PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073499

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073499

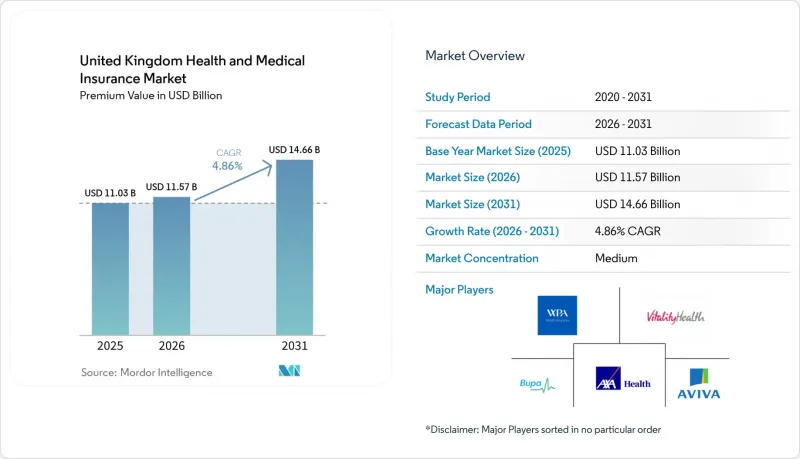

United Kingdom Health and Medical Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom health and medical insurance market size in terms of premium value is projected to expand from USD 11.03 billion in 2025 and USD 11.57 billion in 2026 to USD 14.66 billion by 2031, registering a CAGR of 4.86% between 2026 to 2031.

This report is Segmented by Policy Type (Individual, Group/Corporate), Coverage Type (In-Patient Only, Comprehensive, Health Cash Plans, and More), Distribution Channel (Brokers/IFAs, Direct-To-Consumer, and Others), End User (Individuals/Families, SMEs, Large Corporates), and Geography (England, Scotland, Wales, Northern Ireland). Market Forecasts are Provided in Value (USD).

United Kingdom Health and Medical Insurance Market Trends and Insights

Prolonged NHS Waiting Lists Fuelling Demand for Private Medical Insurance

NHS operational statistics show 7.39 million pathways awaiting treatment in April 2025, equivalent to an estimated 6.23 million individual patients, with only 59.7% of pathways treated within the 18-week constitutional standard, which remains well below the 92% target, keeping access constraints elevated in 2026. Pathways exceeding 52 weeks totaled 190,068, including 9,258 patients waiting over 65 weeks and 1,361 over 78 weeks, reinforcing the urgency households and employers feel about parallel private access solutions. Insurance-funded private hospital admissions reached 163,680 in Q2 2025, or 70% of total admissions, indicating that the United Kingdom health and medical insurance market is absorbing demand displaced by NHS wait times. Chemotherapy admissions rose 2% year over year in Q2 2025 to 18,540 treatments, a signal that oncology pathways are a specific pressure point driving insured utilization. Diagnostic waiting lists reached 1.7 million people in April 2025, with 21.2% waiting six weeks or more, which is pushing comprehensive policies that bundle imaging and endoscopy access to the forefront of product design in the United Kingdom health and medical insurance market.

Expansion of Employer-Sponsored Health Benefits Post-COVID-19

Employer-sponsored group policies covered 4.7 million people in 2023, the highest level in more than 30 years of ABI records, and the single largest driver of scale in the United Kingdom health and medical insurance market. Workplace claims rose 26% year over year to 1.3 million in 2023, with GBP 2.27 billion (USD 3.05 billion) paid, which underscores that employers are funding real use rather than offering symbolic benefits. Employers value reduced sickness absence, with ABI data suggesting prevention of 14 million lost working days annually, a productivity effect that supports continued premium budgets in 2026. Continuation of favorable tax treatment for salary sacrifice in the November 2025 Budget provides multi-year planning certainty for corporate benefits strategies and supports broader employee-funded participation, which widens the addressable base for the United Kingdom health and medical insurance market. As SMEs adopt streamlined group products through digital onboarding, distribution gains in the small employer segment complement large corporate renewals, sustaining a diverse demand pipeline in 2026.

Premium Inflation Outpacing Wage Growth

ONS Health Accounts show voluntary health insurance expenditure grew 2.4% in real terms in 2023, while real-terms claims costs rose 12.3%, implying insurers absorbed much of the medical inflation rather than fully repricing premiums in that period. ABI reported record claims payouts of GBP 3.57 billion (USD 4.80 billion) in 2023, up 21% from 2022, which increases the likelihood of premium rate corrections that can strain affordability for households and SMEs in 2026. Individual policyholders are most exposed because adverse selection concentrates risk: healthier members lapse, while older or sicker members retain coverage. Employers also face tougher renewal discussions if double-digit increases collide with budget limits, which can trigger design changes, higher excesses, or greater employee contributions. The United Kingdom health and medical insurance market therefore balances strong demand with price sensitivity, and affordability remains a near-term friction point in 2026.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Population & Chronic Disease Prevalence

- Rapid Uptake of Digital-First, App-Based Policy Administration

- Prospective NHS Reforms Dampening Perceived Need for PMI

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Group and corporate policies accounted for 67.56% of the 2025 share and covered 4.7 million people in 2023, giving this segment the largest enrollment base in the United Kingdom health and medical insurance market. Large employers with 250 or more staff treat private cover as a talent necessity in competitive sectors and as an anchor for renewal stability in 2026. Workplace claims reached 1.3 million in 2023 with GBP 2.27 billion (USD 3.05 billion) in payouts, a scale that reflects real utilization rather than latent take-up. Risk pooling across employee populations supports richer benefits at competitive unit costs relative to individually underwritten policies. The United Kingdom health and medical insurance market also benefits from multi-year corporate planning cycles, which smooth demand across economic conditions.

Individual policies held 32.44% of the 2025 share and are projected to be the fastest-growing policy type at a 6.48% CAGR through 2031, supported by digitally enabled sales and salary sacrifice awareness. The individual buyer mix spans self-employed professionals, retirees supplementing NHS access, and employees without group benefits who are willing to self-fund through tax-efficient mechanisms. Digital aggregators compress search and acquisition costs, thereby improving price transparency and conversion rates. As inflationary pressures ease for households, willingness to pay for faster diagnostics and consultant access is improving in 2026. These conditions expand the customer base for the United Kingdom health and medical insurance market as individual cover complements group growth.

Comprehensive inpatient and outpatient policies held 61.86% of the 2025 share and serve members seeking wide diagnostic access, consultant choice, mental health pathways, and surgical coverage, which sustains high revenue per member in the United Kingdom health and medical insurance market. The Private Healthcare Information Network recorded insurance-funded admissions at 163,680 in Q2 2025 and cited a 2% year-over-year increase in chemotherapy admissions to 18,540, a trend that underscores the need for robust oncology benefits. These policies also include enhanced imaging access and post-operative rehabilitation, which are valued amid NHS waiting times that persist in 2026. Providers and insurers align network strategies around location density and specialization to optimize member access. The United Kingdom health and medical insurance market continues to position comprehensive cover as the benchmark for full-service private pathways.

Health cash plans are projected to grow at a 7.03% CAGR through 2031, supported by FCA value measures showing 69% of premiums returned as claims in 2024 and by low monthly premiums in the GBP 10-30 (USD 13.45-40.36) range, which appeal to budget-conscious consumers. Claims journeys are simple and fast, which builds positive word of mouth and retention. Inpatient-only core policies priced at GBP 600-1,200 (USD 807.31-1,614.6) annually offer catastrophic protection at a lower cost for households prioritizing financial security. Dental and specialist covers address constrained NHS access, while standalone virtual GP subscriptions at GBP 5-15 (USD 6.72-20.18) per month offer low-commitment entry points. The United Kingdom health and medical insurance market size for health cash plans is projected to expand at a 7.03% CAGR between 2026 and 2031, reinforcing their role as on-ramps to broader protection.

Complete Report Scope:

- By Policy Type

- Individual Policies

- Group / Corporate Policies

- By Coverage Type

- In-patient Only (Core)

- Comprehensive (In- & Out-patient)

- Health Cash Plans

- Dental & Specialist Covers

- Other/Emerging (e.g., Virtual GP Access, Wellness Plans)

- By Distribution Channel

- Brokers & Independent Financial Advisers (IFAs)

- Direct-to-Consumer (Insurer)

- Bancassurance & Affinity Partnerships

- Online Aggregators / Insurtech Platforms

- By End User

- Individuals & Families

- Small & Medium Enterprises (SMEs)

- Large Corporates

- By Region (United Kingdom)

- England

- Scotland

- Wales

- Northern Ireland

List of Companies Covered in this Report:

- Bupa

- AXA Health

- Aviva

- VitalityHealth

- WPA

- Simplyhealth

- Benenden Health

- The Exeter

- Westfield Health

- Medicash

- Health Shield

- BHSF

- Sovereign Health Care

- General & Medical Healthcare

- Freedom Health Insurance

- Saga Health Insurance

- Equipsme

- CS Healthcare

- Allianz Care

- Aetna International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prolonged NHS waiting lists fuelling demand for private medical insurance (PMI)

- 4.2.2 Expansion of employer-sponsored health benefits post-COVID-19

- 4.2.3 Ageing population & chronic disease prevalence

- 4.2.4 Rapid uptake of digital-first, app-based policy administration

- 4.2.5 Salary-sacrifice PMI schemes unlocking tax advantages

- 4.2.6 Integration of virtual-GP networks as gatekeepers

- 4.3 Market Restraints

- 4.3.1 Premium inflation outpacing wage growth

- 4.3.2 Market consolidation reducing consumer choice

- 4.3.3 Prospective NHS reforms dampening perceived need for PMI

- 4.3.4 Data-privacy limits on wearable-driven underwriting models

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Policy Type

- 5.1.1 Individual Policies

- 5.1.2 Group / Corporate Policies

- 5.2 By Coverage Type

- 5.2.1 In-patient Only (Core)

- 5.2.2 Comprehensive (In- & Out-patient)

- 5.2.3 Health Cash Plans

- 5.2.4 Dental & Specialist Covers

- 5.2.5 Other/Emerging (e.g., Virtual GP Access, Wellness Plans)

- 5.3 By Distribution Channel

- 5.3.1 Brokers & Independent Financial Advisers (IFAs)

- 5.3.2 Direct-to-Consumer (Insurer)

- 5.3.3 Bancassurance & Affinity Partnerships

- 5.3.4 Online Aggregators / Insurtech Platforms

- 5.4 By End User

- 5.4.1 Individuals & Families

- 5.4.2 Small & Medium Enterprises (SMEs)

- 5.4.3 Large Corporates

- 5.5 By Region (United Kingdom)

- 5.5.1 England

- 5.5.2 Scotland

- 5.5.3 Wales

- 5.5.4 Northern Ireland

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Bupa

- 6.4.2 AXA Health

- 6.4.3 Aviva

- 6.4.4 VitalityHealth

- 6.4.5 WPA

- 6.4.6 Simplyhealth

- 6.4.7 Benenden Health

- 6.4.8 The Exeter

- 6.4.9 Westfield Health

- 6.4.10 Medicash

- 6.4.11 Health Shield

- 6.4.12 BHSF

- 6.4.13 Sovereign Health Care

- 6.4.14 General & Medical Healthcare

- 6.4.15 Freedom Health Insurance

- 6.4.16 Saga Health Insurance

- 6.4.17 Equipsme

- 6.4.18 CS Healthcare

- 6.4.19 Allianz Care

- 6.4.20 Aetna International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment