PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073421

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073421

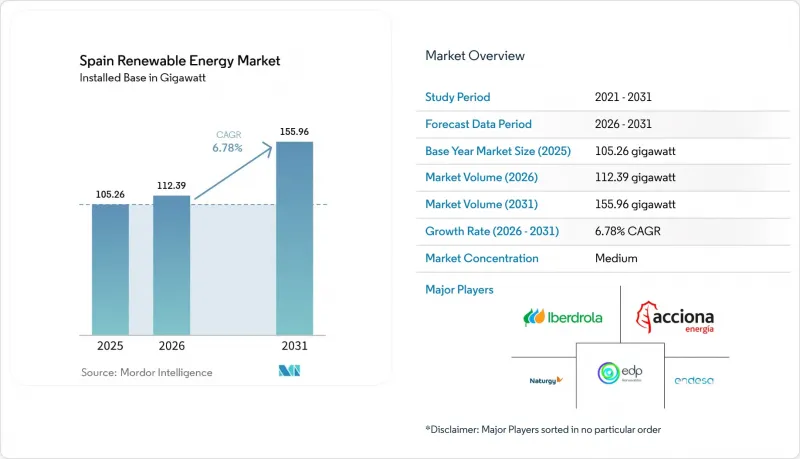

Spain Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, spain renewable energy market size in 2026 is estimated at 112.39 gigawatt, growing from 2025 value of 105.26 gigawatt with 2031 projections showing 155.96 gigawatt, growing at 6.78% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Spain Renewable Energy Market Trends and Insights

Declining Levelized Cost of Solar PV

Utility-scale solar delivered an average LCOE of EUR 29 per MWh in 2024, undercutting combined-cycle gas generation in every major node. The cost advantage reflects widespread adoption of bifacial modules and single-axis tracking that lifts yields by up to 20%, as well as aggressive EPC pricing from new Chinese entrants. Collective self-consumption rules have translated the same economics into urban rooftops, where installations expanded by 30% during 2024. Lower wholesale prices, expected from accelerated solar additions, threaten thermal margins and hasten coal retirements; however, anti-dumping probes on Asian module imports could disrupt the downward cost curve. Even so, the investment shift toward merchant or PPA-backed projects reduces dependence on government auctions and signals rising confidence in the long-term competitiveness of solar energy.

Rapid Build-Out of Onshore Wind Capacity

The repowering of early-2000s turbines using 15 MW platforms has increased capacity factors by approximately 40%, while alleviating land-use tensions in saturated regions. Developers secure sub-4% debt through long-tenor PPAs with data-center and steel offtakers, transferring volumetric risk downstream. Nonetheless, limited greenfield sites and avian-protection zones push activity toward floating offshore pilots off Galicia and the Canary Islands, where 3 GW is slated for commissioning late in the decade. Streamlined environmental reviews remain essential if Spain is to achieve an average of 5 GW of net wind additions each year and stay aligned with its 2030 target of 62 GW.

Grid Congestion and Curtailment Risk

Curtailment events tripled year-over-year in 2023 and forced 1.2 GW of solar and wind capacity offline during midday peaks in 2024, erasing EUR 180 million in revenue. REE's expansion plan encompasses 2,500 kilometers of new lines and 15 substations; however, land acquisition lags behind capacity additions, resulting in constraints through 2027. Co-located battery projects partly offset lost output; however, round-trip efficiency and cost hurdles limit their uptake. A pilot dispatch regime now prioritizes hybrid assets, signaling tougher economics ahead for standalone solar.

Other drivers and restraints analyzed in the detailed report include:

- EU Fit-for-55 and PNIEC 2023 Targets

- Corporate PPAs from Energy-Intensive Industries

- Lengthy Environmental and Permitting Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spain Solar energy accounted for 42.62% of installed capacity in 2025, confirming its leadership within the Spanish renewable energy market. Utility-scale projects in Andalusia and Extremadura, where irradiance exceeds 2,000 kWh / m2, underpin the segment's 10.09% CAGR outlook through 2031. The Spain renewable energy market size for solar is forecast to add roughly 35 GW by the decade's close, reflecting the lowest LCOE across competing resources. Wind follows as the second-largest pillar; onshore parks in Castilla-La Mancha and Aragon deliver capacity factors of 28-32%, while a 3 GW floating portfolio off Galicia and the Canary Islands seeks final permits. Hydropower supplies 20 GW, with 5.3 GW of pumped storage acting as a flexibility backbone, yet it is vulnerable to drought-driven inflow variability.

Cost competitiveness drives investor preference toward solar and wind, but technological diversification remains essential. CSP plants provide thermal storage and extend dispatch into evening peaks, mitigating price cannibalization. Bioenergy, geothermal, and ocean energy collectively contribute less than 2 GW, primarily due to limited feedstock availability, resource quality, and the nascent stage of technology readiness. Nevertheless, pumped storage expansions and battery hybrids signal a trend toward integrated resource portfolios that balance intermittency and bolster system reliability.

Complete Report Scope:

- By Technology

- Solar Energy (PV and CSP)

- Wind Energy (Onshore and Offshore)

- Hydropower (Small, Large, PSH)

- Bioenergy

- Geothermal

- Ocean Energy (Tidal and Wave)

- By End-User

- Utilities

- Commercial and Industrial

- Residential

List of Companies Covered in this Report:

- Iberdrola SA

- Acciona Energia SA

- Siemens Gamesa Renewable Energy SA

- Endesa SA

- Naturgy Energy Group SA

- EDP Renovaveis (EDPR)

- Cobra Group (ACS)

- Red Electrica Corporacion SA (REE)

- Solaria Energia y Medio Ambiente SA

- JinkoSolar Holding Co. Ltd (Spain)

- Vestas Wind Systems Spain

- Enel Green Power Espana

- Grenergy Renovables

- Forestalia Renovables

- Capital Energy

- Repsol Renovables

- Solarpack Corporacion

- X-Elio

- Abengoa Solar

- IM2 Systems SLU

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining levelized cost of solar PV

- 4.2.2 Rapid build-out of on-shore wind capacity

- 4.2.3 EU Fit-for-55 & Spain's PNIEC 2023 targets

- 4.2.4 Corporate PPAs from energy-intensive industries

- 4.2.5 Green-hydrogen export hub initiatives

- 4.2.6 Cross-border interconnectors with France & Portugal

- 4.3 Market Restraints

- 4.3.1 Grid congestion & curtailment risk

- 4.3.2 Lengthy environmental/permitting lead-times

- 4.3.3 Balancing-market revenue volatility post 2025

- 4.3.4 Battery-grade lithium supply uncertainty

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Iberdrola SA

- 6.4.2 Acciona Energia SA

- 6.4.3 Siemens Gamesa Renewable Energy SA

- 6.4.4 Endesa SA

- 6.4.5 Naturgy Energy Group SA

- 6.4.6 EDP Renovaveis (EDPR)

- 6.4.7 Cobra Group (ACS)

- 6.4.8 Red Electrica Corporacion SA (REE)

- 6.4.9 Solaria Energia y Medio Ambiente SA

- 6.4.10 JinkoSolar Holding Co. Ltd (Spain)

- 6.4.11 Vestas Wind Systems Spain

- 6.4.12 Enel Green Power Espana

- 6.4.13 Grenergy Renovables

- 6.4.14 Forestalia Renovables

- 6.4.15 Capital Energy

- 6.4.16 Repsol Renovables

- 6.4.17 Solarpack Corporacion

- 6.4.18 X-Elio

- 6.4.19 Abengoa Solar

- 6.4.20 IM2 Systems SLU

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment