PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073644

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073644

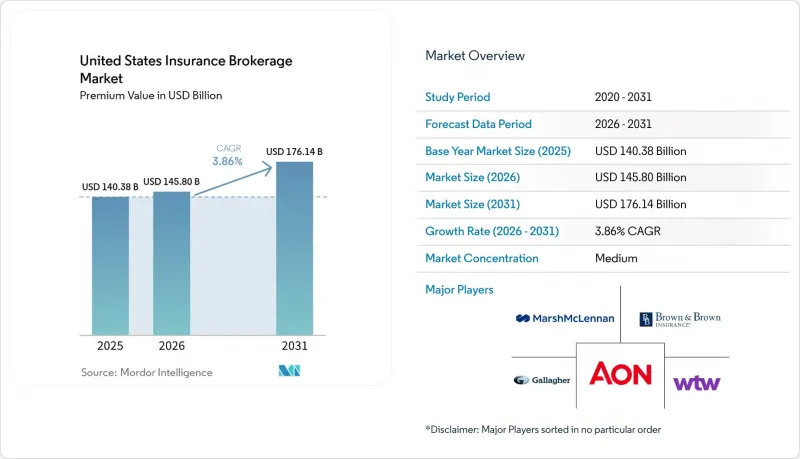

United States Insurance Brokerage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states insurance brokerage market size in terms of premium value is projected to expand from USD 140.38 billion in 2025 and USD 145.80 billion in 2026 to USD 176.14 billion by 2031, registering a CAGR of 3.86% between 2026 to 2031.

This report is Segmented by Brokerage Type (Retail Brokerage, Wholesale Brokerage, and More), Client Type (Individuals, Small & Medium-Sized Enterprises, and More), Insurance Line (Life, Health, and More), Distribution Channel (Traditional Face-To-Face, Digital/Online Platforms, and More), and Geography (Northeast, Midwest, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Insurance Brokerage Market Trends and Insights

Data-Driven Pricing & Risk-Selection Models Transform Underwriting

Predictive analytics and artificial intelligence tools now allow brokerages to slice historical loss data, external data sets, and carrier appetite information into precise pricing recommendations that lower loss ratios by 15-20% for leading firms. Brokers that control proprietary data assets embed those insights directly into negotiations, turning formerly relationship-centric exchanges into evidence-based conversations with underwriters. As a result, mid-sized agencies increasingly subscribe to third-party analytics vendors to remain viable, while the largest houses expand internal data science teams. State insurance regulators, via NAIC model rules, demand transparency on algorithmic fairness and governance, adding compliance layers that smaller agencies must budget for. The United States insurance brokerage market, therefore, rewards investment in explainable AI that balances predictive power with regulator trust. Insurers likewise benefit from richer submissions, creating a positive-feedback loop that reinforces data-led broker value.

Cyber-Attack Surge Drives Specialty Coverage Expansion

Ransomware events reported to the FBI jumped 41% year-on-year in 2024, with median extortion payments hitting USD 2.73 million, spurring a surge in cyber-liability demand. The United States insurance brokerage market channels this urgency into a 5.92% specialty-lines CAGR, dwarfing growth rates in traditional P&C. Brokerages establish dedicated cyber practices staffed by forensic analysts and incident-response veterans who can calibrate limit structures, retention levels, and war-exclusion carve-outs. Higher technical complexity means clients value counsel, enabling brokers to command 25-30% higher commission rates than standard commercial placements. Rapidly shifting ransomware variants also shorten policy cycles, giving brokers more frequent touchpoints that translate into sticky advisory relationships. As federal privacy regulations tighten, mid-market enterprises increasingly seek help navigating breach-notification rules, further bolstering broker relevance. Competitive differentiation hinges on access to proprietary incident data and partnerships with cybersecurity vendors, reinforcing first-mover advantages.

Talent Shortage Drives Compensation Inflation Across Producer Ranks

Roughly 400,000 insurance professionals are slated to retire by 2026, while new-hire pipelines trail replacement demand by 25%. As competition intensifies for licensed talent, commercial-lines producers in coastal metros now command 8-12% annual pay bumps plus signing bonuses that can exceed USD 100,000. The United States insurance brokerage market passes a portion of those incremental costs on to clients through higher service fees, yet margin compression persists, especially for small agencies. Elevated payroll outlays also divert capital away from technology upgrades, creating a vicious cycle where resource-constrained brokers risk falling further behind digital leaders. State continuing-education mandates add time and expense that favor organizations with in-house training academies. Talent scarcity is most acute in cyber, employee-benefits, and catastrophe-modeling disciplines, where brokers require deep technical fluency to advise clients credibly. Intensified poaching among large firms drives up non-compete litigation, inflating legal budgets.

Other drivers and restraints analyzed in the detailed report include:

- Property & Casualty Rate Hardening Sustains Commission Growth

- Fiduciary Transparency Rules Reshape Compensation Models

- Direct-to-Consumer Digital Platforms Compress Traditional Broker Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Retail houses captured 60.55% of the United States insurance brokerage market share in 2025 by serving vast consumer and mid-market accounts, but reinsurance specialists are projected to log a 5.02% CAGR through 2031 as catastrophe exposure drives treaty-renegotiation volume. Retail leaders integrate analytics, digital self-service, and bundled advisory to defend margins in a commoditizing arena. Simultaneously, wholesale intermediaries channel surplus-lines placements for risks that standard carriers reject, sustaining steady growth despite tighter economic cycles. The reinsurance niche leverages demand for alternative capital, insurance-linked securities, and parametric retrocession layers that respond to climate volatility. Bancassurance brokerage, though the smallest, benefits from deregulation that lets banks cross-sell property-casualty and life solutions within wealth-management branches. The United States insurance brokerage market size for reinsurance is expected to widen as cedents confront rising frequency-severity curves and seek modeling sophistication unavailable in-house. Brokers supplement placements with advisory on retention structures, capital relief, and portfolio diversification.

The competitive tableau favors firms that pair traditional market access with predictive modeling and multi-capital structuring expertise. Global brokers deploy proprietary catastrophe models and sidecar funds to absorb peak-zone exposures, offering insurers capital-relief pathways previously limited to reinsurance giants. Smaller specialists carve niches in facultative placements, targeting high-margin industrial risks. Retail brokers, meanwhile, pilot embedded-insurance APIs to halt share erosion from direct channels. Each sub-segment vies for talent, yet divergent skill sets, retail account management versus quantitative cat modeling limitt cross-over hiring efficiency. Regulatory oversight tightens around reinsurance collateralization, compelling brokers to vet counterparties rigorously. The segment's success ultimately hinges on balancing speed of placement with depth of analytical justification that satisfies both clients and rating agencies.

Small and medium-sized enterprises delivered 42.35% of the United States insurance brokerage market revenue in 2025, reflecting vibrant post-pandemic entrepreneurship, while individual clients will expand fastest at a 6.7% CAGR to 2031. Millennial wealth accumulation, amplified by digital-advice channels, unlocks appetite for life, disability, and cyber-identity covers once reserved for high-net-worth segments. Brokers deploy robo-onboarding, decision-tree underwriting, and policy-comparison dashboards to serve these cost-conscious yet tech-literate buyers profitably. Large corporates maintain outsized premium spend, but in-house risk managers and captive vehicles dampen organic brokerage growth, pushing brokers toward analytics-centric service retainer models. Public-sector entities continue to require complex insurance programs for critical infrastructure, cyber, and climate resilience, although budget cycles can be protracted. Across client classes, fiduciary transparency and ESG reporting elevate broker roles from transactional procurement to strategic counsel. The United States insurance brokerage market responds by segmenting service teams: mass-affluent digital units, SME hybrid desks, and enterprise consultative pods.

Behavioral segmentation exceeds traditional size-band classification. For individuals, life-event triggers such as home purchase or baby arrival sync with embedded-offer prompts, creating micro-decision windows for brokers. SME owners gravitate toward bundled multiline policies that simplify administration; brokers package P&C, employee benefits, and cyber under unified dashboards. Large corporates demand benchmark reports against peer cohorts, fueling demand for data warehousing and analytics overlays that track claims frequency and severity. Public-sector risk pools encourage brokers to coordinate mutual-aid frameworks and parametric triggers tied to municipal budgets. Cross-selling remains the revenue engine: a broker that secures an SME's general liability policy often wins subsequent benefits and key-person life placements. Within the United States insurance brokerage market, segmentation mastery yields superior client-lifetime value and cushions margin erosion elsewhere.

Complete Report Scope:

- By Brokerage Type

- Retail Brokerage

- Wholesale Brokerage

- Reinsurance Brokerage

- Bancassurance Brokerage Services

- By Client Type

- Individuals

- Small & Medium-Sized Enterprises (SMEs)

- Large Corporations

- Public Sector Entities

- By Insurance Line

- Life Insurance

- Health Insurance

- Property & Casualty (Motor, Home, Commercial, Liability)

- Specialty Lines (Cyber, Pet, Marine, Travel)

- By Distribution Channel

- Traditional Face-to-Face

- Digital / Online Platforms

- Affinity & Embedded Partnerships

- Bancassurance Partnerships

- By Geography

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- Marsh McLennan (Marsh)

- Aon plc

- Willis Towers Watson (WTW)

- Arthur J. Gallagher & Co.

- Brown & Brown Inc.

- HUB International

- Lockton Companies

- USI Insurance Services

- Truist Insurance Holdings

- Acrisure

- Alliant Insurance Services

- Hilb Group

- Ryan Specialty Group

- NFP Corp.

- BXS Insurance

- PCF Insurance Services

- AssuredPartners

- Amwins Group

- INSURICA

- Risk Strategies Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-driven pricing & risk-selection models

- 4.2.2 Increasing cyber-attack frequency boosting specialty demand

- 4.2.3 Hardening P&C rates sustaining brokerage commissions

- 4.2.4 Regulatory tailwinds for fiduciary transparency

- 4.2.5 Embedded-insurance partnerships with fintech & e-commerce

- 4.2.6 Growing demand for parametric & climate-risk covers

- 4.3 Market Restraints

- 4.3.1 Talent shortage & escalating producer compensation costs

- 4.3.2 Margin pressure from direct-to-consumer digital carriers

- 4.3.3 Increased carrier consolidation reducing brokerage panels

- 4.3.4 Rising E&O litigation risk on advisory failures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Brokerage Type

- 5.1.1 Retail Brokerage

- 5.1.2 Wholesale Brokerage

- 5.1.3 Reinsurance Brokerage

- 5.1.4 Bancassurance Brokerage Services

- 5.2 By Client Type

- 5.2.1 Individuals

- 5.2.2 Small & Medium-Sized Enterprises (SMEs)

- 5.2.3 Large Corporations

- 5.2.4 Public Sector Entities

- 5.3 By Insurance Line

- 5.3.1 Life Insurance

- 5.3.2 Health Insurance

- 5.3.3 Property & Casualty (Motor, Home, Commercial, Liability)

- 5.3.4 Specialty Lines (Cyber, Pet, Marine, Travel)

- 5.4 By Distribution Channel

- 5.4.1 Traditional Face-to-Face

- 5.4.2 Digital / Online Platforms

- 5.4.3 Affinity & Embedded Partnerships

- 5.4.4 Bancassurance Partnerships

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Marsh McLennan (Marsh)

- 6.4.2 Aon plc

- 6.4.3 Willis Towers Watson (WTW)

- 6.4.4 Arthur J. Gallagher & Co.

- 6.4.5 Brown & Brown Inc.

- 6.4.6 HUB International

- 6.4.7 Lockton Companies

- 6.4.8 USI Insurance Services

- 6.4.9 Truist Insurance Holdings

- 6.4.10 Acrisure

- 6.4.11 Alliant Insurance Services

- 6.4.12 Hilb Group

- 6.4.13 Ryan Specialty Group

- 6.4.14 NFP Corp.

- 6.4.15 BXS Insurance

- 6.4.16 PCF Insurance Services

- 6.4.17 AssuredPartners

- 6.4.18 Amwins Group

- 6.4.19 INSURICA

- 6.4.20 Risk Strategies Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment