PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073481

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073481

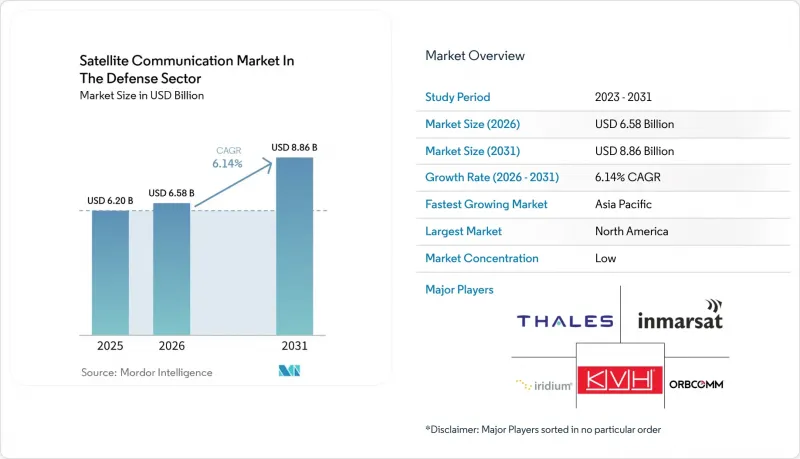

Satellite Communication In The Defense Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the satellite communication market size In The Defense Sector market is expected to grow from USD 6.20 billion in 2025 to USD 6.58 billion in 2026 and is forecast to reach USD 8.86 billion by 2031 at 6.14% CAGR over 2026-2031.

This report is Segmented by Type (Ground Equipment, Services), Platform (Land Forces, Naval Forces, Airborne), Frequency Band (L-Band, S-Band, C-Band, X-Band, Ku-Band, Ka-Band, Q/V and Optical), Application (C3, ISR, Remote Sensing, Disaster Relief, ELINT/SIGINT), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Satellite Communication Market In The Defense Sector

Growing Demand for Real-Time Data Links for Network-Centric Warfare

Net-centric operations hinge on uninterrupted, low-latency connectivity, a requirement that legacy geostationary architectures struggle to satisfy at the tactical edge. The Pentagon has allocated USD 248 million to develop jam-resistant constellations that mesh low-, medium- and geostationary-orbit assets, eliminating single points of failure. Multi-orbit terminals such as ThinKom's Ka2517 already demonstrate dynamic roaming across SES's O3b mPOWER MEO network and GEO overlays, sustaining links even under deliberate interference. Combat experience in Ukraine reinforced the value of commercial capacity backstopping military gateways, prompting doctrine updates that treat commercial SATCOM as a first-line asset rather than last-resort redundancy. Software-defined radios now integrate adaptive nulling so forces can pivot to cleaner channels when jamming spikes, and constellation-level routing algorithms balance traffic loads to maintain latency ceilings. As sensor fusion proliferates across platforms, operators gravitate toward as-a-service contracts that guarantee bandwidth elasticity without forcing hardware refresh.

Proliferation of Unmanned Systems Requiring Secure SATCOM

Unmanned aircraft, maritime vessels and ground robots are escalating theater demand for assured beyond-visual-line-of-sight links. L3Harris's Hawkeye III Lite VSAT exemplifies the new breed of rugged terminals that auto-acquire multiple orbits in minutes and sustain high-definition video streams under movement. Artificial-intelligence-enabled payloads multiply data volumes, compelling adoption of higher-frequency Ka-band and laser cross-links to contain latency. Orbit Communication Systems' low-profile MPT antennas integrate inertial navigation units for platform agility while offering encryption compliant with advanced information assurance standards. Because unsecured links translate into commandeered vehicles, military buyers insist on frequency-hopping, quantum-resistant encryption layers even for interim leases. Commercial operators have responded by carving out government tiers that reserve spectrum, harden cybersecurity and furnish priority restoration clauses.

Cyber-Intrusion and Jamming Vulnerabilities of SATCOM Networks

Adversarial advances in electronic warfare expose predictable satellite passes and standardized protocols. Incidents of GPS spoofing illustrate how even modest power transmitters can paralyze logistics nodes, while commercial gateways built for civilian uptime rarely meet military hardening thresholds. Integration of 5G-non-terrestrial-network standards, though expanding coverage, widens the attack surface as hackers exploit cross-domain protocol handshakes. Defense ministries therefore accelerate fielding of spread-spectrum, low-probability-of-intercept waveforms and quantum-safe encryption keys. These countermeasures elevate terminal complexity and price, potentially delaying replacement of legacy assets.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Deployment of Resilient Small-Satellite Constellations

- Rising Defense Budgets Allocated to SATCOM Modernization

- High Capital and Launch Costs of Next-Gen SATCOM Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ground equipment retained 60.70% share of the satellite communication market in the defense sector in 2025, underpinned by the vast inventory of fixed and mobile antennas, modems and transceivers fielded since the early 2000s. Terminal upgrades now center on electronically steered phased arrays that shrink footprint and enable multi-orbit roaming. Software-defined modems execute on-the-fly waveform shifts to maintain connectivity in contested bands, while portal-based management suites give commanders visibility into link health across fleets.

Services, however, are projected to register the strongest 7.03% CAGR, validating the shift from hardware ownership to capacity subscription. NATO's EUR 200 million contract with SES for managed O3b mPOWER bandwidth epitomizes demand for scalable throughput without new ground footprint. Under these constructs, vendors absorb satellite depreciation, obsolescence risk and launch delays, allowing militaries to redirect capital toward user equipment and cyber defense. Lifecycle analytics also reveal that service models cut total cost of ownership when constellation refresh periods fall below 10 years, a threshold many LEO-based systems now approach.

Land platforms dominated the satellite communication market size in the defense sector in 2025 with 38.10% share, reflecting decades of investment in vehicle-mounted systems and fixed command posts. Yet the airborne category leads growth at 6.74% CAGR, propelled by expanded use of medium-altitude long-endurance drones and rotary-wing ISR aircraft. L3Harris hybrid radios combine SATCOM, line-of-sight and cellular links inside a single enclosure, simplifying aircraft integration while ensuring redundancy.

Airborne growth also stems from manned aircraft modernization programs that replace legacy Ku-band radomes with lighter Ka-band or dual-band apertures to support real-time sensor streaming. Passenger-transport fleets assigned to medical evacuation or VIP missions now demand encrypted broadband comparable to commercial inflight connectivity, prompting integrators such as Gogo Business Aviation to adapt GEO-LEO-ATG hybrids for militarized configurations. As sortie rates intensify under distributed-operations doctrine, bandwidth elasticity becomes indispensable, positioning managed services as the default acquisition route.

Complete Report Scope:

- By Type

- Ground Equipment

- Antennas

- Modems and Transceivers

- Terminals (Manpack, Fly-Away, Vehicular)

- Services

- Managed SATCOM Services

- Leasing, Integration and Maintenance

- Ground Equipment

- By Platform

- Land Forces

- Naval Forces

- Airborne (Manned and Unmanned)

- By Frequency Band

- L-band

- S-band

- C-band

- X-band

- Ku-band

- Ka-band

- Q/V and Optical (Laser)

- By Application

- Command, Control and Communications (C3)

- Intelligence, Surveillance and Reconnaissance (ISR)

- Remote Sensing and Earth Observation

- Disaster Relief and Humanitarian Ops

- Electronic Intelligence (ELINT and SIGINT)

- Geography

- North America

- United States

- Canada

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Turkey

- Israel

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

North America held 40.80% of 2025 revenue, anchored by U.S. modernization programs that prioritize layered resilience and by Canada's Five Eyes commitments that require interoperable gateways. The U.S. Space Force's Commercial Augmentation Space Reserve model formalizes access to commercial capacity during crises, embedding service-level agreements that guarantee surge bandwidth and cyber priority. Industrial-base depth ensures rapid terminal fielding and secure waveform certification, enabling the region to spearhead adoption of laser cross-links and quantum-safe encryption.

Asia-Pacific is projected to record the fastest 7.78% CAGR, catalyzed by China's BeiDou expansion, India's tri-service SATCOM roadmap and Japan's Cabinet-approved X-band upgrades. Sovereignty concerns drive indigenous program funding while quad-nation exercises push interoperability standards. Australia's long-range strike and maritime patrol platforms rely on satellite backhauls that traverse vast oceanic gaps, creating steady demand for GEO-MEO-LEO hybrids. Regional market depth is further reinforced by South Korea's kilo-satellite plan, which aims to network 40-plus microsats for imagery relay and secure communications by the end of the decade.

Europe accelerates its spend in the wake of heightened security tensions. Germany's SATCOMBw Stage 3 anchors a continental shift toward sovereign capability, complemented by France's Syracuse IV and the UK's Skynet 6, both of which emphasize Ka-band throughput and electronic protection. The European Union's IRIS2 framework seeks to federate commercial and governmental demand into a single procurement vehicle, though member states debate governance and export-control implications. SES's acquisition of Intelsat consolidates GEO and MEO fleets under one European roof, but national security reviews scrutinize the company's historical joint ventures to ensure technology sovereignty.

- Thales Group

- Airbus Defence and Space

- Lockheed Martin Corp.

- Northrop Grumman Corp.

- L3Harris Technologies Inc.

- Inmarsat Communications

- ViaSat Inc.

- Iridium Communications Inc.

- SES Government Solutions

- Cobham PLC

- ST Engineering iDirect

- Hughes Network Systems (EchoStar)

- Eutelsat Communications SA

- OneWeb Ltd.

- KVH Industries Inc.

- ORBCOMM Inc.

- Thuraya (Yahsat)

- General Dynamics Mission Systems

- Gilat Satellite Networks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for real-time data links for network-centric warfare

- 4.2.2 Proliferation of unmanned systems requiring secure SATCOM

- 4.2.3 Rapid deployment of resilient small-satellite constellations

- 4.2.4 Rising defense budgets allocated to SATCOM modernisation

- 4.2.5 Adoption of laser inter-satellite links to ease RF congestion

- 4.2.6 Integration of 5G-NTN standards into military SATCOM

- 4.3 Market Restraints

- 4.3.1 Cyber-intrusion and jamming vulnerabilities of SATCOM networks

- 4.3.2 High capital and launch costs of next-gen SATCOM infrastructure

- 4.3.3 Orbital-debris mitigation constraints on constellation size

- 4.3.4 RF-spectrum sharing conflict with 5G terrestrial networks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Macroeconomic Impact Assessment

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Ground Equipment

- 5.1.1.1 Antennas

- 5.1.1.2 Modems and Transceivers

- 5.1.1.3 Terminals (Manpack, Fly-Away, Vehicular)

- 5.1.2 Services

- 5.1.2.1 Managed SATCOM Services

- 5.1.2.2 Leasing, Integration and Maintenance

- 5.1.1 Ground Equipment

- 5.2 By Platform

- 5.2.1 Land Forces

- 5.2.2 Naval Forces

- 5.2.3 Airborne (Manned and Unmanned)

- 5.3 By Frequency Band

- 5.3.1 L-band

- 5.3.2 S-band

- 5.3.3 C-band

- 5.3.4 X-band

- 5.3.5 Ku-band

- 5.3.6 Ka-band

- 5.3.7 Q/V and Optical (Laser)

- 5.4 By Application

- 5.4.1 Command, Control and Communications (C3)

- 5.4.2 Intelligence, Surveillance and Reconnaissance (ISR)

- 5.4.3 Remote Sensing and Earth Observation

- 5.4.4 Disaster Relief and Humanitarian Ops

- 5.4.5 Electronic Intelligence (ELINT and SIGINT)

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 Turkey

- 5.5.5.3 Israel

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thales Group

- 6.4.2 Airbus Defence and Space

- 6.4.3 Lockheed Martin Corp.

- 6.4.4 Northrop Grumman Corp.

- 6.4.5 L3Harris Technologies Inc.

- 6.4.6 Inmarsat Communications

- 6.4.7 ViaSat Inc.

- 6.4.8 Iridium Communications Inc.

- 6.4.9 SES Government Solutions

- 6.4.10 Cobham PLC

- 6.4.11 ST Engineering iDirect

- 6.4.12 Hughes Network Systems (EchoStar)

- 6.4.13 Eutelsat Communications SA

- 6.4.14 OneWeb Ltd.

- 6.4.15 KVH Industries Inc.

- 6.4.16 ORBCOMM Inc.

- 6.4.17 Thuraya (Yahsat)

- 6.4.18 General Dynamics Mission Systems

- 6.4.19 Gilat Satellite Networks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment