PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687769

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1687769

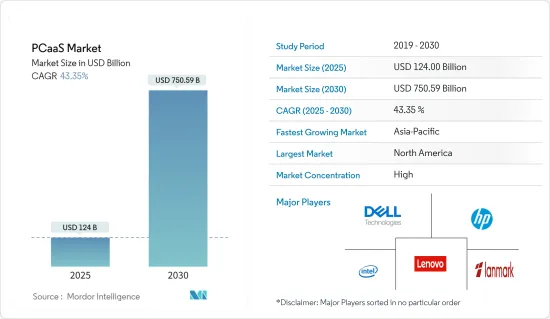

PCaaS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The PCaaS Market size is estimated at USD 124.00 billion in 2025, and is expected to reach USD 750.59 billion by 2030, at a CAGR of 43.35% during the forecast period (2025-2030).

The increasing need to reduce IT staffing costs and workload and the adoption of PCaaS by small and medium-sized enterprises (SMEs) are the key factors driving demand in the market. Recently, HP Inc. presented a comprehensive set of PCaaS offerings for customers and channel partners, including the launch of DaaS, an evolution of PCaaS aimed at simplifying and speeding up IT management and thereby reducing IT staffing costs by providing a comprehensive, end-to-end solution for businesses.

Key Highlights

- The increasing IT budget and focus on business support applications are the vital factors driving the market's growth. According to Spiceworks' Ziff Davis, 64% of enterprises (with more than 500 employees) planned to increase their IT budgets by the end of last year.Also, some of the major reasons for the IT budget increase include increased priority on IT projects (49%), a need to upgrade outdated IT infrastructure (47%), and increased security concerns (44%). Furthermore, by last year, 9% of the total software and hosted/cloud-based services budget was expected to be allocated for business support applications. The emphasis on improving business applications in line with an increase in IT budgets creates new opportunities for the PCaaS market.

- Efficiency plays a vital role in SMEs' IT expenditures. Owing to the benefits that PCaaS offers, the adoption of these solutions is high among SMEs. According to Intel, small business workers lose more than one workweek per year due to old PCs that use outdated technology. The PCaaS offering is expected to evade unnecessary costs related to efficiency, security, and workforce productivity. Such advantages will likely drive the demand for PCaaS in SMEs during the forecast period.

- An assessment done by Schneider Electric and Hartford Steam Boiler in the past year revealed that there are a large number of factors that contribute to equipment failure. These factors include environmental issues (8%), humidity (9%), and improper operations (9%), among the many factors responsible for the failures. In another survey of 200 executives conducted by Honeywell, approximately 42% admitted to operating equipment in an improper manner, resulting in equipment failure.Such scenarios indirectly add to the demand for PCaaS services, especially in the case of large organizations.

- Despite PCaaS improving employee flexibility, customer experience, and ROI, lack of product differentiation is a factor that affects the market's growth. Most of the players in the market offer similar benefits to their clients, which include monthly fixed-time payments, PC lifecycle support, and improved productivity, among others.

- With the growth in cloud-based desktop services during the COVID-19 pandemic situation, PCaaS packages have been highly efficient and cost-effective for supporting [work-from-home] employees, according to Pund-IT. Long-term, more people are likely to use PCaaS because of the strong digital transformation and the need to cut IT costs to keep businesses running.

PC as a Service Market Trends

Small and Medium-scale Organizations is Expected to Register a Significant Growth

- Survey research shows cloud SMBs are more likely to adopt PCaaS and refresh PCs than SMBs with an ad hoc cloud approach. Similarly, SMEs with an organization-wide mobility strategy are more open to PCaaS than those with siloed mobility initiatives.

- According to a survey by Techaisle, 9% of SMEs have adopted PC-as-a-Service (PCaaS), and 32% are aware of PCaaS plans. Acquisition of the latest technology, the potential to reduce IT support workload, and predictable costs were key reasons for using PCaaS. Awareness of PCaaS increases from a low of 21% (unweighted) among small businesses to a high of 64% within the 500-999 employee size segments.

- The growing digital adoption in SMEs has led to a need for PCs across the globe. According to HP India, PCs have emerged as more users sign in from home. The need for adoption was even more significant for SMBs whose digitization levels were traditionally lower. More importantly, SMBs in India recognized the importance of going digital to revive their businesses. Also, three-quarters (75%) of the surveyed companies believe digital adoption is essential to their success. The need for PCs also drives the growth of the market.

- Vendors' get-what-you-need and pay-as-you-go financing models make it suitable for SMEs. Thus, with the growth of technologies and support from vendors in the market, the adoption of PCaaS is growing in SMEs. Also, the increasing demand from small and medium-scale organizations due to the cost benefits is a critical factor driving the growth of the PCaaS market. Small and medium-sized enterprises (SMEs) are critical for all countries around the world because they contribute significantly to GDP.

- Organizations are growing rapidly in terms of technology adoption, which also contributes to market growth. According to the European Commission, the major technologies adopted by SMEs include cloud computing (43%), high-speed infrastructure (32%), smart devices (21%), big data analytics (10%), and others. The growth in cloud adoption complements the push for cloud PCaaS solutions that offer SMEs strong data security and protection.

North America is Expected to Hold the largest market share

- The United States is one of the biggest markets for PCs due to the presence of major players such as Dell, HP Inc., Samsung, and others. 2021 proved to be one of the best years for the display monitor market due to increased consumer and commercial demand. Moreover, with the surge in demand for PC units, the market is expected to grow and expand drastically within the region.

- Customers also prefer the PCaaS model in the commercial market offered by large corporations like Dell since it provides no upfront costs, fixed monthly rentals, and the most recent features for antivirus, security, data removal, recycling, and trouble detection. During the planned time frame, all of these factors are expected to support demand from the business sector.

- Some of the key firms in the sector are also based in the area, such as Microsoft, Dell EMC, and others, which are continually investing in developing the technology through R&D, strategic partnerships, and mergers and acquisitions, which have allowed them to gain a stronger footprint in the market. For instance, in November 2021, HP expanded its digital services portfolio to support companies' growing demand to make IT more adaptive to change, deliver more consistent end-user experiences, and leverage new service consumption models that match the various businesses' expectations. The new HP Subscription Management Service is made for small and medium-sized businesses. It lets businesses decide what software to buy based on accurate information about their workforce.

- The region is one of the biggest leaders in cloud adoption, which has helped PCaaS and DaaS companies use the cloud's advantages. For instance, VMware disclosed its intentions to introduce the Managed Desktops Solution, a new DaaS service on the VMware Cloud on AWS. Over the projected period, this is expected to accelerate the adoption of the technology.

- The COVID-19 pandemic caused a rapid shift in the working environment in Canada. Remote working methods helped raise Canada's office vacancy rate during the COVID-19 pandemic. According to a report from CBRE, the national vacancy rate for offices increased by 3.1% from the start of the pandemic until February 2021. This has caused Canadians to invest less in traditional PC setups and shift toward adopting PCaaS to reduce permanent asset investments. Moreover, with hybrid workplace models implemented, businesses are expected to increase their dependence on services like PCaaS.

PC as a Service Industry Overview

Due to the existence of several large players like HP, Fujitsu, and AWS, among others, there is intense competition among the competitors in the PCaaS industry. They have a competitive advantage over rivals due to the continuous innovation of their product offerings. Additionally, they have expanded their market presence because of significant mergers and acquisitions, strategic alliances, and research and development investments.

In November 2022, Dell Technologies will enhance its high-performance computing (HPC) portfolio, providing solutions to help companies develop more securely. Dell's new offerings include technology and services that assist customers with power-demanding applications while also making HPC capabilities more accessible to companies.

In February 2022, Lenovo announced a portfolio of new products and solutions aimed at a more connected and hybrid world. The lineup comprises a diverse variety of smart products and solutions that support Lenovo's aim of bringing smarter technology to all.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand from Small and Medium-scale Organizations Due to Cost Benefits

- 4.2.2 Renewed Focus on Managed Service Providers

- 4.3 Market Restraints

- 4.3.1 Lack of Product Differentiation

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Type

- 5.2.1 Small and Medium-scale Organizations

- 5.2.2 Large Organizations

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 IT and Telecom

- 5.3.4 Government and Defense

- 5.3.5 Education

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lenovo Group Ltd

- 6.1.2 Dell Technologies

- 6.1.3 Brizbang LLC

- 6.1.4 Compucom Systems Inc. (Office Depot Inc.)

- 6.1.5 HP Inc.

- 6.1.6 Utopia Software LLC

- 6.1.7 Lanmark Ltd

- 6.1.8 Shi International Corp.

- 6.1.9 Telia

- 6.1.10 Intel Corporation

- 6.1.11 Symetri

- 6.1.12 XMA Ltd

7 INVESTMENT ANALYSIS

8 Future OF THE MARKET