PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073537

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073537

Europe Insurance Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

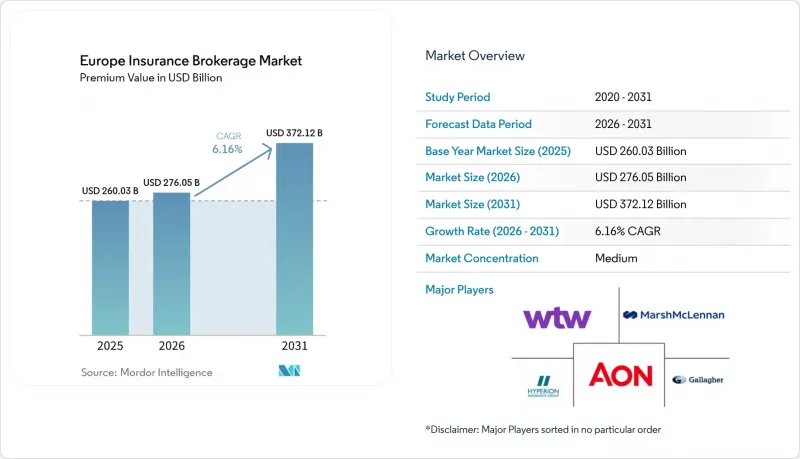

According to Mordor Intelligence, the europe insurance brokerage market size in terms of premium value is projected to expand from USD 260.03 billion in 2025 and USD 276.05 billion in 2026 to USD 372.12 billion by 2031, registering a CAGR of 6.16% between 2026 to 2031.

This report is Segmented by Brokerage Type (Retail Brokerage, Wholesale Brokerage, and More), Client Type (Individuals, Small & Medium-Sized Enterprises, and More), Insurance Line (Life, Health Insurance, and More), Distribution Channel (Traditional Face-To-Face, Digital/Online, and More), and Geography (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Insurance Brokerage Market Trends and Insights

Rising Demand for Cyber-Insurance Advisory

Organizations across Europe are upgrading risk-transfer strategies as ransomware incidents surge and legislative scrutiny intensifies under DORA, effective January 2025. Cyber premiums rose 35% during 2024, yet insurer capacity remains tight, prompting brokers to structure layered, parametric, and captive-fronted programs tailored to sector-specific exposures. SMEs, which remain 60% underinsured for digital risks, represent a fertile advisory pool that rewards firms capable of translating technical vulnerabilities into appropriate indemnities. Brokerages are recruiting chief information security officers and penetration-testing specialists to bridge knowledge gaps and secure underwriting data credibility. Standardized frameworks such as ISO 27001 and forthcoming NIS2 rules further expand consulting revenue because clients require proof of compliance alignment for policy issuance. Talent bottlenecks, however, inflate salary costs and prolong onboarding, marginally tempering the tailwind.

Increasing Regulatory Complexity

The 2025 Solvency II review tightens capital disclosure while the IDD elevates conduct-of-business obligations, compelling brokers to maintain granular product-suitability records that small carriers and SMEs often lack. These layers of oversight generate incremental advisory fees as intermediaries map risk appetite to carrier solvency positions and ensure multi-jurisdictional compliance. The United Kingdom's Consumer Duty framework solidifies this trend by mandating fair-value assessments and clear remuneration disclosure, reinforcing the value proposition of brokers with embedded compliance expertise. At the same time, duplicated reporting and audit procedures raise overheads that smaller firms struggle to absorb, accelerating acquisition interest from scale players looking to spread fixed costs. Brokers capitalize on regulatory arbitrage by structuring cross-border programs that exploit variance in premium taxes and capital-relief rules, yet emerging pan-EU alignment under DORA may gradually narrow such opportunities.

Fee Compression From Online Comparison Platforms

Price-aggregator websites have eroded commission rates for personal lines and commoditized segments by offering real-time premium grids that enable straight-through purchasing. Insurers aiming for sub-15% expense ratios channel more volume directly to digital-first distributors, cutting traditional intermediaries out of the value chain. Transparency rules under IDD and Consumer Duty reinforce client bargaining power by obliging brokers to disclose remuneration and demonstrate fair value. As a result, negotiated base commissions for standard motor and home policies in some EU markets fell by as much as 150 basis points during 2024. Premium-rich advisory segments like cyber and trade credit offer insulation, yet cross-subsidization becomes harder as profit pools shrink on commoditized lines. Brokers counter by differentiating through value-added services, risk engineering, claims advocacy, and data analytics, though scaling these services across diverse micro-segments remains challenging.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of the SME Sector

- Insurtech Partnerships Enhancing Customer Experience

- Talent Shortage in Specialty-Risk Advisory

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Retail brokerage generated 56.40% of the European insurance brokerage market size in 2025 on the back of deep client relationships and multichannel servicing capabilities. Nevertheless, reinsurance brokerage is predicted to expand at a 5.05% CAGR through 2031, energizing overall growth as climate-driven catastrophe severity prompts cedents to seek sophisticated capital-management solutions. Reinsurance specialists monetize advanced stochastic-modeling and alternative-risk-transfer advisory, often commanding higher fee yields than retail placements. Wholesale brokers remain pivotal for surplus-line cover and multi-territory programs, especially where local capacity constraints intersect with complex compliance requirements. Bancassurance brokerage, though smaller in absolute terms, is regaining momentum as banks leverage payment and balance-sheet data to upsell bundled coverage and increase non-interest income.

Reinsurance brokerage is accelerating, with growth projected to rise from 3.8% (2019-2024) to 5.05%, driven by increased catastrophe-bond issuance, parametric solutions, and greater demand for carrier capital relief. Meanwhile, retail insurance margins are under pressure as digital aggregators compress commission spreads on standard products, prompting a shift toward advisory-heavy specialties. Wholesale intermediaries are gaining from the globalization of supply chains, which require cross-border certificate issuance and localized claims support. However, broader macroeconomic headwinds may dampen premium growth across markets. Bancassurance is set to expand as open-banking regulations boost data availability, allowing insurers to embed personalized offers within everyday financial transactions.

Small and medium-sized enterprises currently represent 46.10% of the European insurance brokerage market share and are projected to clock a 6.03% CAGR over the forecast horizon. Geopolitical disruptions and cybercrime spikes have heightened risk awareness, catapulting demand for business-interruption, trade-credit, and cyber-liability policies. Brokers that introduce modular policy architectures and digital self-serve platforms shorten onboarding, an advantage when courting cost-sensitive micro-enterprises. Large corporations sustain resilient premium pools but exert fee pressure by internalizing elements of risk management and running competitive tenders among mega-brokers. Public-sector entities rely on brokers for climate-resilience funding structures and catastrophe-response frameworks, bolstering demand for alternative-risk-transfer counsel.

The SME segment is growing rapidly, boosted by EU recovery-fund investments that support digitization grants and expose businesses to new cyber risks requiring coverage. Start-ups within platform ecosystems are driving demand for innovative policies, including contingent-labor liability and intellectual property protection. At the individual level, more customers are turning to direct-to-consumer channels for motor and home insurance, squeezing broker margins in the small-account space. As a result, brokerages are refocusing on advisory-rich services tied to professional indemnity, key-person coverage, and voluntary benefits. These offerings are increasingly aligned with the needs of entrepreneurial clients and their evolving risk profiles.

Complete Report Scope:

- By Brokerage Type

- Retail Brokerage

- Wholesale Brokerage

- Reinsurance Brokerage

- Bancassurance Brokerage Services

- By Client Type

- Individuals

- Small & Medium-Sized Enterprises (SMEs)

- Large Corporations

- Public Sector Entities

- By Insurance Line

- Life Insurance

- Health Insurance

- Property & Casualty (Motor, Home, Commercial, Liability)

- Specialty Lines (Cyber, Pet, Marine, Travel)

- By Distribution Channel

- Traditional Face-to-Face

- Digital / Online Platforms

- Affinity & Embedded Partnerships

- Bancassurance Partnerships

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

List of Companies Covered in this Report:

- Marsh & McLennan Companies (Marsh)

- Aon plc

- Willis Towers Watson (WTW)

- Arthur J. Gallagher & Co.

- Hyperion Insurance Group (Howden)

- BGL Group

- Soderberg & Partners

- Acrisure

- Lockton Companies

- PIB Group

- Siaci Saint Honore

- GrECo Group

- Henner Group

- AJB Group

- Ecclesiastical Insurance Broker Services

- Jensten Group

- Eurorisk (Renomia)

- Miller Insurance Services

- Funk Gruppe

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for cyber insurance advisory

- 4.2.2 Increasing regulatory complexity (IDD, Solvency II)

- 4.2.3 Expansion of SME sector seeking tailored cover

- 4.2.4 Insurtech partnerships enhancing customer experience

- 4.2.5 Embedded-insurance distribution in EU digital marketplaces

- 4.2.6 EU Green Deal driving climate-risk & parametric products

- 4.3 Market Restraints

- 4.3.1 Fee compression from online comparison platforms

- 4.3.2 GDPR limits on data-driven cross-selling

- 4.3.3 Insurer consolidation reduces broker bargaining power

- 4.3.4 Talent shortage in specialty-risk advisory

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, 2020-2030)

- 5.1 By Brokerage Type

- 5.1.1 Retail Brokerage

- 5.1.2 Wholesale Brokerage

- 5.1.3 Reinsurance Brokerage

- 5.1.4 Bancassurance Brokerage Services

- 5.2 By Client Type

- 5.2.1 Individuals

- 5.2.2 Small & Medium-Sized Enterprises (SMEs)

- 5.2.3 Large Corporations

- 5.2.4 Public Sector Entities

- 5.3 By Insurance Line

- 5.3.1 Life Insurance

- 5.3.2 Health Insurance

- 5.3.3 Property & Casualty (Motor, Home, Commercial, Liability)

- 5.3.4 Specialty Lines (Cyber, Pet, Marine, Travel)

- 5.4 By Distribution Channel

- 5.4.1 Traditional Face-to-Face

- 5.4.2 Digital / Online Platforms

- 5.4.3 Affinity & Embedded Partnerships

- 5.4.4 Bancassurance Partnerships

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Marsh & McLennan Companies (Marsh)

- 6.4.2 Aon plc

- 6.4.3 Willis Towers Watson (WTW)

- 6.4.4 Arthur J. Gallagher & Co.

- 6.4.5 Hyperion Insurance Group (Howden)

- 6.4.6 BGL Group

- 6.4.7 Soderberg & Partners

- 6.4.8 Acrisure

- 6.4.9 Lockton Companies

- 6.4.10 PIB Group

- 6.4.11 Siaci Saint Honore

- 6.4.12 GrECo Group

- 6.4.13 Henner Group

- 6.4.14 AJB Group

- 6.4.15 Ecclesiastical Insurance Broker Services

- 6.4.16 Jensten Group

- 6.4.17 Eurorisk (Renomia)

- 6.4.18 Miller Insurance Services

- 6.4.19 Funk Gruppe

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment