Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690774

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690774

Europe Biodiesel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 110 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

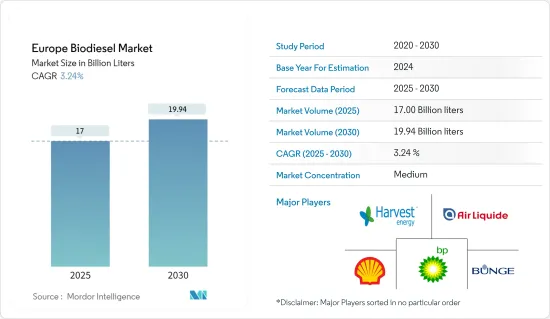

The Europe Biodiesel Market size is estimated at 17.00 billion liters in 2025, and is expected to reach 19.94 billion liters by 2030, at a CAGR of 3.24% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as government-supportive policies and regulations and concerns over energy security are expected to drive the market during the forecasted period.

- On the other hand, the availability and price of feedstocks, such as vegetable oils and animal fats, are expected to hinder the market's growth during the forecasted period.

- Nevertheless, research and development efforts focus on finding alternative biodiesel production feedstocks. Advanced feedstocks, such as algae and waste oils, offer the potential for improved sustainability, reduced land-use impact, and increased feedstock availability, creating new opportunities for biodiesel production.

- Germany is expected to dominate the market during the forecasted period. Due to supportive government policies.

Europe Biodiesel Market Trends

Palm Oil Is Likely To Dominate The Market

- Palm oil is one of the most widely produced vegetable oils globally. Major palm oil-producing countries, such as Indonesia and Malaysia, have large-scale plantations and efficient extraction processes, leading to a significant and reliable palm oil supply. This abundant supply gives palm oil a competitive advantage in terms of availability and cost compared to other feedstocks.

- Palm oil has a high energy content, making it an efficient feedstock for biodiesel production. Its energy density allows for higher biodiesel yields per unit of feedstock, resulting in cost-effective production. The energy efficiency of palm oil contributes to its attractiveness for biodiesel manufacturers and can potentially drive its dominance in the market.

- Moreover, palm oil possesses favorable properties for biodiesel production, such as its low viscosity and high lubricity. These properties enhance the performance of biodiesel in diesel engines and make it compatible with existing diesel infrastructure. The favorable properties of palm oil-based biodiesel contribute to its market potential and competitiveness.

- The value of biodiesel imported into Europe has increased significantly between 2021 and 2022. According to Statista, the total import value for biodiesel increased by more than 36%, signifying increased biodiesel consumption in the regions.

- In December 2022, the European Union reached a preliminary agreement to introduce a regulation that would mandate companies to provide evidence that their palm oil and other commodities sold within the EU are not linked to deforestation.

- Therefore, per the points discussed above, the palm oil segment will likely dominate the market during the forecasted period.

Germany to Dominate the Market

- Germany has implemented supportive policies and regulations to promote renewable energy, including biodiesel. The country has ambitious renewable energy targets and offers financial incentives and subsidies for biodiesel production. This support encourages investment and growth in the biodiesel industry, positioning Germany as a key player.

- Germany is known for its advanced engineering and technological expertise. The country has a strong research and development infrastructure, enabling innovative biodiesel production technologies to be developed and implemented. German companies are at the forefront of developing efficient and cost-effective biodiesel production processes, giving them a competitive advantage in the market.

- In February 2022, Renewable Energy Group announced its plans to enhance the pretreatment capacity at its biodiesel refinery in Emden, Germany. This expansion aims to enable the processing of challenging feedstocks into renewable fuel feed, including those that are typically difficult to convert.

- Germany has a well-developed infrastructure for producing, distributing, and using biodiesel. The country has many biodiesel production plants, an extensive blending facility network, and fueling stations. This existing infrastructure provides a solid foundation for the growth and dominance of the biodiesel market in Germany.

- In 2022, Germany's biodiesel consumption amounted to 2.516 million metric tons (around 755 million gallons), decreasing from 2.560 million tons (approximately 768.5 million gallons) in 2021. In contrast, ethanol utilization in blends grew nearly 2.9 percent, rising from 1.153 million tons (386 million gallons) to 1.186 million tons (approximately 397 million gallons).

- Therefore, as per the points mentioned above, Germany is likely to be a significant player in the biodiesel market in Europe.

Europe Biodiesel Industry Overview

Europe's biodiesel market is semi fragmented. Some of the major players in the market (in no particular order) include Shell PLC, BP PLC, Bunge Limited, Air Liquide SA, Harvest Energy, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 71558

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, until 2028

- 4.3 Government Policies and Regulations

- 4.4 Recent Trends and Developments

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Supportive Policies and Regulations

- 4.5.1.2 Energy Security

- 4.5.2 Restraints

- 4.5.2.1 Feedstock Availability and Price Volatility

- 4.5.1 Drivers

- 4.6 Supply-Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Feedstock

- 5.1.1 Rapeseed Oil

- 5.1.2 Palm Oil

- 5.1.3 Used Cooking Oil

- 5.1.4 Other Feedstocks

- 5.2 Biodiesel Blends

- 5.2.1 B5

- 5.2.2 B20

- 5.2.3 B100

- 5.3 Geography

- 5.3.1 Germany

- 5.3.2 Spain

- 5.3.3 United Kingdom

- 5.3.4 France

- 5.3.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shell PLC

- 6.3.2 BP PLC

- 6.3.3 Bunge Limited

- 6.3.4 Air Liquide SA

- 6.3.5 Harvest Energy

- 6.3.6 Abengoa Bioenergia SA

- 6.3.7 Envien Group

- 6.3.8 Greenergy International Ltd.

- 6.3.9 GBF German Biofuels GMBH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Advanced Feedstocks

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.