PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061317

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061317

Software-Defined Satellite (SDS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

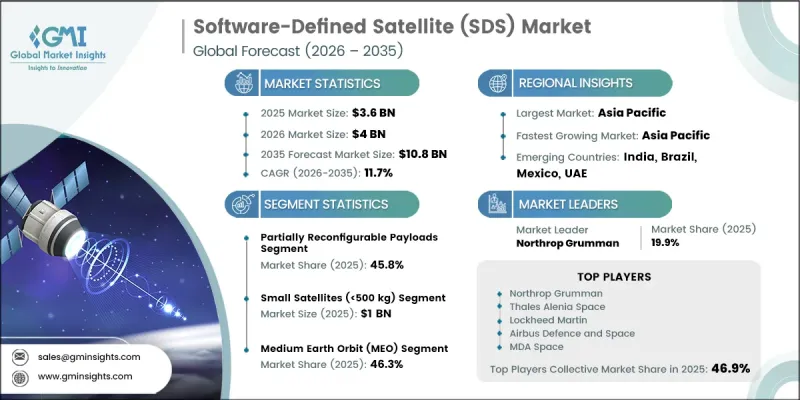

The Global Software-Defined Satellite Market was valued at USD 3.6 billion in 2025 and is estimated to grow at a CAGR of 11.7% to reach USD 10.8 billion by 2035.

Growth across the software-defined satellite industry is driven by the increasing demand for flexible and efficient satellite operations, rising integration with advanced communication ecosystems, and the continued expansion of satellite networks that require adaptive management capabilities. As satellite operators seek greater operational agility, software-defined architectures are becoming increasingly important for optimizing resource utilization and enhancing network performance. Growing demand for high-capacity communication services and evolving defense requirements are further supporting market expansion. These systems enable operators to dynamically manage satellite resources, improve service delivery, and respond more effectively to changing connectivity needs. In addition, advancements in digital technologies are accelerating the transition from conventional satellite architectures toward software-centric platforms capable of supporting more intelligent and responsive operations. As global connectivity requirements continue to increase, software-defined satellites are emerging as a critical technology for improving efficiency, scalability, and performance across modern satellite communication networks, creating strong growth opportunities throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.6 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 11.7% |

The software-defined satellite market is also benefiting from the rapid expansion of low Earth orbit satellite deployments and the increasing need for scalable satellite infrastructure. As the number of operational satellites continues to rise, network management becomes more complex and requires greater flexibility in resource allocation and operational control. Software-defined architectures enable real-time optimization of network resources while improving overall system efficiency and reducing operational complexity. By leveraging software-driven functionality, operators can accelerate service deployment, improve scalability, and enhance network adaptability. This transition toward more agile and software-enabled satellite operations is expected to remain a key growth driver through 2030 and beyond.

The partially reconfigurable payloads segment accounted for 45.8% share in 2025. The segment's leadership position is supported by its ability to deliver a practical combination of operational flexibility and cost efficiency. These payload configurations allow operators to modify selected performance parameters while maintaining manageable system complexity. Their compatibility with existing satellite infrastructure and strong suitability for communication-focused applications continue to support widespread adoption across the industry.

The small satellites (below 500 kilograms) segment generated USD 1 billion in 2025. Segment growth is being driven by increasing deployment within large satellite networks and the economic advantages associated with lower manufacturing and launch costs. Small satellites offer faster deployment timelines and provide operators with a scalable approach to expanding communication capabilities. Their growing role in supporting commercial connectivity services and satellite-based data applications continues to strengthen demand across the market.

North America Software-Defined Satellite Market accounted for 37.2% share in 2025. Regional market expansion is supported by the strong presence of satellite manufacturers, technology developers, and communication infrastructure providers. Increasing investment in advanced satellite platforms and next-generation connectivity solutions is driving demand for software-centric satellite architectures throughout the region. In addition, efforts to improve communication coverage and strengthen connectivity across underserved locations are contributing to broader adoption of software-defined satellite technologies. These factors continue to position North America as a key growth center within the global market.

Key companies operating in the Global Software-Defined Satellite Industry include Thales Alenia Space, Airbus Defence and Space, Lockheed Martin, Boeing, MDA Space, OHB System, CAST, Mitsubishi Electric, Maxar Technologies, Northrop Grumman, SpaceX, Viasat, OneWeb, Telesat, AST SpaceMobile, and Planet Labs. Participants in the software-defined satellite market are pursuing a variety of strategies to strengthen their competitive position and expand their market presence. Companies are investing heavily in research and development to enhance satellite flexibility, improve digital payload capabilities, and optimize software-driven resource management. Strategic partnerships with telecommunications providers, government agencies, and technology organizations are enabling broader deployment opportunities and accelerating innovation. Many market participants are also focusing on developing scalable satellite platforms that support evolving connectivity requirements while reducing operational costs. Expansion of satellite constellations, modernization of ground infrastructure, and integration with advanced communication networks remain key priorities. In addition, companies are emphasizing technological differentiation, service innovation, and global market expansion to strengthen customer relationships and secure a larger share of the rapidly growing software-defined satellite market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Payload flexibility level trends

- 2.2.2 Satellite mass trends

- 2.2.3 Network architecture trends

- 2.2.4 Orbit type trends

- 2.2.5 End-User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for flexible and reconfigurable satellite operations

- 3.2.1.2 Rising integration of satellites with 5G and non-terrestrial networks (NTN)

- 3.2.1.3 Expansion of low orbit (LEO) satellite constellations

- 3.2.1.4 Growing defense and secure communication requirements

- 3.2.1.5 Rising global demand or high throughput and data intensive connectivity services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High complexity in software integration and system interoperability

- 3.2.2.2 Regulatory and spectrum coordination challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of digital twin technology in satellite operations

- 3.2.3.2 Emergence of software-defined payload marketplaces and open architectures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Payload Flexibility Level, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fully reconfigurable payloads

- 5.3 Partially reconfigurable payloads

- 5.4 Limited reconfigurable payloads

Chapter 6 Market Estimates and Forecast, By Satellite Mass, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Small satellites (<500 kg)

- 6.3 Medium satellites (500-1,000 kg)

- 6.4 Large satellites (1,000-2,500 kg)

- 6.5 Heavy satellites (>2,500 kg)

Chapter 7 Market Estimates and Forecast, By Network Architecture, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Standalone satellites

- 7.3 Constellation architecture

Chapter 8 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Low earth orbit (LEO)

- 8.3 Medium earth orbit (MEO)

- 8.4 Geostationary earth orbit (GEO)

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial satellite operators

- 9.3 Government & civil agencies

- 9.4 Defense & military organizations

- 9.5 Research & academic institutions

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Northrop Grumman

- 11.1.2 Thales Alenia Space

- 11.1.3 Lockheed Martin

- 11.1.4 Airbus Defence and Space

- 11.1.5 MDA Space

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Boeing

- 11.2.1.2 Maxar Technologies

- 11.2.1.3 Viasat

- 11.2.1.4 Telesat

- 11.2.1.5 Planet Labs

- 11.2.2 Asia Pacific

- 11.2.2.1 Mitsubishi Electric

- 11.2.2.2 CAST

- 11.2.3 Europe

- 11.2.3.1 OHB System

- 11.2.3.2 OneWeb

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 SpaceX

- 11.3.2 AST SpaceMobile