Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1430950

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1430950

Global Automotive Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2021 - 2026)

PUBLISHED:

PAGES: 80 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

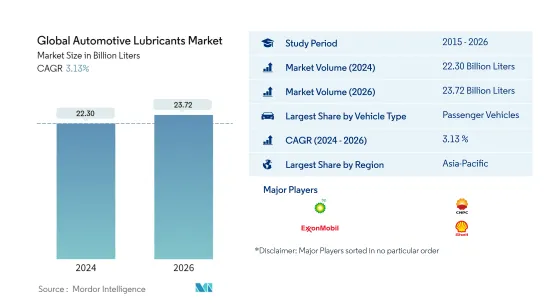

The Global Automotive Lubricants Market size is estimated at 22.30 Billion Liters in 2024, and is expected to reach 23.72 Billion Liters by 2026, growing at a CAGR of 3.13% during the forecast period (2024-2026).

Key Highlights

- Largest Segment by Vehicle Type - Passenger Vehicles : The large fleet size of passenger vehicles across the globe has resulted in this sector accounting for the highest lubricant consumption among all the different vehicle types.

- Fastest Segment by Vehicle Type - Motorcycles : The sales boost for motorcycles in several countries despite the COVID-19 pandemic is likely to continue and boost the lubricant consumption by the sector in the future.

- Largest Regional Market - Asia-Pacific : Asia-Pacific is home to countries with large vehicle fleets like China, India & Indonesia. As a result, lubricant consumption by this sector was highest in Asia-Pacific.

- Fastest Growing Regional Market - Asia-Pacific : The low penetration of synthetic lubricants and expected high growth rates of vehicle population in countries like India are likely to drive lubricant consumption in APAC.

Automotive Lubricants Market Trends

Largest Segment By Vehicle Type : Passenger Vehicles

- In the global automotive industry, the passenger vehicles (PV) segment accounted for almost 55.1% share in the total number of on-road vehicles during 2020, followed by motorcycles and passenger vehicles with 34.7% and 10.1% shares, respectively.

- The passenger vehicles segment accounted for the highest share of 53.6% in the total automotive lubricant volume consumption in 2020, followed by the commercial vehicles segment that accounted for a share of 37.3%. During the same year, travel restrictions to curb COVID-19 significantly affected the usage of these vehicles and their lubricant consumption.

- During 2021-2026, lubricant consumption by the motorcycles segment is expected to witness the highest CAGR growth, amounting to 5.06%. The growing motorcycle sales combined with the easing down of COVID-19 pandemic-related travel restrictions are likely to be the key factors driving this trend.

Largest Region : Asia-Pacific

- Consumption of automotive lubricants is dominated by Asia-Pacific, North America, and Europe. In 2020, Asia-Pacific accounted for about 43% of the total automotive lubricant consumption globally, while North America and Europe accounted for a share of around 20% and 14.8%, respectively.

- The COVID-19 outbreak in 2020 significantly affected automotive lubricant consumption in many countries worldwide. North America was the most affected, with a 17.4% drop, during 2019-2020. Africa was the least affected, with a 4.7% drop in its automotive lubricant consumption.

- During 2021-2026, Asia-Pacific is likely to be the fastest-growing lubricant market, as the consumption is likely to increase at a CAGR of 4.89%, followed by Africa and the Middle East, which are expected to record a CAGR of 4.13% and 3.22%, respectively.

Automotive Lubricants Industry Overview

The Global Automotive Lubricants Market is moderately consolidated, with the top five companies occupying 40.21%. The major players in this market are BP PLC (Castrol), China National Petroleum Corporation, Exxon Mobil Corporation, Royal Dutch Shell PLC and TotalEnergies (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 90298

TABLE OF CONTENTS

1 Executive Summary & Key Findings

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 Key Industry Trends

- 3.1 Automotive Industry Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 Market Segmentation

- 4.1 By Vehicle Type

- 4.1.1 Commercial Vehicles

- 4.1.2 Motorcycles

- 4.1.3 Passenger Vehicles

- 4.2 By Product Type

- 4.2.1 Engine Oils

- 4.2.2 Greases

- 4.2.3 Hydraulic Fluids

- 4.2.4 Transmission & Gear Oils

- 4.3 By Region

- 4.3.1 Africa

- 4.3.1.1 Egypt

- 4.3.1.2 Morocco

- 4.3.1.3 Nigeria

- 4.3.1.4 South Africa

- 4.3.1.5 Rest of Africa

- 4.3.2 Asia-Pacific

- 4.3.2.1 China

- 4.3.2.2 India

- 4.3.2.3 Indonesia

- 4.3.2.4 Japan

- 4.3.2.5 Malaysia

- 4.3.2.6 Philippines

- 4.3.2.7 Singapore

- 4.3.2.8 South Korea

- 4.3.2.9 Thailand

- 4.3.2.10 Vietnam

- 4.3.2.11 Rest of Asia-Pacific

- 4.3.3 Europe

- 4.3.3.1 Bulgaria

- 4.3.3.2 France

- 4.3.3.3 Germany

- 4.3.3.4 Italy

- 4.3.3.5 Norway

- 4.3.3.6 Poland

- 4.3.3.7 Russia

- 4.3.3.8 Spain

- 4.3.3.9 United Kingdom

- 4.3.3.10 Rest of Europe

- 4.3.4 Middle East

- 4.3.4.1 Iran

- 4.3.4.2 Qatar

- 4.3.4.3 Saudi Arabia

- 4.3.4.4 Turkey

- 4.3.4.5 UAE

- 4.3.4.6 Rest of Middle East

- 4.3.5 North America

- 4.3.5.1 Canada

- 4.3.5.2 Mexico

- 4.3.5.3 United States

- 4.3.5.4 Rest of North America

- 4.3.6 South America

- 4.3.6.1 Argentina

- 4.3.6.2 Brazil

- 4.3.6.3 Colombia

- 4.3.6.4 Rest of South America

- 4.3.1 Africa

5 Competitive Landscape

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Profiles

- 5.3.1 BP PLC (Castrol)

- 5.3.2 Chevron Corporation

- 5.3.3 China National Petroleum Corporation

- 5.3.4 China Petroleum & Chemical Corporation

- 5.3.5 Exxon Mobil Corporation

- 5.3.6 FUCHS

- 5.3.7 Idemitsu Kosan Co. Ltd

- 5.3.8 Royal Dutch Shell PLC

- 5.3.9 TotalEnergies

- 5.3.10 Valvoline Inc.

6 Appendix

- 6.1 Appendix-1 References

- 6.2 Appendix-2 List of Tables & Figures

7 Key Strategic Questions for Lubricants CEOs

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.