meet low-VOC requirements and deliver familiar installation rhythms. Where hygiene and seam minimization are critical, sheet formats continue to serve use cases in healthcare and cleanroom-adjacent spaces aligned with emissions criteria and cleaning protocols. Tile formats support phased renovations and visual zoning in high-traffic interiors, which suits commercial refresh cycles that prioritize minimal downtime. These options are increasingly accompanied by emissions certifications and documentation that meet CDPH Section 01350 thresholds and comparable schemes recognized by procurement teams.

The PVC-free vinyl flooring market is also seeing deeper integration of take-back considerations at the format level, with modular products positioned for selective replacement and improved material recovery. Verified low-emissions credentials and EPDs align these products with LEED v5 and BREEAM pathways, with emissions testing and accredited laboratory procedures enhancing confidence among education and healthcare clients. Tiles and planks support controlled disassembly, which aligns with EU Green Public Procurement language on take-back systems under the Circular Economy Action Plan. Sheet products remain essential in environments requiring seamless surfaces, but must demonstrate clear end-of-life handling to remain favored in public-sector bids. The PVC-free vinyl flooring market size signals that modular formats with robust documentation will continue to set the pace in specifications for institutional and commercial interiors with indoor air quality priorities.

Click-and-interlocking installations accounted for 43.67% of revenue in 2025, reflecting speed, predictability, and reduced site downtime, as adhesives are minimized or avoided. Loose-lay is the fastest-growing method, with a 11.52% CAGR, driven by end-of-life recovery considerations, simplified removal, and alignment with take-back requirements in Europe. Glue-down remains essential for heavy-traffic or specialty environments where peak bond strength and dimensional stability under dynamic loads are prioritized. Public specifications codify adhesive emissions and content rules for occupied spaces, ensuring that full systems are considered at design and procurement stages. These approaches are underpinned by performance standards that define dimensional stability, indentation resistance, and surface integrity for resilient products.

Circularity is a key theme influencing method selection, as tenders specify take-back and reuse plans, including for sports and community facilities that redeploy finished surfaces. Loose-lay systems make disassembly and reuse more practical and further reduce adhesive use, simplifying both installation and end-of-life processes. Click systems deliver consistent fit and shorter schedules that appeal to busy campuses and occupied healthcare environments, provided emissions and indoor air quality thresholds are met. Adhesive choices are documented in submittals with emissions program references that comply with CDPH Section 01350 or an equivalent, strengthening compliance narratives in public-sector bids. These conditions favor installation methods that integrate well with low-VOC adhesives, accredited emissions testing, and closed-loop collection frameworks consistent with EU public procurement guidance.

Complete Report Scope:

- By Format

- Sheets

- Tiles

- Planks

- By Installation Method

- Glue-down

- Loose-lay

- Click / Interlocking

- By End User

- Residential

- Commercial

- Industrial & Specialized Vehicles

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Flooring Stores

- Online

- Local Hardware Shops (unorganized market)

- Other Distribution Channels

- B2B/Contractors/Builders

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Geography Analysis

North America held 33.00% share in 2025 as LEED-aligned projects and emissions-based specifications remained a backbone of public and private procurement. U.S. federal and defense construction documents reference low-VOC emissions programs, which reinforce systems-based compliance for resilient floors and adhesives. Domestic capacity additions in resilient platforms and reclamation services support institutional clients that prefer short supply lines and verified take-back. The education and healthcare segments continue to provide steady volume, with an emphasis on emissions performance and assured maintenance outcomes over time. These buyers prioritize third-party testing and recognized certifications that meet CDPH Section 01350 or equivalent standards widely used in the region.

Europe is expected to pace global growth at 10.16% CAGR through 2031, reflecting the EU's Circular Economy Action Plan and the integration of take-back systems into green public procurement. Nordic ecolabel criteria and similar frameworks are tightening expectations for emissions and recycled content, which supports platforms with clear reclamation and reprocessing pathways. Public tenders in schools, hospitals, and government offices favor materials with documented emissions performance and established collection logistics. Suppliers with long-running take-back programs and verified EPDs are better positioned as minimum criteria become common within country-level procurement guidance. The PVC-free vinyl flooring market share in the region is supported by harmonized rules that promote circular design, end-of-life accountability, and consistent emissions testing.

