PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073546

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073546

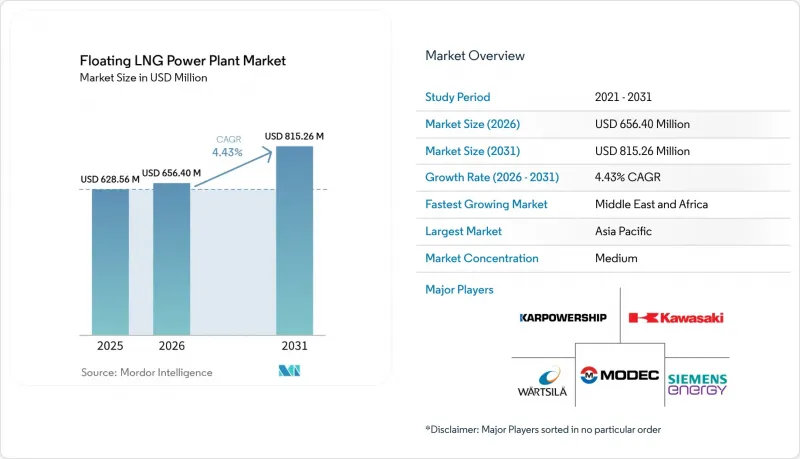

Floating LNG Power Plant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the floating LNG power vessel market is expected to grow from USD 628.56 million in 2025 to USD 656.40 million in the same year and is projected to reach USD 815.26 million by 2031, registering a CAGR of 4.43% during the forecast period of 2025-2031.

This report is Segmented by Type (Power Barge, Power Ship), Power Capacity (<= 50 MW and More), Application (Peak Power Supply, Base-Load Supply, Emergency/Disaster Relief), End-User (Utilities & IPPs, Industrial, Commercial & Data-Centres), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Floating LNG Power Plant Market Trends and Insights

LNG Price Advantage Over Diesel Remains the Sharpest Commercial Driver

The floating LNG power vessel market continues to rely on a strong fuel-cost advantage, as evidenced in 2026 when UHERO reported delivered LNG prices at USD 17.9 per MMBtu compared to LSFO at USD 22.2 per MMBtu under Brent-linked conditions. A similar cost dynamic was observed in Indonesia, where peer-reviewed research published in April 2025 indicated natural gas delivered to island plants at USD 10.4-11.3 per MMBtu, significantly lower than high-speed diesel at USD 25.5 per MMBtu, maintaining a 55-60% cost advantage for natural gas. This price differential is driving project activity in the floating LNG power vessel market. For instance, PLN EPI announced a USD 1.5 billion small-scale LNG program in March 2025, targeting 41 island plants with a combined capacity of 2,148 MW and aiming for annual diesel savings of USD 300 million.

Integrated floating storage, regasification, and power vessels offer an additional cost advantage over separated assets. Research by Rahmanta and co-authors highlighted that hub-and-spoke supply-chain costs can account for 30-40% of the delivered gas price when FSRU and generation assets are procured separately. This underscores the benefits of a bundled vessel solution, which eliminates an intermediate cost node in the LNG-to-power supply chain. Consequently, the floating LNG power vessel market benefits not only from lower fuel costs but also from a streamlined delivery model. Procurement strategies that separate regasification and generation in tenders risk undervaluing the commercial benefits of an integrated solution, favoring operators capable of delivering fuel intake, storage, regasification, and power generation through a single platform.

IMO CII And EEXI Are Accelerating Fleet Transition Toward Gas-Fired Vessels

The floating LNG power vessel market is influenced by regulatory developments and fuel economics. The April 2025 IMO MEPC 83 outcome introduced a two-tier GHG fuel-intensity framework, requiring reductions of 4-17% by 2028 and 30-43% by 2035 compared to 2008 baselines. Within this framework, LNG vessels equipped with high-pressure diesel-cycle engines, which have a methane slip near 0.2%, are commercially better positioned than Otto medium-speed alternatives with significantly higher slip rates. This has already impacted vessel specifications in the market. For instance, Wartsila announced in January 2026 that its NextDF technology can reduce methane slip in four-stroke dual-fuel engines to below 1%, aligning newer designs more closely with compliance requirements.

Cost pressures are particularly pronounced in Europe, where the EU ETS expanded its scope to include methane and nitrous oxide starting in 2026. Operators calling at EU ports must surrender allowances for 70% of their 2025 vessel emissions in 2026. This regulatory shift is creating a divide within the floating LNG power vessel market. Newer fleets capable of maintaining charter economics are better positioned, while older Otto-cycle assets face significant retrofit or retirement decisions by the end of the decade. Vessel owners who invest early in methane-abatement measures can safeguard rechartering opportunities during the 2026-2031 period. Conversely, those who delay such investments are likely to encounter reduced vessel valuations and diminished pricing power.

