Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693647

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693647

Commercial Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 409 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

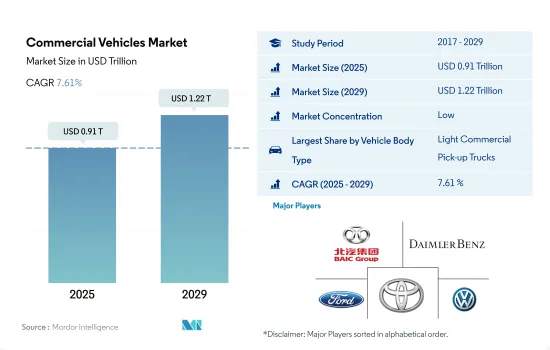

The Commercial Vehicles Market size is estimated at 0.91 trillion USD in 2025, and is expected to reach 1.22 trillion USD by 2029, growing at a CAGR of 7.61% during the forecast period (2025-2029).

- The industrial sector's growth in emerging economies and the rise in commercial logistics activities are key drivers of the demand for commercial vehicles. This demand surge is primarily fueled by the expanding construction and e-commerce industries, which are driving the need for efficient material transportation. Following a dip of three million units in 2020, the production of commercial vehicles rebounded, reaching approximately 23.2 million units in 2021, marking a steady recovery.

- With most international borders closed due to the COVID-19 pandemic, the commercial vehicle manufacturing industry faced prolonged disruptions in its supply chain in 2021, hampering market growth. The pandemic's impact on the transportation sector was profound, presenting significant hurdles for both the freight and manufacturing industries in ensuring smooth movement of goods.

- Due to increased demand for commercial vehicles, truck manufacturers have been introducing new advanced trucks to meet the rising demand and emission standards. Commercial vehicle leasing and the rental industry are also growing due to the increasing demand for operational efficiencies and the realization of economies of scale by businesses across multiple industries. E-commerce has become an essential component of the global retail framework in recent years. Over 2 billion people purchased goods or services online in 2020, and global e-commerce sales surpassed USD 4.2 trillion in the same year. The overall commercial vehicle market is expected to grow significantly in the future.

The rising concerns over carbon emissions from the transportation sector are expected to drive the penetration of electric commercial vehicles in the coming years

- In 2021, global commercial vehicle manufacturing rebounded, reaching approximately 23.2 million units, following a decline of 3 million units in 2020. Light commercial vehicles, typically weighing under 3.5 tons, are classified as such. Broadly, commercial vehicles refer to motor vehicles designed for transporting goods and people. North America took the lead in production, manufacturing 10.9 million commercial vehicles in 2021. Asia and Oceania emerged as the top producers of heavy trucks, with an estimated output of nearly 3.3 million units in 2021. A notable growth driver for this sector is the increasing demand for clean energy in the automotive industry.

- After a 13% dip from 2019 to 2020, global commercial vehicle output rebounded in 2021. The global commercial vehicles market faced significant disruptions during the pandemic, with manufacturing facilities shutting down due to national lockdowns that extended into 2020. Although the demand and output recovered in 2021, the market faced a setback due to a global chip shortage, leading to production cutbacks.

- Amid the rising concerns over carbon emissions from the transportation sector, the commercial fleet industry is prioritizing alternative fuel sources. Governments worldwide are taking the lead in implementing regulations to promote electric vehicle adoption. China, India, France, and the United Kingdom have announced plans to halt gasoline and diesel vehicle production by 2040. This shift is expected to drive the penetration of electric commercial vehicles in the coming years.

Global Commercial Vehicles Market Trends

The rising global demand and government support propel electric vehicle market growth

- Electric vehicles (EVs) have become indispensable in the automotive industry, driven by their potential to enhance energy efficiency and reduce greenhouse gas and pollution emissions. This surge is primarily attributed to growing environmental concerns and supportive government initiatives. Notably, global EV sales witnessed a robust 10.82% growth in 2022 compared to 2021. Projections indicate that annual sales of electric passenger cars will surpass 5 million by the end of 2025, accounting for approximately 15% of total vehicle sales.

- Leading manufacturers and organizations, like the London Metropolitan Police & Fire Service, have been actively pursuing their electric mobility strategies. For instance, they have set a target of a zero-emission fleet by 2025, with a goal of electrifying 40% of their vans by 2030 and achieving full electrification by 2040. Similar trends are expected globally, with the period from 2024 to 2030 witnessing a surge in demand and sales of electric vehicles.

- Asia-Pacific and Europe are poised to dominate electric vehicle production, driven by their advancements in battery technology and vehicle electrification. In May 2020, Kia Motors Europe unveiled its "Plan S," signaling a strategic shift toward electrification. This decision came on the heels of record-breaking sales of Kia's EVs in Europe. Kia has ambitious plans to introduce 11 EV models globally by 2025, spanning various segments like passenger vehicles, SUVs, and MPVs. The company aims to achieve annual global EV sales of 500,000 by 2026.

Commercial Vehicles Industry Overview

The Commercial Vehicles Market is fragmented, with the top five companies occupying 30%. The major players in this market are BAIC Motor Corporation Ltd., Daimler AG (Mercedes-Benz AG), Ford Motor Company, Toyota Motor Corporation and Volkswagen AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 93035

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.1.1 Africa

- 4.1.2 Asia-Pacific

- 4.1.3 Europe

- 4.1.4 Middle East

- 4.1.5 North America

- 4.1.6 South America

- 4.2 GDP Per Capita

- 4.2.1 Africa

- 4.2.2 Asia-Pacific

- 4.2.3 Europe

- 4.2.4 Middle East

- 4.2.5 North America

- 4.2.6 South America

- 4.3 Consumer Spending For Vehicle Purchase (cvp)

- 4.3.1 Africa

- 4.3.2 Asia-Pacific

- 4.3.3 Europe

- 4.3.4 Middle East

- 4.3.5 North America

- 4.3.6 South America

- 4.4 Inflation

- 4.4.1 Africa

- 4.4.2 Asia-Pacific

- 4.4.3 Europe

- 4.4.4 Middle East

- 4.4.5 North America

- 4.4.6 South America

- 4.5 Interest Rate For Auto Loans

- 4.6 Impact Of Electrification

- 4.7 EV Charging Station

- 4.8 Battery Pack Price

- 4.8.1 Africa

- 4.8.2 Asia-Pacific

- 4.8.3 Europe

- 4.8.4 Middle East

- 4.8.5 North America

- 4.8.6 South America

- 4.9 New Xev Models Announced

- 4.10 Logistics Performance Index

- 4.10.1 Africa

- 4.10.2 Asia-Pacific

- 4.10.3 Europe

- 4.10.4 Middle East

- 4.10.5 North America

- 4.10.6 South America

- 4.11 Fuel Price

- 4.12 Oem-wise Production Statistics

- 4.13 Regulatory Framework

- 4.14 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Commercial Vehicles

- 5.1.1.1 Heavy-duty Commercial Trucks

- 5.1.1.2 Light Commercial Pick-up Trucks

- 5.1.1.3 Light Commercial Vans

- 5.1.1.4 Medium-duty Commercial Trucks

- 5.1.1 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Hybrid and Electric Vehicles

- 5.2.1.1 By Fuel Category

- 5.2.1.1.1 BEV

- 5.2.1.1.2 FCEV

- 5.2.1.1.3 HEV

- 5.2.1.1.4 PHEV

- 5.2.2 ICE

- 5.2.2.1 By Fuel Category

- 5.2.2.1.1 CNG

- 5.2.2.1.2 Diesel

- 5.2.2.1.3 Gasoline

- 5.2.2.1.4 LPG

- 5.2.1 Hybrid and Electric Vehicles

- 5.3 Region

- 5.3.1 Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Malaysia

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Rest-of-APAC

- 5.3.3 Europe

- 5.3.3.1 Czech Republic

- 5.3.4 Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.6 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BAIC Motor Corporation Ltd.

- 6.4.2 BYD Auto Co. Ltd.

- 6.4.3 Daimler AG (Mercedes-Benz AG)

- 6.4.4 Dongfeng Motor Corporation

- 6.4.5 Ford Motor Company

- 6.4.6 General Motors Company

- 6.4.7 Groupe Renault

- 6.4.8 Mahindra & Mahindra Limited

- 6.4.9 Nissan Motor Co. Ltd.

- 6.4.10 Rivian Automotive Inc.

- 6.4.11 Saic General Motors Corporation Limited

- 6.4.12 Scania AB

- 6.4.13 Tata Motors Limited

- 6.4.14 Toyota Motor Corporation

- 6.4.15 Volkswagen AG

- 6.4.16 Volvo Group

7 KEY STRATEGIC QUESTIONS FOR VEHICLES CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.