PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073620

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073620

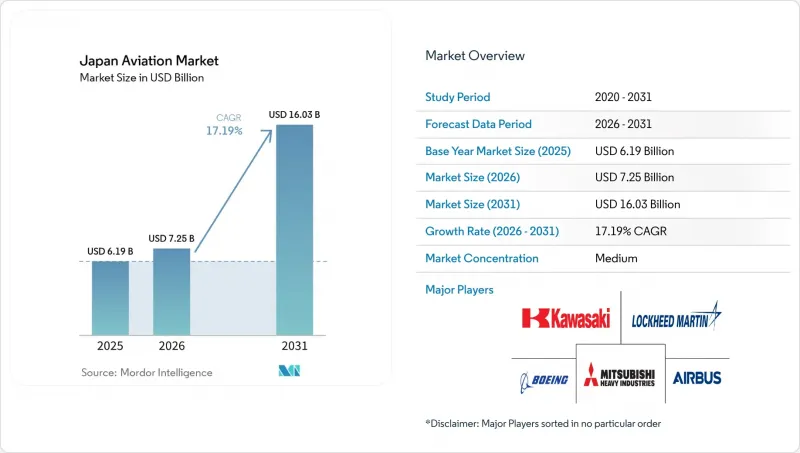

Japan Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, japan aviation market size in 2026 is estimated at USD 7.25 billion, growing from 2025 value of USD 6.19 billion with 2031 projections showing USD 16.03 billion, growing at 17.19% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Commercial Aviation, General Aviation, and Military Aviation), Propulsion Technology (Turboprop, Turbofan, Piston Engine, Turboshaft, and Others), and End User (Civil and Commercial Operators, Government and Defense Agencies, and Business and General Aviation Owners). The Market Forecasts are Provided in Terms of Value (USD).

Japan Aviation Market Trends and Insights

Surge in Inbound Tourism Post Pandemic

Japan aims to attract 60 million overseas visitors by 2030, a goal already supported by double-digit monthly arrivals in 2025. ANA Holdings reinforced the premium segment by taking a stake in XPERISUS, a curator of bespoke travel experiences, to capture higher revenue per passenger. Airlines are responding with widebody retrofits that expand premium-cabin density while retaining economy-class seat counts, balancing yield and volume. Regional airports, from Kyushu to Hokkaido, now host more direct international services as tourists seek heritage and culinary experiences beyond the Tokyo-Osaka axis. These dispersed flows encourage operators of 70- to 150-seat aircraft and helicopter tour providers to broaden route maps, stimulating auxiliary segments such as ground handling and hospitality training. The tourism-linked uplift remains front-loaded, with pronounced gains expected through 2027, before growth normalizes to structural demand tied to cultural, business events, and remote work travel.

Record Defense Budget Boosting Fighter and Rotorcraft Procurement

In FY 2025 Japan's Defense budget topped USD 52 billion, directing new funds to the Global Combat Air Programme (GCAP) it is co-developing with the United Kingdom and Italy. The project transfers stealth-airframe and mission-system design authority to Japanese primes, elevating domestic aerospace know-how ahead of prototype rollout in 2026. Complementary investments in multi-mission helicopters protect maritime assets and strengthen disaster-response readiness. A parallel workforce plan removed minimum height limits for pilot applicants, broadening the talent pipeline and integrating gender-diverse cadets across all service branches. Rising procurement outlays cascade through suppliers of carbon-fiber composites, infrared sensors, and electronic warfare suites, cementing Japan's status as a regional defense and aviation hub with growing export potential.

Pilot Shortage Driven by Aging Workforce and Training Limitations

The average pilot age at full-service carriers surpassed 49 years in 2025, straining roster planning during peak traffic periods. The SKYCAMP initiative, a collaboration between Kagoshima University, JAL, and Japan Airlines, has produced its first cadets, who will enter line service in 2026, providing a template for regional talent pipelines. JAL partnered with JAXA to develop AI-driven proficiency-forecast models that reduced simulator hours by up to 20% while maintaining safety thresholds. Even so, training capacity ceilings and high tuition deter recruits, especially for cargo and turboprop roles that require multiple ratings. Policy responses include relaxed visa pathways for foreign captains and widened eligibility criteria for military cadets. Still, these measures will mature only after 2027, leaving a medium-term capacity gap in the Japan Aviation market.

Other drivers and restraints analyzed in the detailed report include:

- Fleet Renewal Favoring Fuel-Efficient Aircraft

- Growth in E-commerce Driving Freighter Conversions

- Aircraft Delivery Delays and Ongoing Spare-Parts Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Military aviation contributed 18.77% CAGR to the Japan Aviation market between 2026 and 2031, outpacing all other categories despite commercial aviation holding a 57.32% revenue share in 2025. Fighter-procurement budgets earmarked for GCAP prototypes and F-35 follow-on orders underpin spending momentum, while transport-helicopter acquisitions address humanitarian relief and maritime security missions. The Japan Aviation market size for military fixed-wing assets is forecast to exceed USD 4.46 billion by 2031, reflecting steady pipeline funding and localized sustainment contracts. Commercial carriers nevertheless secure the larger revenue pool through passenger-traffic recovery and premium-cabin densification programs that enhance unit economics.

Rotorcraft fleets across defense and civil agencies capitalize on shared maintenance infrastructure, which lowers per-flight-hour costs and accelerates fleet turnover. Regulatory harmonization between the Japan Civil Aviation Bureau and the Ministry of Defense simplifies dual-use certification pathways, enabling manufacturers to amortize research and development costs across both civilian and military variants. The blended demand profile improves order-book visibility and fosters economies of scale, uplifting the Japan Aviation market.

Complete Report Scope:

- By Aircraft Type

- Commercial Aviation

- Passenger Aircraft

- Narrowbody Aircraft

- Widebody Aircraft

- Freighter

- Passenger Aircraft

- General Aviation

- Business Jets

- Large Jet

- Mid-Size Jet

- Light Jet

- Helicopters

- Others

- Business Jets

- Military Aviation

- Fixed-Wing Aircraft

- Multi-Role Aircraft

- Training Aircraft

- Transport Aircraft

- Others

- Rotorcraft

- Multi-Mission Helicopter

- Transport Helicopter

- Training

- Fixed-Wing Aircraft

- Commercial Aviation

- By Propulsion Technology

- Turboprop

- Turbofan

- Piston Engine

- Turboshaft

- Others

- By End User

- Civil and Commercial Operators

- Government and Defense Agencies

- Business and General Aviation Operators

List of Companies Covered in this Report:

- Airbus SE

- The Boeing Company

- Kawasaki Heavy Industries Ltd.

- SUBARU CORPORATION

- Lockheed Martin Corporation

- Mitsubishi Heavy Industries, Ltd.

- ShinMaywa Industries, Ltd

- ATR

- Bombardier Inc.

- Textron Inc.

- Leonardo S.p.A

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (RPK)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-Net-Worth-Individual (HNWI)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Surge in inbound tourism post pandemic

- 5.2.2 Record defense budget boosting fighter and rotorcraft procurement

- 5.2.3 Fleet renewal by airlines favoring fuel-efficient aircraft

- 5.2.4 Growth in e-commerce increasing demand for freighter conversions

- 5.2.5 Steady helicopter replacement demand in disaster response and offshore missions

- 5.2.6 Expansion of domestic carbon fiber capacity strengthening supply chain

- 5.3 Market Restraints

- 5.3.1 Pilot shortage driven by aging workforce and training limitations

- 5.3.2 Aircraft delivery delays and ongoing spare parts shortages

- 5.3.3 High landing fees and slot constraints at Tokyo airports

- 5.3.4 Termination of the SpaceJet program reducing indigenous OEM expertise

- 5.4 Value Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Bargaining Power of Suppliers

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Aircraft Type

- 6.1.1 Commercial Aviation

- 6.1.1.1 Passenger Aircraft

- 6.1.1.1.1 Narrowbody Aircraft

- 6.1.1.1.2 Widebody Aircraft

- 6.1.1.2 Freighter

- 6.1.1.1 Passenger Aircraft

- 6.1.2 General Aviation

- 6.1.2.1 Business Jets

- 6.1.2.1.1 Large Jet

- 6.1.2.1.2 Mid-Size Jet

- 6.1.2.1.3 Light Jet

- 6.1.2.2 Helicopters

- 6.1.2.3 Others

- 6.1.2.1 Business Jets

- 6.1.3 Military Aviation

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.3.1.1 Multi-Role Aircraft

- 6.1.3.1.2 Training Aircraft

- 6.1.3.1.3 Transport Aircraft

- 6.1.3.1.4 Others

- 6.1.3.2 Rotorcraft

- 6.1.3.2.1 Multi-Mission Helicopter

- 6.1.3.2.2 Transport Helicopter

- 6.1.3.2.3 Training

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.1 Commercial Aviation

- 6.2 By Propulsion Technology

- 6.2.1 Turboprop

- 6.2.2 Turbofan

- 6.2.3 Piston Engine

- 6.2.4 Turboshaft

- 6.2.5 Others

- 6.3 By End User

- 6.3.1 Civil and Commercial Operators

- 6.3.2 Government and Defense Agencies

- 6.3.3 Business and General Aviation Operators

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Airbus SE

- 7.4.2 The Boeing Company

- 7.4.3 Kawasaki Heavy Industries Ltd.

- 7.4.4 SUBARU CORPORATION

- 7.4.5 Lockheed Martin Corporation

- 7.4.6 Mitsubishi Heavy Industries, Ltd.

- 7.4.7 ShinMaywa Industries, Ltd

- 7.4.8 ATR

- 7.4.9 Bombardier Inc.

- 7.4.10 Textron Inc.

- 7.4.11 Leonardo S.p.A

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-need Assessment

9 KEY STRATEGIC QUESTIONS FOR JAPAN AVIATION CEOS