PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073498

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073498

United States Health and Medical Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

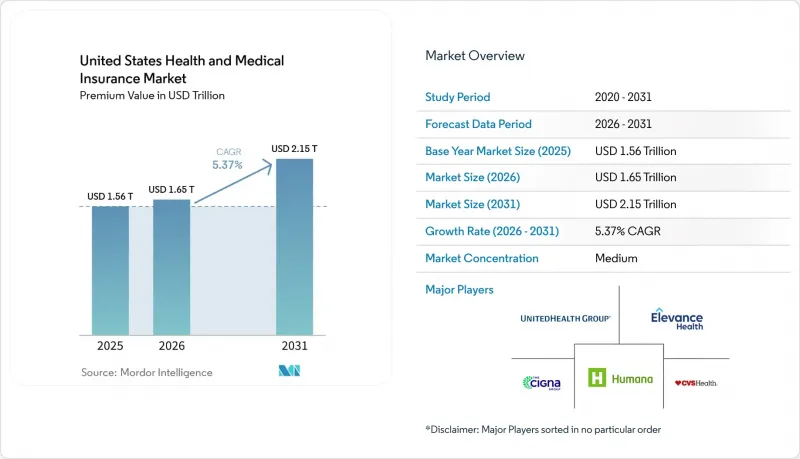

According to Mordor Intelligence, the united states health and medical insurance market size in terms of premium value is expected to increase from USD 1.56 trillion in 2025 to USD 1.65 trillion in 2026 and reach USD 2.15 trillion by 2031, growing at a CAGR of 5.37% over 2026-2031.

This report is Segmented by Coverage Type (Employer-Sponsored, Individual/ACA, and More), Plan Type (HMO, PPO, EPO, POS, HDHP), Insurance Type (Major Medical, Medicare Supplement, and More), Distribution Channel (Direct, Brokers/Agents, Consultants, Online Exchanges), and Geography (Northeast, Midwest, South, West). Forecasts in Value (USD).

United States Health and Medical Insurance Market Trends and Insights

Rising Healthcare Costs & Aging Population Fuel Coverage Expansion

Medical trend remains elevated in 2026, with carriers pointing to GLP-1 uptake and specialty drug costs that supported the largest ACA rate filings since 2018, reflected in a median requested increase for 2026 Marketplace plans. This demographic shift intersects with sustained medical cost inflation-insurers reported an 18% median proposed rate increase for 2026 ACA Marketplace plans, the largest since 2018, driven by GLP-1 drug utilization, specialty medication proliferation, and provider consolidation that elevates contracted reimbursement rates. If enhanced premium tax credits do not extend, modeling points to higher gross benchmark premiums in 2026 and a multi-year trajectory of premium growth as healthier individuals exit, which reshapes the risk pool in the United States health and medical insurance market. In Medicare Advantage, carriers are moving members toward HMO structures to strengthen referral controls and align cost management with narrower networks, an approach reflected in broad HMO access for beneficiaries in 2026. Plans are also adjusting supplemental benefits and product features to absorb revenue headwinds from the V28 risk-adjustment transition and are reallocating dollars from lower-value benefits to sustain actuarial balance under the new model.

ACA Marketplace Enrollment Doubling Creates Individual Market Momentum

ACA Marketplace enrollment more than doubled from 11 million in 2020 to over 24 million in 2025, powered by the American Rescue Plan's elimination of the 400% federal poverty level subsidy cliff and the reduction of maximum premium contributions to 8.5% of income. A large share of enrollees now falls within the 100% to 150% FPL range, which increases sensitivity to premium changes if temporary credits lapse in 2026 and may compress the United States health and medical insurance market in the individual segment. State-based exchanges are using reinsurance and Section 1332 waiver strategies to stabilize premiums and reduce federal pass-through spending, as seen in Nevada's public option that is expected to generate material pass-through savings over its early years. Similar initiatives in Colorado and Washington show how state-led designs that cap reimbursement levels and set premium targets can build enrollment in products that compete on price without eroding network adequacy. These strategies underpin a more resilient individual market if federal support becomes intermittent, although the near-term adjustment to the subsidy cliff remains a headwind in the United States health and medical insurance market.