Charter Rate Volatility Creates Financing Risk Across The Value Chain

The floating LNG power vessel market experiences financing challenges when charter pricing fluctuates significantly, as vessel economics, fuel pass-through terms, and tariff recovery are closely tied to the rate cycle at the time of contract signing. FSRU charter rates, which averaged USD 80,000-120,000 per day before 2022, surged to USD 180,000-200,000 per day following the European energy crisis and stabilized at approximately USD 130,000-150,000 per day for converted vessels by mid-2024, according to the analysis referenced in the draft. A key issue for the market is the difficulty in structuring long-term Power Purchase Agreements (PPAs) in a declining LNG and charter market. Pass-through clauses transfer volatility to off-takers, while fixed-price structures reduce operator margins. For instance, the draft highlights Brazil, where charter contracts for eight FSRUs were estimated at nearly USD 1 million per day, amounting to USD 1.5 billion over four years, with costs passed through regulated tariffs. Operators who secured charters during the 2022-2023 peak now face disadvantages in rebidding, competing against lower-cost vessels in a softer market. While this does not eliminate demand for floating LNG power vessels, it increases challenges related to financing, refinancing, and tariff approvals throughout the value chain.

Other drivers and restraints analyzed in the detailed report include:

- African Gas-To-Power Tenders Are a Structural Demand Catalyst

- AI-Driven Load-Balancing Software Is Redefining Barge Operational Economics

- Methane-Slip Regulation Is Narrowing The Operational Life Of Older Dual-Fuel Fleets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Power barges accounted for 59.6% of the floating LNG power vessel market share in 2025, while power ships are projected to grow at a compound annual growth rate (CAGR) of 5.1% through 2031. The dominance of power barges is attributed to their simpler structural design, which reduces hull costs and provides additional deck space for turbines, heat recovery systems, and control equipment. This design advantage typically lowers total capital expenditure (CAPEX) by 15-20% compared to similar power ships, making barges a cost-effective option in price-sensitive tenders. In the floating LNG power vessel market, the lower construction costs of barges align well with base-load contracts where mobility is less critical, and installation efficiency and stable output are prioritized.

Power ships are gaining market share more rapidly due to their self-propulsion capabilities, which enable redeployment within weeks of a contract award. This feature is particularly advantageous in emergency tenders and short-notice capacity auctions. For instance, ST Engineering's October 2025 contract for Estrella del Mar IV, a 145 MW floating combined-cycle plant equipped with onboard lithium-ion battery storage, highlights the increasing integration of mobility with hybrid dispatch capabilities. This flexibility allows vessels to transition between base-load and peak support roles, expanding revenue opportunities while maintaining their core gas-to-power function within the floating LNG power vessel market. While power barges are expected to remain the dominant format over the forecast period, power ships are poised to gain traction in scenarios where governments prioritize rapid response times, contract flexibility, and the ability to relocate capacity across borders with minimal civil infrastructure requirements.

The 51-200 MW range represented 49.3% of the floating LNG power vessel market size in 2025, highlighting its suitability for island grids, remote industrial loads, and smaller urban systems. At this capacity, combined-cycle gas turbine configurations become feasible on floating platforms, achieving net efficiency levels of 50-55%, compared to 35-42% for simple-cycle open-frame systems. This range offers a balance between manageable vessel size and improved fuel efficiency, making it a key segment for applications requiring steady output without the capacity to accommodate large single-vessel installations.

The >= 401 MW category is projected to be the fastest-growing segment, with a compound annual growth rate (CAGR) of 5.9% through 2031. This growth is driven by utilities prioritizing single-vessel solutions to minimize coordination risks associated with multiple units. This trend is particularly evident in South Asia and Africa, where large-scale utility procurement increasingly favors larger floating plants over modular additions. By May 2026, Karpowership's fleet had surpassed 8,500 MW across 45 vessels, demonstrating the commercial viability of large-scale deployments. Meanwhile, the <= 50 MW range remains significant for emergency backup and small-island applications, while the 201-400 MW range continues to serve mining operations, offshore oil-field supply, and remote industrial power needs, where mid-sized vessels are advantageous due to fuel logistics and grid absorption considerations.

Complete Report Scope:

- By Type

- Power Barge

- Power Ship

- By Power Capacity

- less than 50 MW

- 51 - 200 MW

- 201 - 400 MW

- more than 401 MW

- By Application

- Peak Power Supply

- Base-Load Supply

- Emergency / Disaster Relief

- By End-user

- Utilities & IPPs

- Industrial (Mining, O&G, Desalination)

- Commercial & Data-Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific accounted for 36.1% of the floating LNG power vessel market share in 2025, making it the largest regional base for current demand. The region benefits from a combination of island electrification needs, dense coastal load centers, and a mature LNG supply chain across countries such as Indonesia, Malaysia, Japan, and South Korea. Indonesia remains a key market, with PLN EPI launching a USD 1.5 billion small-scale LNG program in March 2025 to support 41 island plants. A peer-reviewed analysis highlighted that integrated FSRPP structures reduce costs by eliminating a supply-chain link that can account for 30-40% of the delivered gas price when assets are separated. Additionally, the region is expanding beyond established markets, as evidenced by the Haiphong FSRU project in Vietnam and JERA's proposed Hawaii FSRU-linked program, demonstrating that Asia-Pacific expertise is being exported to adjacent island-power corridors.

The Middle East and Africa are projected to grow at a 4.6% CAGR through 2031, making it the fastest-expanding region in the floating LNG power vessel market. This growth is supported by the African Energy Chamber's projection that natural gas demand across Africa will increase by 60% by 2050. Senegal's Dakar project exemplifies this trend with a 335 MW integrated LNG-to-power system capable of meeting up to 25% of national demand without requiring onshore gas infrastructure. Egypt is further solidifying its role as a floating gas hub, with Hoegh Evi's 10-year charter for the Hoegh Gandria expected to add up to 1,000 mmscfd of peak regasification capacity at Port of Sumed starting in Q4 2026. Similarly, Jordan's decision in May 2026 to lease a new FSRU for Aqaba underscores the growing reliance on floating regasification as a standard component of grid gas supply security in the region.

While Europe and the Americas currently represent smaller markets in terms of scale, they remain strategically significant for the floating LNG power vessel market. These regions combine reserve-power needs, gas-security concerns, and selective large-capacity procurement. In Brazil, the 2026 reserve capacity auction contracted nearly 8.5 GW of LNG-fired thermal capacity, attracting an estimated BRL 48 billion (USD 9.6 billion) in investment to support new or expanded FSRU infrastructure across multiple states. In the Americas, Mexico's Yucatan deployment and JERA's Hawaii proposal highlight opportunities in both frontier and regulated systems where dispatchable power is required before onshore infrastructure becomes operational. In Europe, supply security remains a priority, with Congo LNG output reaching 3 million tonnes per year in early 2026, providing an additional floating supply source for utilities aiming to reduce reliance on Russian gas.

- Bumi Armada Berhad

- CMHI Haimen

- Damen Shipyards Group

- GE Vernova Inc.

- Golar Power

- Hanwha Ocean Co., Ltd.

- Karpowership

- Kawasaki Heavy Industries, Ltd.

- Seatrium Limited

- MAN Energy Solutions

- Mitsubishi Heavy Industries, Ltd.

- MODEC, Inc.

- Power Barge Corporation

- Samsung Heavy Industries Co., Ltd.

- Siemens Energy AG

- Tri-Yard Power Solutions

- TSUNEISHI Shipbuilding

- VARD

- Wartsila Oyj Abp

- Shanghai Zhenhua Heavy Industries Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream LNG-price advantage vs. diesel in island grids

- 4.2.2 IMO CII & EEXI pushing gas-fired marine assets

- 4.2.3 African gas-to-power tenders favour redeployable vessels

- 4.2.4 AI-driven load-balancing software unlocks hybrid barges

- 4.2.5 Ageing steam-turbine LNG carriers ripe for power-plant conversion

- 4.2.6 Modular cryogenic BOP packages cut barge CAPEX 25 %

- 4.3 Market Restraints

- 4.3.1 LNG shipping over-capacity keeps charter rates volatile

- 4.3.2 High methane-slip regulations threaten dual-fuel engines

- 4.3.3 Insurance premiums for cyclone-prone moorings

- 4.3.4 Limited berth availability at congested coal terminals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Power Barge

- 5.1.2 Power Ship

- 5.2 By Power Capacity

- 5.2.1 less than 50 MW

- 5.2.2 51 - 200 MW

- 5.2.3 201 - 400 MW

- 5.2.4 more than 401 MW

- 5.3 By Application

- 5.3.1 Peak Power Supply

- 5.3.2 Base-Load Supply

- 5.3.3 Emergency / Disaster Relief

- 5.4 By End-user

- 5.4.1 Utilities & IPPs

- 5.4.2 Industrial (Mining, O&G, Desalination)

- 5.4.3 Commercial & Data-Centres

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Nordic Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Malaysia

- 5.5.3.6 Thailand

- 5.5.3.7 Indonesia

- 5.5.3.8 Vietnam

- 5.5.3.9 Australia

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Bumi Armada Berhad

- 6.4.2 CMHI Haimen

- 6.4.3 Damen Shipyards Group

- 6.4.4 GE Vernova Inc.

- 6.4.5 Golar Power

- 6.4.6 Hanwha Ocean Co., Ltd.

- 6.4.7 Karpowership

- 6.4.8 Kawasaki Heavy Industries, Ltd.

- 6.4.9 Seatrium Limited

- 6.4.10 MAN Energy Solutions

- 6.4.11 Mitsubishi Heavy Industries, Ltd.

- 6.4.12 MODEC, Inc.

- 6.4.13 Power Barge Corporation

- 6.4.14 Samsung Heavy Industries Co., Ltd.

- 6.4.15 Siemens Energy AG

- 6.4.16 Tri-Yard Power Solutions

- 6.4.17 TSUNEISHI Shipbuilding

- 6.4.18 VARD

- 6.4.19 Wartsila Oyj Abp

- 6.4.20 Shanghai Zhenhua Heavy Industries Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment