PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073621

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073621

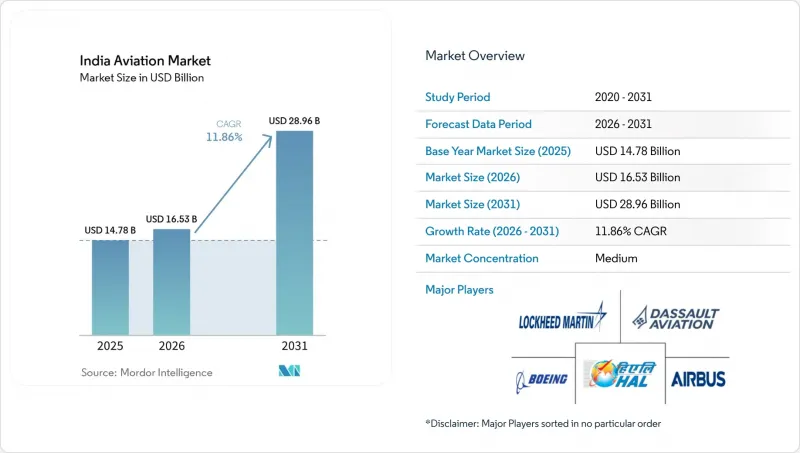

India Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india aviation market size is expected to grow from USD 14.78 billion in 2025 to USD 16.53 billion in 2026 and is forecast to reach USD 28.96 billion by 2031 at 11.86% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Commercial Aviation, General Aviation, and Military Aviation), Propulsion Technology (Turboprop, Turbofan, Piston Engine, Turboshaft, and Others), and End User (Civil and Commercial Operators, Government and Defense Agencies, and Business and General Aviation Owners). The Market Forecasts are Provided in Terms of Value (USD).

India Aviation Market Trends and Insights

Post-COVID passenger rebound and airport capacity expansion

Domestic passenger traffic increased to 164 million in 2024, representing 95% of the 2019 level, while international recovery reached 87%. The number of operational airports doubled from 74 in 2014 to 148 by 2024, easing slot congestion at Delhi, Mumbai, and Bengaluru. Capacity additions, such as Navi Mumbai International Airport and the enlargement of Delhi Terminal 1, have increased available slots by 35% since 2022, supporting a projected 300 million passengers by 2030. These steps address historical choke points and redistribute traffic across a broader airport network, aligning runway, terminal, and air traffic control investments with latent demand. Accelerated certification of new airports under UDAN further tightens the link between infrastructure rollout and traffic recovery, ensuring that the India Aviation market maintains momentum even as yields normalize.

India's FY27 target of over 220 operational airports

Seventy-two new airports are at various stages of construction as of 2024, bringing the planned total to more than 220 by FY27. Greenfield sites in Jewar, Dholera, and Bhogapuram complement brownfield upgrades, raising national capacity while bringing aviation access to 1 billion Indians. Dedicated cargo hubs are integrated into the rollout, directly responding to a 15% annual growth in cargo. UDAN 5.0 added 25 fresh routes and 19 helicopter links during 2024, underscoring the government's campus-to-capital connectivity model. The program aligns with the Make-in-India initiative by establishing new maintenance bases and parts-manufacturing clusters near emerging airports, thereby deepening supply-chain roots in underserved geographies.

Persistent volatility in aviation turbine fuel prices and limited hedging options

Aviation turbine fuel accounted for 35-40% of airline operating costs in 2024 and experienced intra-year price swings of 45%. State-level VAT differentials ranging from 1% to 30% further distort cost structures. Indian carriers hedge only 15% of their fuel needs, compared to 60-80% for global peers, a gap attributed to the absence of sophisticated derivatives in local markets. The cost spike forced fare surcharges, reduced capacity deployment by cash-strapped carriers, and increased break-even load factors. Without a functional jet-fuel futures market, airlines will continue to absorb volatility or pass it on to travelers, tempering the expansion of the India Aviation market's profit pool over the near term.

Other drivers and restraints analyzed in the detailed report include:

- Increase in defense capital outlay driving military aircraft orders

- Growing express cargo demand from e-commerce in Tier-2 and Tier-3 cities

- Infrastructure bottlenecks at Tier-3 airports affecting logistics efficiency

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation accounted for 85.12% of the Indian aviation market size in 2025, driven by the expansion of full-service and low-cost carriers, which increased their fleets and frequencies. IndiGo's order book and Air India's post-merger fleet of 470+ aircraft underline narrowbody leadership, while widebodies gain traction for long-haul routes at an 10.85% CAGR. Military aviation, although smaller, expands at a rate, with the fastest growth at a 13.92% CAGR, fueled by domestic fighter programs and helicopter procurement under Atmanirbhar Bharat.

The breadth of the commercial segment aids cabin interiors, ground-support equipment, and digital services suppliers, creating a multiplier effect within the Indian aviation market. General aviation holding an 8.62% share, saw business jet registrations rise 35% in 2024, reflecting corporate India's focus on time-efficient mobility. Military-segment acceleration broadens the industrial base, drawing private firms into tier-1 and tier-2 supply roles under offset obligations. Collectively, diversified aircraft demand procurement helps absorb manufacturing investments, stabilizing production volumes across market cycles.

Complete Report Scope:

- By Aircraft Type

- Commercial Aviation

- Passenger Aircraft

- Narrowbody Aircraft

- Widebody Aircraft

- Freighter

- Passenger Aircraft

- General Aviation

- Business Jets

- Large Jet

- Mid-Size Jet

- Light Jet

- Helicopters

- Others

- Business Jets

- Military Aviation

- Fixed-Wing Aircraft

- Multi-Role Aircraft

- Training Aircraft

- Transport Aircraft

- Others

- Rotorcraft

- Multi-Mission Helicopter

- Transport Helicopter

- Training

- Fixed-Wing Aircraft

- Commercial Aviation

- By Propulsion Technology

- Turboprop

- Turbofan

- Piston Engine

- Turboshaft

- Others

- By End User

- Business and General Aviation Operators

- Civil and Commercial Operators

- Government and Defense Agencies

List of Companies Covered in this Report:

- Airbus SE

- The Boeing Company

- Hindustan Aeronautics Limited (HAL)

- ATR

- Dassault Aviation

- Lockheed Martin Corporation

- Leonardo S.p.A

- Bombardier Inc.

- Textron Inc.

- Embraer S.A.

- Tata Advanced Systems Limited

- Aeronautical Development Agency

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (RPK)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-Net-Worth-Individual (HNWI)

- 4.9 Regulatory Framework

- 4.10 Value Chain Analysis

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Post-COVID passenger rebound and airport capacity expansion

- 5.2.2 India's FY27 target of over 220 operational airports

- 5.2.3 Increase in defense capital outlay driving military aircraft orders

- 5.2.4 Growing express cargo demand from e-commerce in Tier-2 and Tier-3 cities

- 5.2.5 Tax incentives supporting indigenous avionics research and development

- 5.2.6 SAF blending mandate from 2027 catalyzing new aviation fuel supply chains

- 5.3 Market Restraints

- 5.3.1 Persistent volatility in aviation turbine fuel (ATF) prices and limited hedging options

- 5.3.2 Infrastructure bottlenecks at Tier-3 airports affecting logistics efficiency

- 5.3.3 Shortage of skilled pilots and aircraft maintenance engineers despite training initiatives

- 5.3.4 Rupee depreciation posing risks to dollar-denominated aircraft lease agreements

- 5.4 Value Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Bargaining Power of Suppliers

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Aircraft Type

- 6.1.1 Commercial Aviation

- 6.1.1.1 Passenger Aircraft

- 6.1.1.1.1 Narrowbody Aircraft

- 6.1.1.1.2 Widebody Aircraft

- 6.1.1.2 Freighter

- 6.1.1.1 Passenger Aircraft

- 6.1.2 General Aviation

- 6.1.2.1 Business Jets

- 6.1.2.1.1 Large Jet

- 6.1.2.1.2 Mid-Size Jet

- 6.1.2.1.3 Light Jet

- 6.1.2.2 Helicopters

- 6.1.2.3 Others

- 6.1.2.1 Business Jets

- 6.1.3 Military Aviation

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.3.1.1 Multi-Role Aircraft

- 6.1.3.1.2 Training Aircraft

- 6.1.3.1.3 Transport Aircraft

- 6.1.3.1.4 Others

- 6.1.3.2 Rotorcraft

- 6.1.3.2.1 Multi-Mission Helicopter

- 6.1.3.2.2 Transport Helicopter

- 6.1.3.2.3 Training

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.1 Commercial Aviation

- 6.2 By Propulsion Technology

- 6.2.1 Turboprop

- 6.2.2 Turbofan

- 6.2.3 Piston Engine

- 6.2.4 Turboshaft

- 6.2.5 Others

- 6.3 By End User

- 6.3.1 Business and General Aviation Operators

- 6.3.2 Civil and Commercial Operators

- 6.3.3 Government and Defense Agencies

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Airbus SE

- 7.4.2 The Boeing Company

- 7.4.3 Hindustan Aeronautics Limited (HAL)

- 7.4.4 ATR

- 7.4.5 Dassault Aviation

- 7.4.6 Lockheed Martin Corporation

- 7.4.7 Leonardo S.p.A

- 7.4.8 Bombardier Inc.

- 7.4.9 Textron Inc.

- 7.4.10 Embraer S.A.

- 7.4.11 Tata Advanced Systems Limited

- 7.4.12 Aeronautical Development Agency

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-need Assessment

9 KEY STRATEGIC QUESTIONS FOR INDIA AVIATION CEOS