PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432575

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432575

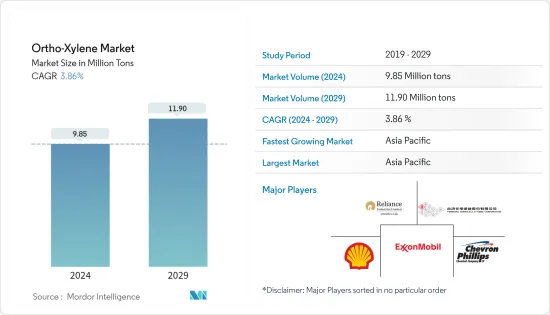

Ortho-Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Ortho-Xylene Market size is estimated at 9.85 Million tons in 2024, and is expected to reach 11.90 Million tons by 2029, growing at a CAGR of 3.86% during the forecast period (2024-2029).

The major factors driving the market studied are the increasing demand for ortho-xylene as an intermediate for PVC production, and extensive usage of ortho-xylene in the production of paints and adhesive.

Key Highlights

- Detrimental neurological effects of ortho-xylene and usage of naphthalene for the production of phthalic anhydride (PA) areexpected to hinder the growth of the market studied.

- Asia-Pacific dominated the global market, with the largest consumption recorded from the countries, such as China and India.

Ortho-Xylene Market Trends

Phthalic Anhydride (PA) to Dominate the Market

- Phthalic anhydride is industrially an important raw material for the production of anthraquinone. Itis also used in the manufacture of many vat dyes, as well as in alizarin and alizarin derivatives. It is used directly for the fluorescein, eosin, and rhodamine dyes.

- Several esters are made from phthalic anhydride, and are largely used in the plastics industry, as plasticizers. It is also used to manufacture alkyd resins, the glyptal and rezyl resins, dioctyl phthalate, and the poly-vinyl resins.

- The ever-increasing demand for phthalic anhydride has stimulated a search for alternative raw materials. Ortho-xylene, which is available in abundant quantities from the petroleum refineries, appears to be the most suitable.

- O-xylene has several advantages as a raw material for the production of phthalic anhydride. The oxidation of o-xylene permits a simpler feed system than that of the oxidation of naphthalene, due tothe liquid state of o-xylene.

- The theoretical amount of air required for oxidizing o-xylene is only two-thirdof the amount required for the oxidation of naphthalene. The heat emitted off during the reaction is 121 kcal less than that of naphthalene. The product is of higher purity, and the theoretical yield percentage is higher than that of naphthalene. Furthermore, as o-xylene is a liquid at ordinary temperature, its use permits a simpler feed system.

- Thus, with increasing demand for phthalic anhydrade, the consumption of o-xylene is likely to increase during the forecast period.

Asia-Pacific to Dominate the Market

- In the Asia-Pacific region, China is the largest economy in terms of GDP. The major proportion of ortho-xylene is used in the manufacture of phthalic anhydride that is used in the production of phthalate-based PVC plasticizers. China is the single largest market for plasticizers, with more than 40% of the global consumption. Some of the manufacturers of PVC in the country are Shin-Etsu Chemical Co. Limited, Xinjiang Zhongtai Chemical Co. Ltd, Lubrizol, Hanwha Chemical, Formosa Plastics, etc.

- PVC is widely used in the automotive industry. PVC's thermoplastic properties have lesser weight compared to metals. It has a lower cost of manufacturing methods compared to the cost of other methods. It is an ideal choice for exterior and automotive interior parts. PVC is favored for exterior parts, owing to its light weight, durability, easily shapeable quality, and attractive appearance.

- The overall cost of a component can be brought down to 20-60%, by using PVC instead of alternative materials. Some of the automotive components made with PVC include instrument panels, floor coverings, mud flaps, seals, sun visors, and anti-stone damage protection.

- China is by far the largest automotive manufacturer in the world, since 2009, with a current share of production of about 29.06%.

- The production decreased by 4.2% in 2018, owing to the decrease in domestic demand and penetration of automotive manufacturers to other countries. The decline is expected to be temporary, as the demand is still increasing.

- Therefore, owing to the aforementioned factors, the consumption of phthalic anhydride is high. This may lead to an increase in demand for ortho-xylene, during the forecast period.

Ortho-Xylene Industry Overview

The ortho-xylene market is fragmented in nature. The major companies includeRoyal Dutch Shell PLC,Reliance Industries Limited,China Petroleum & Chemical Corporation, andExxon Mobil Corporation, and Formosa Chemicals & Fibre Corp.among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand as an Intermediate for PVC Production

- 4.1.2 Extensive Usage of Ortho-xylene in Paints and Adhesive Industries

- 4.2 Restraints

- 4.2.1 Detrimental Neurological Effects of Ortho-xylene

- 4.2.2 Usage of Naphthalene for the Production of Phthalic Anhydride (PA)

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Phthalic Anhydride

- 5.1.2 Bactericides

- 5.1.3 Soybean Herbicides

- 5.1.4 Lube Oil Additives

- 5.1.5 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East & Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East & Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 China Petroleum & Chemical Corporation

- 6.4.2 Exxon Mobil Corporation

- 6.4.3 Flint Hills Resources

- 6.4.4 Formosa Chemicals and Fibre Corporation

- 6.4.5 KP Chemical Corp.

- 6.4.6 Nouri Petrochemical Company

- 6.4.7 Reliance industries Ltd

- 6.4.8 Royal Dutch Shell PLC

- 6.4.9 SK Global Chemical Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS