PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073442

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073442

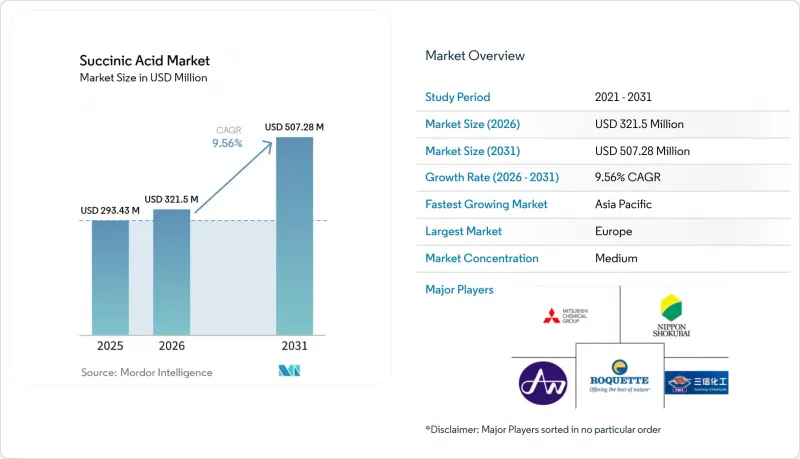

Succinic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, succinic acid market size in 2026 is estimated at USD 321.5 million, growing from 2025 value of USD 293.43 million with 2031 projections showing USD 507.28 million, growing at 9.56% CAGR over 2026-2031.

This report is Segmented Into Product Type (Petro and Bio-Based), Grade (Industrial/Technical, Food, Pharmaceuticals, and Cosmetic), Application (Industrial Chemicals, Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Succinic Acid Market Trends and Insights

Rising demand for biodegradable polymers

Polybutylene succinate (PBS) production has emerged as the primary growth catalyst for succinic acid demand, with automotive and packaging industries mandating biodegradable alternatives to conventional plastics. Technical University of Munich researchers achieved breakthrough fermentation efficiency using the marine bacterium Vibrio natriegens, reducing production time to 2-3 hours compared to traditional 24-48 hour cycles. This technological advancement addresses the critical bottleneck of fermentation scalability that previously limited bio-based succinic acid competitiveness. Polymer manufacturers increasingly specify bio-based succinic acid for PBS production to meet circular economy regulations, particularly in Europe, where extended producer responsibility frameworks penalize non-biodegradable packaging materials.

Regulatory support for bio-based chemicals

Government policy frameworks have crystallized around bio-based chemical incentives, with the U.S. Department of Energy's 2025 sustainable chemistry roundtable identifying succinic acid as a priority platform chemical for industrial decarbonization . Owing to the rising demand for bio-based chemicals, various countries are investing heavily in biotechnology initiatives. According to the Ministry of Science and Technology data from 2024, the Government of India launched the BioF3 (Biotechnology for Economy, Environment and Employment) policy to foster high-performance biotechnology manufacturing in the country . FDA recognition of succinic acid as Generally Recognized as Safe (GRAS) for food applications removes regulatory barriers for expanded usage in food and beverage formulations, with maximum allowable levels established for condiments and meat products. These regulatory endorsements create preferential market access for bio-based succinic acid producers while establishing quality standards that favor established manufacturers with proven production capabilities.

Limited commercial-scale production infrastructure

The collapse of several pioneering companies, including BioAmber, has reduced available production capacity while deterring new investment in manufacturing infrastructure. Developing regions lack the technical expertise and capital access required for fermentation facility construction, concentrating production in established chemical manufacturing hubs. The specialized nature of bio-based production requires different equipment and processes compared to traditional chemical plants, limiting the ability to repurpose existing facilities and increasing capital requirements. Feedstock supply chain development lags behind production capacity needs, particularly for non-food biomass sources that require preprocessing infrastructure investment.

Other drivers and restraints analyzed in the detailed report include:

- Expanding food and beverage usage as acidity regulator and flavor enhancer

- Growing demand in personal care and cosmetics

- Competition from alternative bio-based acids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bio-based succinic acid is projected to grow at a CAGR of 11.02% during 2026-2031, while petro-based succinic acid maintains a 58.82% market share in 2025. The higher growth rate of bio-based production reflects increasing adoption of sustainable manufacturing methods, driven by regulatory requirements and corporate environmental goals. The shift toward bio-based production aligns with global sustainability initiatives and growing environmental consciousness across industries. Petro-based production retains its market leadership due to established infrastructure and lower costs, particularly in industrial applications where price sensitivity outweighs environmental concerns.

The cost advantage of petro-based production stems from decades of process optimization and economies of scale in existing facilities. Bio-based alternatives are gaining traction in premium segments such as food, pharmaceuticals, and cosmetics, where sustainability requirements justify higher prices and consumer preferences influence purchasing decisions. These premium segments demonstrate increasing willingness to absorb the additional costs associated with bio-based production methods, driven by end-user demand for environmentally responsible products.

