PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073503

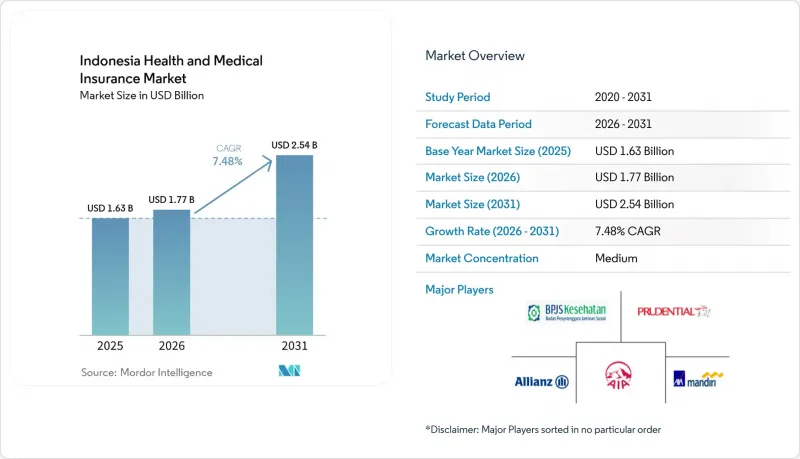

Indonesia Health and Medical Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the indonesia health and medical insurance market size was valued at USD 1.63 billion in 2025 and is estimated to grow from USD 1.77 billion in 2026 to reach USD 2.54 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031).

This report is Segmented by Product Type (Private Medical Insurance and Public or Social Security Schemes), Distribution Channel (Brokers or Agents, Bancassurance, Direct-To-Consumer, and Other Channels), and End-User (Individuals or Households, SMEs, and Large Corporates). Market Forecasts are in Value in USD.

Indonesia Health and Medical Insurance Market Trends and Insights

Near-Universal JKN Coverage Establishing Baseline Insurance Literacy

BPJS Kesehatan reached 99.34% population coverage, or 283 million participants, by October 2025, which establishes near-universal access to primary and catastrophic care and shifts private insurance interest toward enhancements in service quality and speed. The Ministry of Health set a coordination of benefits framework under Decree KMK 1366 of 2024 that legitimizes private cover for cost differences when JKN participants upgrade hospital class or seek services beyond national tariffs, with caps designed to prevent excessive balance billing. This policy standardizes how commercial supplements integrate with JKN, which reduces consumer confusion and establishes a clear role for private plans as enhancement layers rather than substitutes for the universal base. With universal coverage in place, private products compete primarily on network breadth, referral flexibility, and non-formulary medication access that JKN may not prioritize due to tariff constraints. As the coordination framework matures, insurers can design standardized top-up offers tied to specific hospital class upgrades, which supports product clarity and reduces claims friction across providers.

Rising Middle-Class Demand for Private Healthcare Network Access

Indonesia's middle class has been central to household spending, even as its headcount moved from 57.33 million in 2019 to 47.85 million in 2024. Higher-income professionals in financial and insurance services earned above the national average, which sustains paying capacity for supplementary cover that improves access and convenience. Middle-class households tend to value shorter waiting times and cashless access in private hospitals, reinforcing demand for private plans that bypass referral protocols and offer broader specialist choices. Consistent growth in digital financial services and aggregator platforms also reduces frictions in price discovery, which nudges middle-class buyers toward transparent, comparable plans from multiple insurers. These conditions allow the Indonesian health insurance market to attract first-time supplementary buyers who want predictable out-of-pocket costs when receiving higher-tier services than those covered by JKN.

Accelerating medical inflation far above headline inflation

Health care cost trends continue to diverge from consumer prices, with medical inflation for employer retiree populations rising 26.5% in 2022 and 20.48% in 2023. Elevated loss ratios in 2025 in both life and general segments show that repricing lags claim growth, compelling tighter underwriting and benefit redesign. Inpatient care drives substantially higher risk than clinic visits, with medicines and treatment forming large shares of mean expense, which pushes carriers toward formulary management and network steerage. These pressures lead employers to formalize group coverage and invest in managed care and wellness programs, which gradually improve trend lines but take time to manifest in claims experience. The Indonesian health insurance market experiences mixed effects, with short-term premium increases offset by more sustainable product constructs over the forecast.

Other drivers and restraints analyzed in the detailed report include:

- Double-Digit Medical Inflation Pressuring Employers to Formalize Group Benefits

- Digital Bank & E-Wallet Distribution Unlocking Micro-Insurance

- Data localization and PDP Law compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public and social security schemes are expected to account for 71.62% of the Indonesian health insurance market in 2025, with private medical insurance projected as the fastest-growing segment at a 9.02% CAGR through 2031. The coordination of benefits framework under KMK 1366 of 2024 allows private insurers to cover capped cost differences when JKN participants upgrade hospital classes or seek services beyond standard tariffs. This framework positions private insurance as an enhancement layer, enabling products focused on room class upgrades, access to medications beyond JKN formularies, and faster specialist consultations, appealing to households seeking higher service levels. Elevated loss ratios in individual products during 2025 have increased repricing pressures and driven the adoption of utilization reviews and clinical governance to manage costs. The market benefits from stable public coverage as a universal base, with private plans addressing service quality gaps valued by households and employers.

Group health pools remain central as employers prioritize predictable budgets and structured care pathways. Individual products are evolving with clearer co-payment terms and simplified benefits. Enhanced medical governance under POJK 36 of 2025 and insurer-level Medical Advisory Boards improve clinical consistency and consumer confidence. Managed care strategies, pharmacy controls, and negotiated provider arrangements help private insurers curb high-cost inpatient episodes. Rising product literacy through JKN participation boosts upgrade-oriented private plans in urban centers, sustaining private segment growth while public schemes dominate enrollment.

Complete Report Scope:

- By Insurance Product Type

- Private Medical Insurance (PMI)

- Individual Policy Coverage

- Group Policy Coverage

- Public / Social Security Schemes

- Private Medical Insurance (PMI)

- By Distribution Channel

- Brokers / Agents

- Banks (Bancassurance)

- Direct-to-Consumer

- Other Channels (Affinity, Associations, etc.)

- By End-user Segment

- Individuals / Households

- SMEs

- Large Corporates

List of Companies Covered in this Report:

- BPJS Kesehatan

- Prudential Indonesia

- Allianz Life Indonesia

- AIA Financial Indonesia

- AXA Mandiri Financial Services

- BRI Life

- Sun Life

- Sequis Life

- Manulife Indonesia

- Zurich Insurance Indonesia

- FWD Insurance Indonesia

- Sinar Mas MSIG Life

- Panin Dai-ichi Life

- Generali Indonesia

- Astra Aviva Life

- AdMedika (TPA)

- Lifepal (Insurtech)

- Halodoc Insurance

- Qoala

- PasarPolis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Near-universal JKN coverage expansion

- 4.2.2 Rising middle-class demand for private top-up plans

- 4.2.3 Double-digit medical-cost inflation boosting employer group cover

- 4.2.4 Stricter OJK conduct rules raising consumer confidence

- 4.2.5 Digital bank and e-wallet distribution unlocking micro-insurance

- 4.2.6 2025 government-funded annual check-ups creating new risk pools

- 4.3 Market Restraints

- 4.3.1 JKN funding deficits pressuring provider reimbursements

- 4.3.2 Accelerating medical inflation squeezing insurer margins

- 4.3.3 Data-localization and PDP law compliance costs

- 4.3.4 Low health-insurance literacy in rural provinces

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Insurance Product Type

- 5.1.1 Private Medical Insurance (PMI)

- 5.1.1.1 Individual Policy Coverage

- 5.1.1.2 Group Policy Coverage

- 5.1.2 Public / Social Security Schemes

- 5.1.1 Private Medical Insurance (PMI)

- 5.2 By Distribution Channel

- 5.2.1 Brokers / Agents

- 5.2.2 Banks (Bancassurance)

- 5.2.3 Direct-to-Consumer

- 5.2.4 Other Channels (Affinity, Associations, etc.)

- 5.3 By End-user Segment

- 5.3.1 Individuals / Households

- 5.3.2 SMEs

- 5.3.3 Large Corporates

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BPJS Kesehatan

- 6.4.2 Prudential Indonesia

- 6.4.3 Allianz Life Indonesia

- 6.4.4 AIA Financial Indonesia

- 6.4.5 AXA Mandiri Financial Services

- 6.4.6 BRI Life

- 6.4.7 Sun Life

- 6.4.8 Sequis Life

- 6.4.9 Manulife Indonesia

- 6.4.10 Zurich Insurance Indonesia

- 6.4.11 FWD Insurance Indonesia

- 6.4.12 Sinar Mas MSIG Life

- 6.4.13 Panin Dai-ichi Life

- 6.4.14 Generali Indonesia

- 6.4.15 Astra Aviva Life

- 6.4.16 AdMedika (TPA)

- 6.4.17 Lifepal (Insurtech)

- 6.4.18 Halodoc Insurance

- 6.4.19 Qoala

- 6.4.20 PasarPolis

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment