PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083095

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083095

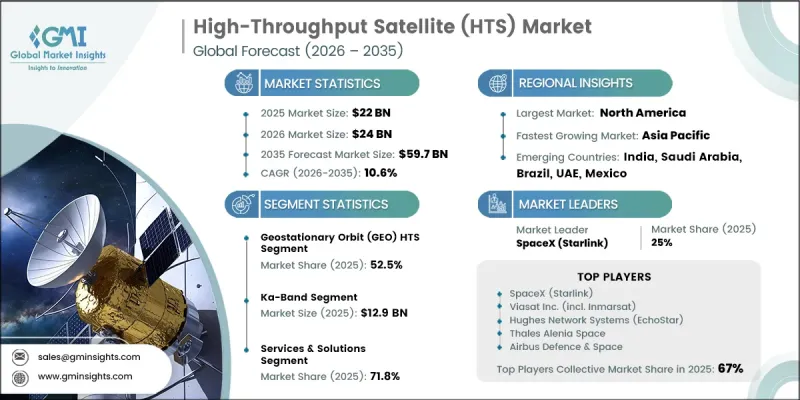

High-Throughput Satellite (HTS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global High-Throughput Satellite Market was valued at USD 22 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 59.7 billion by 2035.

The market is experiencing strong expansion due to increasing requirements for reliable high-speed broadband services in areas with limited terrestrial connectivity. Growing adoption of in-flight connectivity solutions in commercial aviation, rising government and defense requirements for high-capacity satellite communication networks and accelerating digital transformation across maritime industries are creating significant growth opportunities. The increasing volume of data-intensive applications is also encouraging organizations to adopt scalable satellite capacity solutions. Advancements in satellite technologies, including flexible satellite architecture, integrated multi-orbit systems, and improved ground infrastructure, are transforming the economics and accessibility of satellite-based connectivity services. HTS solutions are becoming increasingly important for bridging connectivity gaps and supporting enterprise, government, and consumer communication needs across diverse environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22 Billion |

| Forecast Value | $59.7 Billion |

| CAGR | 10.6% |

The high-throughput satellite market is gaining momentum as global demand for broadband access continues to rise, particularly in regions where conventional communication infrastructure remains difficult or expensive to deploy. HTS technology is emerging as an effective connectivity option for rural communities, remote locations, maritime operations, and other areas requiring dependable communication networks. Market growth is supported by increasing broadband adoption, expanding aviation connectivity services, growing defense communication requirements, rising maritime digitalization, and greater enterprise reliance on high-volume data transmission. The integration of advanced satellite designs, multi-orbit capabilities, and cloud-based ground systems is improving operational efficiency and reshaping service models throughout the satellite communication industry.

The geostationary orbit (GEO) HTS segment held a 52.5% share in 2025. This leadership position is supported by extensive coverage capabilities, established satellite infrastructure, and strong adoption across broadband, enterprise, and government communication applications. GEO satellites provide consistent wide-area connectivity from fixed orbital locations, making them a preferred choice for long-term communication agreements in aviation, maritime, and public sector applications. The availability of mature ground infrastructure, compatibility with existing user terminals, and suitability for applications where ultra-low latency is not essential continue to support sustained demand for GEO-based HTS solutions despite increasing competition from alternative orbital platforms.

The Ka-band segment generated USD 12.9 billion in 2025. The segment's growth is driven by its high spectral efficiency, expanded bandwidth capacity, and compatibility with advanced HTS satellite platforms that utilize focused spot beam technology. Ka-band systems offer high data throughput, smaller terminal requirements, and competitive service costs, making them widely adopted across broadband connectivity, aviation communication, maritime VSAT services, and enterprise networking solutions. Its widespread integration into modern high-capacity satellite systems continues to reinforce its market leadership throughout the forecast period.

North America High-Throughput Satellite Market accounted for 38.2% share in 2025, supported by a highly developed satellite communication ecosystem, strong demand from government and defense organizations, and the presence of established commercial satellite operators. The region continues to benefit from significant investments in advanced satellite connectivity infrastructure and innovative communication solutions. Regulatory developments, including the FCC's Supplemental Coverage from Space framework, have created additional opportunities for satellite operators to expand connectivity services beyond conventional applications. These advancements are helping broaden the role of HTS technology in consumer, enterprise, and government communication networks while strengthening North America's position as a major hub for satellite connectivity development.

Prominent players operating in the global high-throughput satellite industry are Thales Alenia Space, SpaceX (Starlink), Gilat Satellite Networks, Airbus Defence & Space, ViaSat Inc., MDA Space, Hughes Network Systems (EchoStar), ST Engineering iDirect, Boeing Satellite Systems International, Intellian Technologies, Mitsubishi Electric Corporation (MELCO), Comtech Telecommunications, and ThinKom Solutions. Companies operating in the high-throughput satellite market are implementing strategies focused on technology innovation, network expansion, strategic partnerships, and service diversification to strengthen their competitive positions. Key players are investing in next-generation satellite platforms, advanced payload technologies, flexible network architectures, and enhanced ground systems to improve capacity and operational efficiency. Businesses are also expanding their service portfolios, developing solutions for emerging connectivity applications, and forming collaborations with telecom operators, government agencies, and commercial enterprises.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Orbit trends

- 2.2.2 Frequency band trends

- 2.2.3 Component trends

- 2.2.4 Application trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-speed broadband connectivity in underserved and remote regions

- 3.2.1.2 Expansion of in-flight connectivity (IFC) services in commercial aviation

- 3.2.1.3 Increasing demand for high-capacity satellite networks from defense and government sectors

- 3.2.1.4 Rapid growth in maritime digitalization and offshore connectivity requirements

- 3.2.1.5 Growing deployment of HTS-enabled cellular backhaul networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital expenditure and long satellite deployment cycles

- 3.2.2.2 Spectrum allocation constraints and regulatory complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of HTS with direct-to-device (D2D) satellite connectivity

- 3.2.3.2 Expansion of HTS deployment for disaster recovery and emergency communication networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Orbit, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Geostationary orbit (GEO) HTS

- 5.3 Medium earth orbit (MEO) HTS

- 5.4 Low earth orbit (LEO) HTS

Chapter 6 Market Estimates and Forecast, By Frequency Band, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Ka-band

- 6.3 Ku-band

- 6.4 C-band

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Space segment

- 7.3 Ground segment

- 7.4 Services & solutions

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Broadband internet access

- 8.3 Enterprise networks

- 8.4 Government & defense communication

- 8.5 Mobility services

- 8.5.1 Aviation connectivity

- 8.5.2 Maritime connectivity

- 8.5.3 Land connectivity

- 8.6 Cellular backhaul

- 8.7 Disaster recovery & emergency communications

Chapter 9 Market Estimates and Forecast, By End-user, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Telecom operators

- 9.3 Internet service providers (ISPs)

- 9.4 Aviation industry

- 9.5 Maritime industry

- 9.6 Government & military

- 9.7 Energy & utilities

- 9.8 Media & entertainment

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 SpaceX (Starlink)

- 11.1.2 Viasat Inc. (incl. Inmarsat)

- 11.1.3 Hughes Network Systems (EchoStar)

- 11.1.4 Thales Alenia Space

- 11.1.5 Airbus Defence & Space

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Boeing Satellite Systems International

- 11.2.1.2 MDA Space

- 11.2.1.3 Comtech Telecommunications

- 11.2.1.4 ThinKom Solutions

- 11.2.2 Asia Pacific

- 11.2.2.1 Mitsubishi Electric Corporation (MELCO)

- 11.2.2.2 ST Engineering iDirect

- 11.2.2.3 Intellian Technologies

- 11.2.3 Europe

- 11.2.3.1 Gilat Satellite Networks

- 11.2.1 North America