Complete Report Scope:

- By Product Type

- Petro-based

- Bio-based

- By Grade

- Industrial/Technical Grade

- Food Grade

- Pharmaceutical Grade

- Cosmetic Grade

- By Application

- Industrial Chemicals

- Food and Beverage

- Pharmaceuticals

- Personal Care and Cosmetics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Europe commands 31.64% market share in 2025, leveraging established regulatory frameworks supporting bio-based chemicals and mature manufacturing infrastructure. Germany and France lead regional production capacity with integrated chemical complexes that facilitate downstream processing and distribution. The region's extended producer responsibility frameworks for packaging materials create preferential demand for biodegradable polymers derived from bio-based succinic acid.

Asia-Pacific emerges as the fastest-growing region with 10.31% CAGR for 2026-2031, driven by rapid industrialization and expanding manufacturing capacity across China, India, and Southeast Asia. Hyosung's USD 1 billion investment in Vietnam for bio-based 1,4-butanediol production exemplifies the region's strategic positioning in bio-based chemical manufacturing, with the facility targeting 50,000 metric tons of annual capacity by 2026. China's dominance in chemical manufacturing provides established infrastructure for succinic acid production scale-up, while India's growing pharmaceutical and personal care industries create expanding demand for higher-grade products. The region benefits from abundant agricultural waste feedstocks, including rice straw and corn stalks that provide cost-effective raw materials for bio-based production. Government policies supporting industrial decarbonization and circular economy development create favorable conditions for bio-based chemical adoption across the region.

North America maintains a significant market presence despite facing competitive pressure from lower-cost Asian production. The U.S. Department of Agriculture's 2024 biomass supply chain report identifies abundant feedstock availability as a key competitive advantage, with established agricultural infrastructure supporting renewable raw material supply . The U.S. Department of Energy's sustainable chemistry roundtable prioritizes succinic acid as a platform chemical for industrial decarbonization, providing policy support for domestic production development. Canada's experience with BioAmber's failed commercialization provides lessons for risk management and market development strategies, highlighting the importance of realistic cost projections and market pricing assumptions.

- Roquette Freres

- Mitsubishi Chemical Group

- Nippon Shokubai Co., Ltd.

- Air Water Performance Chemical Inc.

- Jinan Finer Chemical Co., Ltd

- Anhui Sunsing Chemicals

- Haihang Group

- Henan GP Chemicals Co.,Ltd

- Kunshan Odowell Co. Ltd

- Royal DSM (Reverdia)

- Wenzhou Blue Dolphin New Material Co., Ltd

- Ensince Industry Co., Ltd

- Carl Roth GmbH + Co. KG

- Axiom Chemicals Pvt. Ltd.

- LCY Biosciences Inc.

- Fengchen Group Co.,Ltd

- Shandong Biotech

- Shandong Feiyang Chemical

- Spectrum Chemical Mfg.

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for biodegradable polymers

- 4.2.2 Regulatory support for bio-based chemicals

- 4.2.3 Expanding food and beverage usage as acidity regulator and flavor enhancer

- 4.2.4 Growing demand in personal care and cosmetics

- 4.2.5 Advancements in bio-based production technologies

- 4.2.6 Rising demand for green solvents and industrial chemicals

- 4.3 Market Restraints

- 4.3.1 High production costs

- 4.3.2 Limited commercial-scale production infrastructure

- 4.3.3 Energy-intensive purification undermining eco-benefits

- 4.3.4 Competition from alternative bio-based acids

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Petro-based

- 5.1.2 Bio-based

- 5.2 By Grade

- 5.2.1 Industrial/Technical Grade

- 5.2.2 Food Grade

- 5.2.3 Pharmaceutical Grade

- 5.2.4 Cosmetic Grade

- 5.3 By Application

- 5.3.1 Industrial Chemicals

- 5.3.2 Food and Beverage

- 5.3.3 Pharmaceuticals

- 5.3.4 Personal Care and Cosmetics

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Roquette Freres

- 6.4.2 Mitsubishi Chemical Group

- 6.4.3 Nippon Shokubai Co., Ltd.

- 6.4.4 Air Water Performance Chemical Inc.

- 6.4.5 Jinan Finer Chemical Co., Ltd

- 6.4.6 Anhui Sunsing Chemicals

- 6.4.7 Haihang Group

- 6.4.8 Henan GP Chemicals Co.,Ltd

- 6.4.9 Kunshan Odowell Co. Ltd

- 6.4.10 Royal DSM (Reverdia)

- 6.4.11 Wenzhou Blue Dolphin New Material Co., Ltd

- 6.4.12 Ensince Industry Co., Ltd

- 6.4.13 Carl Roth GmbH + Co. KG

- 6.4.14 Axiom Chemicals Pvt. Ltd.

- 6.4.15 LCY Biosciences Inc.

- 6.4.16 Fengchen Group Co.,Ltd

- 6.4.17 Shandong Biotech

- 6.4.18 Shandong Feiyang Chemical

- 6.4.19 Spectrum Chemical Mfg.

- 6.4.20 Thermo Fisher Scientific

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK