PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066701

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066701

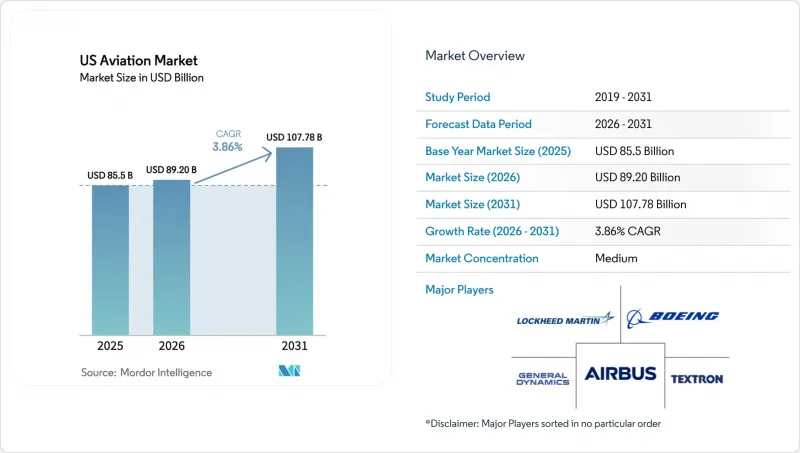

US Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the uS aviation market size is expected to grow from USD 85.50 billion in 2025 to USD 89.20 billion in 2026 and is projected to reach USD 107.78 billion by 2031 at a 3.86% CAGR.

This report is Segmented by Aircraft Type (Commercial Aviation, General Aviation, and Military Aviation), Propulsion Technology (Turboprop, Turbofan, Piston Engine, Turboshaft, and Others), and End User (Civil and Commercial Operators, Government and Defense Agencies, and Business and General Aviation Owners). The Market Forecasts are Provided in Terms of Value (USD).

US Aviation Market Trends and Insights

Recovery in Domestic Passenger Traffic

TSA checkpoints processed an average daily volume of nearly 2.4 million passengers in February 2026, including a mid-month peak of 2.7 million, indicating resilient leisure demand even as the business travel recovery remains uneven across hubs and corporate-heavy routes. In October 2025, passenger activity reached a new monthly high, yet domestic load factors softened as carriers paced growth against certification and delivery schedules that constrained near-term capacity additions. FAA's long-term forecast projects steady mainline enplanement gains over the next decade, while the regional segment adjusts to pilot supply and economic factors that favor larger-gauge aircraft in many domestic markets. The US aviation market remains supply-bound rather than demand-limited in the near term, given that network carriers continue to hold firm on core schedules while deferring some planned fleet retirements until delivery cadence stabilizes. Strategic orders from major airlines signal confidence that underlying demand will meet capacity once production normalizes and infrastructure upgrades reduce bottlenecks at constrained airports.

Continued Growth of E-Commerce Boosting Air-Cargo Demand

Global air cargo volumes increased in 2025, but performance across regions diverged as North American flows adjusted to policy changes and the return of belly cargo in intercontinental markets. Domestic air freight revenue ton-miles gained traction on last-mile parcel density and healthcare logistics, while the reopening of passenger widebody networks compressed freighter yields on certain lanes. The market benefits from sustained e-commerce growth, which increases throughput at integrator hubs and secondary cargo airports. Still, network design is evolving as trade and customs regimes influence route choices and staging. Leading integrators continue to tune fleet plans and facility investments to align with parcel cycles, while reallocating capacity between freighters and belly cargo supports a flexible response to peak traffic windows. Over the forecast period, cargo growth remains additive to passenger networks, though its contribution to overall revenue will vary by carrier mix, product composition, and cross-border policy setting.

Supply Chain Bottlenecks for Titanium, Composites, and Avionics

Backlogs now represent extended production runways, reshaping airline retirement plans and keeping older aircraft in service longer, increasing fuel costs and maintenance exposure while dampening the pace of fleet refresh in the US aviation market. OEMs and engine makers continue to balance quality controls and ramp schedules as certification requirements remain more extensive than in prior cycles, which has extended the time-to-market for specific variants. Tiered suppliers in materials, avionics, and fasteners remain sensitive to one-off disruptions and single-sourcing, heightening risk to delivery plans during a period of elevated demand. Over the medium term, supply resilience depends on capital and workforce readiness at smaller suppliers, where hiring and training pipelines lag retirements and where financing constraints limit surge capacity. These bottlenecks continue to pressure lease rates, yield management, and maintenance turn times, affecting carriers' schedule reliability and unit economics.

Other drivers and restraints analyzed in the detailed report include:

- Sustained DoD Outlays for Next-Generation Combat and Support Aircraft

- FAA "Innovate 2028" Digital Tower Rollout Accelerating Regional Airport Upgrades

- Community-level Opposition Delaying SAF Blending and Storage Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial aviation captured 54.20% of the market share in 2025, and military aviation is projected to grow at the fastest rate with a 4.45% CAGR through 2031. Within commercial fleets, narrowbody aircraft remain central to network plans as carriers invest in fuel-efficient types to improve seat-mile economics and restore capacity with reliability. Delivery schedules and certification timelines have led operators to extend aircraft life, raising maintenance exposure and keeping lease markets tight across popular variants in the US aviation market. Airlines with strong balance sheets placed strategic orders to secure multi-year delivery positions, which helps de-risk replacement cycles once production stabilizes.

Defense demand anchors growth for the fastest-rising segment as procurement and sustainment funding levels prioritize fifth-generation fleets and next-generation platforms. The F-35 enterprise continues to scale across US services and partner nations through multi-lot awards that underpin system upgrades and maintain a deep industrial footprint. General aviation sustained healthy large-cabin and midsize jet deliveries in 2025, supported by corporate and high-net-worth demand and strengthened by OEM product refresh initiatives and avionics upgrades. These dynamics set a balanced foundation for the market as commercial carriers optimize gauge and schedule integrity, and defense programs stabilize supplier utilization with longer-horizon commitments.

List of Companies Covered in this Report:

- Air Tractor, Inc.

- Airbus SE

- The Boeing Company

- Avions de Transport Regional GIE (ATR)

- Bombardier Inc.

- Cirrus Design Corporation

- Dassault Aviation S.A.

- Embraer S.A.

- General Dynamics Corporation

- Honda Aircraft Company (Honda Motor Co., Ltd.)

- Leonardo S.p.A.

- Lockheed Martin Corporation

- MD Helicopters LLC

- Northrop Grumman Corporation

- Pilatus Aircraft Ltd.

- Piper Aircraft, Inc.

- Robinson Helicopter Company

- Textron Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.2 Air Transport Freight

- 4.3 Gross Domestic Product

- 4.4 Revenue Passenger Kilometers (RPK)

- 4.5 Inflation Rate

- 4.6 Active Fleet Data

- 4.7 Defense Spending

- 4.8 High-Net-Worth-Individual (HNWI)

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Recovery in domestic passenger traffic

- 5.2.2 Continued growth of e-commerce boosting air cargo demand

- 5.2.3 Sustained DoD outlays for next-generation combat and support aircraft

- 5.2.4 FAA "Innovate 2028" digital tower rollout accelerating regional airport upgrades

- 5.2.5 Airline fleet renewal programs favoring fuel-efficient models

- 5.2.6 Venture capital funding surge for electric short-haul aircraft creating new OEM revenue pools

- 5.3 Market Restraints

- 5.3.1 Supply chain bottlenecks for titanium, composites, and avionics

- 5.3.2 Community-level opposition delaying SAF blending and storage infrastructure

- 5.3.3 Persistent pilot, airframe, and powerplant mechanic shortages inflating labor costs

- 5.3.4 Escalating cyber insurance premiums for connected aircraft systems

- 5.4 Value Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Bargaining Power of Suppliers

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Aircraft Type

- 6.1.1 Commercial Aviation

- 6.1.1.1 Passenger Aircraft

- 6.1.1.1.1 Narrowbody Aircraft

- 6.1.1.1.2 Widebody Aircraft

- 6.1.1.1.3 Regional Jets

- 6.1.1.1 Passenger Aircraft

- 6.1.2 General Aviation

- 6.1.2.1 Business Jets

- 6.1.2.1.1 Large Jet

- 6.1.2.1.2 Mid-Size Jet

- 6.1.2.1.3 Light Jet

- 6.1.2.2 Piston and Turboprop Aircraft

- 6.1.2.3 Commercial Helicopters

- 6.1.2.1 Business Jets

- 6.1.3 Military Aviation

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.3.1.1 Combat Aircraft

- 6.1.3.1.2 Multi-Role Aircraft

- 6.1.3.1.3 Transport Aircraft

- 6.1.3.1.4 Training Aircraft

- 6.1.3.2 Rotorcraft

- 6.1.3.2.1 Multi-Mission Helicopter

- 6.1.3.2.2 Transport Helicopter

- 6.1.3.2.3 Others

- 6.1.3.1 Fixed-Wing Aircraft

- 6.1.1 Commercial Aviation

- 6.2 By Propulsion Technology

- 6.2.1 Turboprop

- 6.2.2 Turbofan

- 6.2.3 Piston Engine

- 6.2.4 Turboshaft

- 6.2.5 Others

- 6.3 By End User

- 6.3.1 Civil and Commercial Operators

- 6.3.2 Government and Defense Agencies

- 6.3.3 Business and General Aviation Owners

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Air Tractor, Inc.

- 7.4.2 Airbus SE

- 7.4.3 The Boeing Company

- 7.4.4 Avions de Transport Regional GIE (ATR)

- 7.4.5 Bombardier Inc.

- 7.4.6 Cirrus Design Corporation

- 7.4.7 Dassault Aviation S.A.

- 7.4.8 Embraer S.A.

- 7.4.9 General Dynamics Corporation

- 7.4.10 Honda Aircraft Company (Honda Motor Co., Ltd.)

- 7.4.11 Leonardo S.p.A.

- 7.4.12 Lockheed Martin Corporation

- 7.4.13 MD Helicopters LLC

- 7.4.14 Northrop Grumman Corporation

- 7.4.15 Pilatus Aircraft Ltd.

- 7.4.16 Piper Aircraft, Inc.

- 7.4.17 Robinson Helicopter Company

- 7.4.18 Textron Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-need Assessment

9 KEY STRATEGIC QUESTIONS FOR US AVIATION CEOS