Asia-Pacific accounts for a meaningful base with sustained growth through 2031, with activity strongest in mature markets that emphasize emissions and hygiene in healthcare and technology sectors. Standardized approaches to emissions testing and accredited laboratories continue to support adoption in pharmaceutical and medical technology facilities. Public projects in Southeast Asia are balancing cost with performance and durability, with humidity management and lifecycle maintenance shaping specifications. Regional policies on used cooking oil exports and renewable-blended fuels can tighten bio-circular feedstock markets, which the supply chain must navigate to deliver PVC-free, resilient platforms. Owner requirements in Japan and South Korea emphasize emissions and material-safety controls, which align with established low-VOC frameworks and recognized testing regimes.

- Tarkett S.A.

- Forbo Flooring Systems

- Interface Inc.

- Gerflor Group

- Mohawk Industries Inc.

- Shaw Industries Group Inc.

- Armstrong Flooring LLC

- IVC Group (Mohawk)

- Windmoller GmbH (wineo PURLINE)

- Upofloor Oy

- Ecore International

- LG Hausys Ltd.

- Beaulieu International Group (BerryAlloc)

- Amorim Cork Flooring

- Parador GmbH

- Karndean Designflooring

- Roppe Corporation

- Novalis Innovative Flooring

- NOX Corporation

- CFL Flooring

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in green-building certifications (LEED, BREEAM)

- 4.2.2 Tightening regulations on chlorine & ortho-phthalates

- 4.2.3 Healthcare & education demand for low-VOC interiors

- 4.2.4 Bio-polyolefin breakthroughs enable 100 % recyclability

- 4.2.5 EU take-back mandates in public tenders

- 4.2.6 Niche OEM uptake in electric RVs & e-buses

- 4.3 Market Restraints

- 4.3.1 Adoption Barriers (Price premium vs. conventional PVC flooring, Installer Acceptance, Supply-Chain Availability)

- 4.3.2 Limited installer familiarity & tooling

- 4.3.3 Feed-stock volatility for bio-based polymers

- 4.3.4 Dimensional-stability issues in humid climates

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Comparative Performance Benchmarking for Traditional versus PVC-free Vinyl Flooring (Durability, Acoustics, Lifecycle Cost, Maintenance, etc.)

- 4.7 Cost-Structure Benchmarking vs. Traditional LVT / SPC

- 4.8 Insights into the Latest Trends and Innovations in the Industry

- 4.9 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Format

- 5.1.1 Sheets

- 5.1.2 Tiles

- 5.1.3 Planks

- 5.2 By Installation Method

- 5.2.1 Glue-down

- 5.2.2 Loose-lay

- 5.2.3 Click / Interlocking

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial & Specialized Vehicles

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail

- 5.4.1.1 Home Centers

- 5.4.1.2 Specialty Flooring Stores

- 5.4.1.3 Online

- 5.4.1.4 Local Hardware Shops (unorganized market)

- 5.4.1.5 Other Distribution Channels

- 5.4.2 B2B/Contractors/Builders

- 5.4.1 B2C/Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab of Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tarkett S.A.

- 6.4.2 Forbo Flooring Systems

- 6.4.3 Interface Inc.

- 6.4.4 Gerflor Group

- 6.4.5 Mohawk Industries Inc.

- 6.4.6 Shaw Industries Group Inc.

- 6.4.7 Armstrong Flooring LLC

- 6.4.8 IVC Group (Mohawk)

- 6.4.9 Windmoller GmbH (wineo PURLINE)

- 6.4.10 Upofloor Oy

- 6.4.11 Ecore International

- 6.4.12 LG Hausys Ltd.

- 6.4.13 Beaulieu International Group (BerryAlloc)

- 6.4.14 Amorim Cork Flooring

- 6.4.15 Parador GmbH

- 6.4.16 Karndean Designflooring

- 6.4.17 Roppe Corporation

- 6.4.18 Novalis Innovative Flooring

- 6.4.19 NOX Corporation

- 6.4.20 CFL Flooring

7 Market Opportunities & Future Outlook

- 7.1 Closed-loop Recycling Infrastructure Build-out

- 7.2 Hybrid Bio-Composite Flooring Innovation