ACA Subsidy Cliff Threatens to Reverse Individual Market Gains

The scheduled lapse of enhanced ACA premium tax credits as of January 1, 2026, restores the 400% FPL eligibility cap and increases required premium contributions across income bands, which raises out-of-pocket premiums for subsidized households and pressures retention in the United States health and medical insurance market. Pricing for 2026 exchange plans reflects expectations of higher adverse selection if the credits are not extended and incorporates broader medical trend pressures observed in rate filings for 2026. Surveys show many enrollees have limited ability to absorb higher monthly payments, a factor that could reduce take-up among middle-income households if offsets are not available. Some state-based exchanges have contingency measures funded through Section 1332 pass-through dollars, but states on the federal platform lack such backstops, which may widen geographic disparities in affordability. The near-term risk is a smaller and less balanced risk pool in individual coverage, with downstream effects on plan design, network composition, and pricing strategies across the United States health and medical insurance market.

Other drivers and restraints analyzed in the detailed report include:

- Medicaid Managed Care Reaches Saturation as States Navigate Post-PHE Acuity Mismatch

- Employer ICHRAs & QSEHRAs Shifting Coverage to Individual Market

- Medical Loss Ratio Pressure Forces Plan Design Austerity Across Segments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Employer-sponsored insurance led with a 49.33% share in 2025 of the United States health and medical insurance market, reflecting large employer inertia, Section 125 tax treatment, and the use of broad networks to support workforce retention despite rising plan costs. Medicare Advantage is projected as the fastest-growing coverage type at a 9.73% CAGR from 2026 to 2031, which cements MA as a core growth engine within the United States health and medical insurance market size as older adults shift from fee-for-service Medicare into coordinated products. Growth aligns with benefit stability under 2026 payment updates, continued access to behavioral health telehealth, and the expansion of chronic and dual-eligible special needs plans that target higher-acuity cohorts with care coordination models. The ACA individual market doubled membership from 2020 to 2025 under enhanced subsidies, but pending policy shifts introduce uncertainty in retention if subsidies remain lapsed beyond 2026. Medicaid managed care holds a stable enrollment base after the end of continuous coverage, with state capitation approaches adjusting to revised acuity and utilization profiles.

Medicare Advantage's momentum is supported by the demographic shift and by the share of beneficiaries enrolled in MA surpassing half of eligible Medicare members, a threshold that reinforces competitive intensity in plan design and quality performance. Carriers are leaning toward HMO structures to reinforce utilization controls through primary care gatekeeping and to align network economics with lower premiums for price-sensitive members. Star Ratings changes for 2026, and risk-adjustment model updates are prompting targeted investments in HEDIS measures and experience scores to sustain quality bonus payments over the medium term. Military, government, and other public programs continue steady enrollment linked to statutory eligibility and appropriations, with limited volatility relative to commercial lines. These dynamics collectively sustain a mixed demand profile across the United States health and medical insurance market, where government programs set the pace of growth while employer groups carry the largest premium base.

Preferred provider organizations held 48.35% of 2025 enrollment, underscoring member preference for broader access and the willingness of employers to fund flexibility when the labor market is tight, even as PPO offerings shrink in MA lines where carriers favor HMO designs for cost control. High-deductible health plans with HSAs are expected to post the fastest growth at an 11.38% CAGR through 2031, supported by higher statutory HSA contribution limits for 2026, expanded use of price transparency tools, and employer adoption of defined-contribution philosophies that cap premium growth in the United States health and medical insurance market. HMO access in Medicare Advantage remains widespread in 2026 and aligns with benefit management strategies that emphasize primary care alignment and referral pathways. EPO and POS products serve niche preferences for network structure and price, balancing narrower networks against premium advantages in selected geographies. The United States health and medical insurance market continues to support a spectrum of plan types as carriers match benefit designs to employer and beneficiary cost-sharing preferences.

HDHP adoption has grown within employer-sponsored coverage, correlating with long-running trends in benefit cost shifting and increased availability of employer contributions to HSAs that support out-of-pocket expenses. The United States health and medical insurance industry is also adapting to state mandates for behavioral health and other categories that must be embedded into compliant plan designs, which may narrow the premium gap between HDHP and traditional plans in some states. Within Medicare Advantage, carriers are consolidating plan portfolios into structures that allow tighter formulary management and focused networks to align with MLR requirements and quality performance goals. Direct coordination with provider organizations supports plan designs that balance utilization controls with access for high-need members. As employer and MA plan portfolios evolve, the United States health and medical insurance market presents a diversified set of options that align with different price and access trade-offs.

Complete Report Scope:

- By Coverage Type

- Employer-Sponsored

- Individual (ACA / Non-Group)

- Medicaid Managed Care

- Medicare Advantage

- Military / Government (TRICARE, VA, FEHBP)

- By Plan Type

- HMO

- PPO

- EPO

- POS

- HDHP / Consumer-Driven

- By Insurance Type

- Major Medical (Comprehensive)

- Medicare Supplement

- Dental

- Hospital Indemnity / Limited Benefit

- Vision

- Short-Term Medical

- Other Ancillary (Accident, Critical Illness)

- By Distribution Channel

- Direct to Consumer

- Brokers & Agents

- Employer Benefit Consultants

- Online Marketplaces / Exchanges

- By Region

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- UnitedHealth Group

- CVS Health (Aetna)

- Elevance Health (Blue Cross Blue Shield)

- Cigna Group

- Humana

- Centene

- Kaiser Permanente

- Health Care Service Corp (HCSC)

- Molina Healthcare

- GuideWell (Florida Blue)

- Independence Health Group

- Highmark Health

- Blue Cross Blue Shield of Alabama

- Blue Cross Blue Shield of Michigan

- Blue Cross Blue Shield of North Carolina

- Medica

- Oscar Health

- Bright Health

- Clover Health

- Evernorth

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising healthcare costs & aging population

- 4.2.2 Expansion of ACA subsidies & Marketplace enrollment

- 4.2.3 Growth in Medicaid managed care adoption by states

- 4.2.4 Employer ICHRAs & QSEHRAs shifting coverage to individual market

- 4.2.5 AI-driven risk stratification enabling micro-insurance offerings

- 4.2.6 Permanent telehealth reimbursement parity expanding virtual-care coverage

- 4.3 Market Restraints

- 4.3.1 Regulatory uncertainty around ACA subsidy extension

- 4.3.2 Rising medical loss ratios squeezing insurer margins

- 4.3.3 State-level public-option initiatives intensifying price competition

- 4.3.4 Escalating cybersecurity & data-privacy compliance costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Coverage Type

- 5.1.1 Employer-Sponsored

- 5.1.2 Individual (ACA / Non-Group)

- 5.1.3 Medicaid Managed Care

- 5.1.4 Medicare Advantage

- 5.1.5 Military / Government (TRICARE, VA, FEHBP)

- 5.2 By Plan Type

- 5.2.1 HMO

- 5.2.2 PPO

- 5.2.3 EPO

- 5.2.4 POS

- 5.2.5 HDHP / Consumer-Driven

- 5.3 By Insurance Type

- 5.3.1 Major Medical (Comprehensive)

- 5.3.2 Medicare Supplement

- 5.3.3 Dental

- 5.3.4 Hospital Indemnity / Limited Benefit

- 5.3.5 Vision

- 5.3.6 Short-Term Medical

- 5.3.7 Other Ancillary (Accident, Critical Illness)

- 5.4 By Distribution Channel

- 5.4.1 Direct to Consumer

- 5.4.2 Brokers & Agents

- 5.4.3 Employer Benefit Consultants

- 5.4.4 Online Marketplaces / Exchanges

- 5.5 By Region

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 UnitedHealth Group

- 6.4.2 CVS Health (Aetna)

- 6.4.3 Elevance Health (Blue Cross Blue Shield)

- 6.4.4 Cigna Group

- 6.4.5 Humana

- 6.4.6 Centene

- 6.4.7 Kaiser Permanente

- 6.4.8 Health Care Service Corp (HCSC)

- 6.4.9 Molina Healthcare

- 6.4.10 GuideWell (Florida Blue)

- 6.4.11 Independence Health Group

- 6.4.12 Highmark Health

- 6.4.13 Blue Cross Blue Shield of Alabama

- 6.4.14 Blue Cross Blue Shield of Michigan

- 6.4.15 Blue Cross Blue Shield of North Carolina

- 6.4.16 Medica

- 6.4.17 Oscar Health

- 6.4.18 Bright Health

- 6.4.19 Clover Health

- 6.4.20 Evernorth

7 Market Opportunities & Future Outlook

- 7.1 Introduce or scale behavioral health coverage bundles to meet consumer expectations.

- 7.2 Develop affordable hybrid models with protections for cost-sensitive consumers.