PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073424

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073424

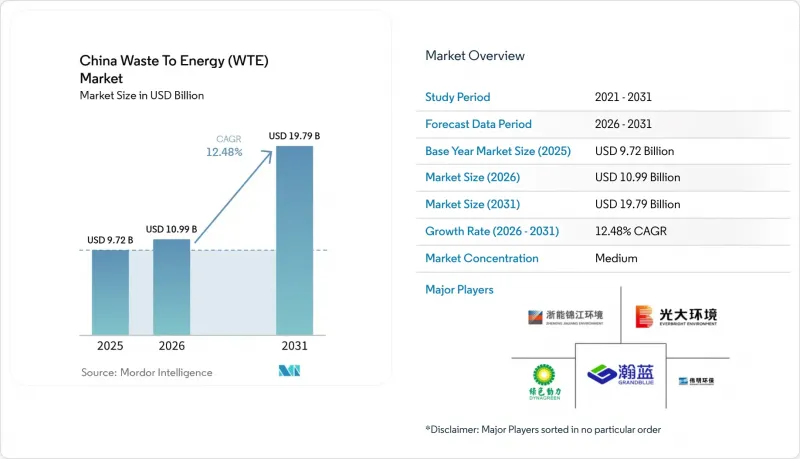

China Waste To Energy (WTE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china waste to energy market size is expected to increase from USD 9.72 billion in 2025 to USD 10.99 billion in 2026 and reach USD 19.79 billion by 2031, growing at a CAGR of 12.48% over 2026-2031.

This report is Segmented by Technology (Physical, Thermal, and Biological), Waste Type (Municipal Solid Waste, Agricultural and Agro-Industrial Residues, and More), Energy Output (Electricity, Heat, Transportation Fuels, and More), and End-User (Utilities and IPPs, Industrial Captive Plants, Transport Fuel Distributors, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

China Waste To Energy (WTE) Market Trends and Insights

Grid-Parity Large-Scale Incinerator Retrofits (Ultra-Supercritical)

Ultra-supercritical boilers operating above 25 megapascals and 580 °C raise net thermal efficiency to 32-35%, allowing plants to sell power at market rates without feed-in tariffs. Shenzhen Energy's Baoan Phase III plant, commissioned in 2025, produces 550 kWh per tonne of waste and won a 15-year power purchase agreement that undercuts coal dispatch costs. A National Energy Administration circular encourages retrofitting 180 plants above 1,200 t/d, backed by USD 1.67 billion in China Development Bank loans. Retrofit economics depend on long-term offtake contracts because spot power prices in eastern provinces dipped 12% in 2025, stretching payback periods to 11 years. Skilled labor shortages in ultra-supercritical boiler operation have prompted partnerships with Mitsubishi Heavy Industries and Hitachi Zosen for technology transfer.

National Zero-Waste City Roll-Out (113 Cities by 2027)

The framework mandates 60% landfill diversion by 2027, guaranteeing baseline feedstock for thermal and biological projects. The 113 pilot cities handled 48% of national urban waste in 2025 and allocated USD 11.82 billion to waste infrastructure, 40% of which funds anaerobic digestion. Chengdu alone budgeted USD 445.12 million for four digesters that will yield 180 million m3 of biogas annually for buses and district heating. Projects aligned with municipal master plans secure environmental permits in 14 months versus 24 months previously, trimming pre-construction financing costs by about 20%.

Stricter Dioxin/Furan Emission Caps (GB 18485-2025)

The new standard halves allowable dioxin emissions to 0.05 ng TEQ/m3 and mandates continuous monitoring. Compliance needs USD 3.48-5.56 million per plant for activated-carbon injection and real-time analyzers, slicing operating margins by up to 6 percentage points. Roughly 320 plants built before 2016 face retrofit or closure. Early movers such as Zhejiang Weiming Environment leverage compliance readiness to win 20-year concessions with inflation-indexed gate fees.

Other drivers and restraints analyzed in the detailed report include:

- AI-Optimised Dispatch of CHP Exports to District Heating

- Provincial RDF Blending Mandates for Cement Kilns

- Recycling-Led Feedstock Shortfalls in Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thermal schemes controlled 77.1% of the Chinese waste-to-energy market in 2025, supported by proven GB 18485 pathways and high tolerance of mixed waste streams. Biological treatment is gaining traction at a 17.8% CAGR because biogas attracts carbon credits and renewable gas certificates. Gasification and pyrolysis remain niche at under 2% of capacity due to tar handling and high capital intensity.

Anaerobic digestion benefits from the relaunch of the China Certified Emission Reduction scheme, which paid an average USD 13.21 per tonne CO2-eq in 2025, boosting project revenues by up to 18%. The National Energy Administration aims to triple digestion capacity to supply 30 billion m3 of biogas by 2030. This trajectory positions biological routes to gradually erode thermal dominance, though incineration still tolerates 60% moisture and unsorted feed, a capability unmatched by digestion or RDF lines.

Municipal solid waste represented 74.8% of throughput in 2025, yet agricultural and agro-industrial residues are growing at 15.6% CAGR under straw-utilization mandates that target 60% recovery by 2028. Industrial solid waste contributed 12% of feedstock, and sewage sludge 5%.

Seasonality and storage costs challenge straw projects, yet USD 6.96-11.13 per tonne collection subsidies and flexible feed-in-tariff quotas improve economics. Sludge co-incineration attracts disposal fees twice those of household waste, helping urban operators backfill capacity lost to recycling. These trends broaden the resource base for the Chinese waste-to-energy market while aligning with rural revitalization policies.

Complete Report Scope:

- By Technology

- Physical (Refuse-Derived Fuel, Mechanical Biological Treatment)

- Thermal (Incineration/Combustion, Gasification, Pyrolysis and Plasma-Arc)

- Biological (Anaerobic Digestion, Fermentation)

- By Waste Type

- Municipal Solid Waste

- Industrial Waste

- Agricultural and Agro-industrial Residues

- Sewage Sludge

- Others (Commercial, Construction, Hazardous)

- By Energy Output

- Electricity

- Heat

- Combined Heat and Power (CHP)

- Transportation Fuels (Bio-SNG, Bio-LNG, Ethanol)

- By End-user

- Utilities and IPPs

- Industrial Captive Plants

- District Heating Operators

- Transport Fuel Distributors

List of Companies Covered in this Report:

- China Everbright Environment Group Ltd

- Zheneng Jinjiang Environment Holding Co Ltd

- Zhejiang Weiming Environment Protection Co Ltd

- Grandblue Environment Co Ltd

- Dynagreen Environmental Protection Group Co Ltd

- China Tianying Inc

- Beijing Capital Eco-Environment Protection Group

- Beijing Enterprises Environment Group Ltd

- Shanghai Environment Group

- Sanfeng Environment Co Ltd

- Veolia Environnement SA (China Ops)

- Hitachi Zosen Inova AG

- Mitsubishi Heavy Industries Environmental & Chemical Eng.

- Babcock & Wilcox Enterprises Inc

- Covanta Holding Corporation

- Suez SA (China Ops)

- Keppel Seghers

- Dongjiang Environmental Co Ltd

- Tianjin Teda Environmental Protection Co Ltd

- Jiangsu Huahong Technology Co Ltd

- StockViz Top Revenue Players ? USD 0.8 Bn (others)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Policy-Driven Gate Fees & FIT Subsidies

- 4.2.2 National "Zero-Waste City" Roll-out (113 cities by 2027)

- 4.2.3 Grid-Parity Large-Scale Incinerator Retrofits (Ultra-Supercritical)

- 4.2.4 Under-the-Radar High-Value Plastics Segregation Boosting LHV

- 4.2.5 AI-Optimised Dispatch of CHP Exports to District Heating

- 4.2.6 Provincial RDF Blending Mandates for Cement Kilns

- 4.3 Market Restraints

- 4.3.1 Mainstream Rising Public Opposition & Social Licence Costs

- 4.3.2 Stricter Dioxin/Furan Emission Caps (GB 18485-2025)

- 4.3.3 Under-the-Radar Recycling-Led Feedstock Shortfalls in Tier-1 Cities

- 4.3.4 Volatile Carbon Credit Prices Reducing PPP IRRs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Physical (Refuse-Derived Fuel, Mechanical Biological Treatment)

- 5.1.2 Thermal (Incineration/Combustion, Gasification, Pyrolysis and Plasma-Arc)

- 5.1.3 Biological (Anaerobic Digestion, Fermentation)

- 5.2 By Waste Type

- 5.2.1 Municipal Solid Waste

- 5.2.2 Industrial Waste

- 5.2.3 Agricultural and Agro-industrial Residues

- 5.2.4 Sewage Sludge

- 5.2.5 Others (Commercial, Construction, Hazardous)

- 5.3 By Energy Output

- 5.3.1 Electricity

- 5.3.2 Heat

- 5.3.3 Combined Heat and Power (CHP)

- 5.3.4 Transportation Fuels (Bio-SNG, Bio-LNG, Ethanol)

- 5.4 By End-user

- 5.4.1 Utilities and IPPs

- 5.4.2 Industrial Captive Plants

- 5.4.3 District Heating Operators

- 5.4.4 Transport Fuel Distributors

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 China Everbright Environment Group Ltd

- 6.4.2 Zheneng Jinjiang Environment Holding Co Ltd

- 6.4.3 Zhejiang Weiming Environment Protection Co Ltd

- 6.4.4 Grandblue Environment Co Ltd

- 6.4.5 Dynagreen Environmental Protection Group Co Ltd

- 6.4.6 China Tianying Inc

- 6.4.7 Beijing Capital Eco-Environment Protection Group

- 6.4.8 Beijing Enterprises Environment Group Ltd

- 6.4.9 Shanghai Environment Group

- 6.4.10 Sanfeng Environment Co Ltd

- 6.4.11 Veolia Environnement SA (China Ops)

- 6.4.12 Hitachi Zosen Inova AG

- 6.4.13 Mitsubishi Heavy Industries Environmental & Chemical Eng.

- 6.4.14 Babcock & Wilcox Enterprises Inc

- 6.4.15 Covanta Holding Corporation

- 6.4.16 Suez SA (China Ops)

- 6.4.17 Keppel Seghers

- 6.4.18 Dongjiang Environmental Co Ltd

- 6.4.19 Tianjin Teda Environmental Protection Co Ltd

- 6.4.20 Jiangsu Huahong Technology Co Ltd

- 6.4.21 StockViz Top Revenue Players ? USD 0.8 Bn (others)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment