PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690722

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1690722

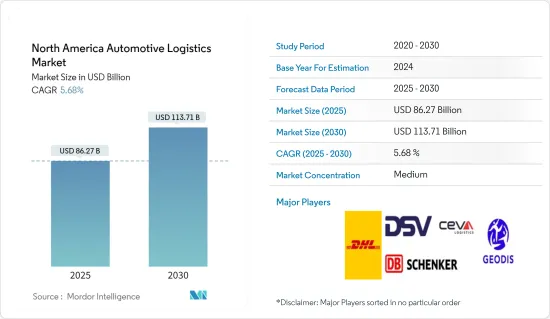

North America Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America Automotive Logistics Market size is estimated at USD 86.27 billion in 2025, and is expected to reach USD 113.71 billion by 2030, at a CAGR of 5.68% during the forecast period (2025-2030).

North American automotive logistics has rarely been on the verge of much change and opportunity. Yet, as in the broader automotive industry, there are few uncertainties about economic and trade risks, new regulations, consumer behavior, or returns on investment faced by vehicle logistics.

With greater visibility and more flexibility than ever before, the vehicle logistics sector must be able to compete. OEMs, logistics, and technology providers must collaborate to share data, plan, and upgrade technology to keep the supply chain flowing efficiently.

The future of automotive supply chains is vital to logistics service providers in the automotive sector and, at the macro level, whole economies. The nature of global trade and the dynamics of different national economies can be affected by any change in the supply chain structure for vehicles.

An increasing number of vehicle production facilities worldwide compels the growth of the automotive logistics market. In addition, the market growth is expected to accelerate in the coming years due to automobile manufacturers' significant business opportunities for logistics providers. In the post-recession era, emerging economies have seen steady growth, leading to a rise in disposable income for consumers.

North America Automotive Logistics Market Trends

Demand for Light Vehicle Production

- In North America, consumer preferences have shifted to sport utility vehicles and trucks, driving auto manufacturers to adapt their production to meet rising demand. Instances include the popularity of models like Ford Explorer and Chevrolet Silverado.

- Increased production of electric vehicles results from the increasing interest in hybrids and EVs. For example, in December 2023, Tesla's Gigafactory in Texas aimed to meet North America's growing demand for electric vehicles.

- The automotive industry in North America has been adapting to and investing in technologies to meet stringent emission standards, influencing the design and production of light vehicles. In August 2022, the US government signed the historic Inflation Reduction Act into law, which could prove to be the most critical economic and climate legislation in American history. The Act to reduce inflation, which has driven a revival in US manufacturing capacity, offers broad incentives for developing and manufacturing clean energy technologies.

- As the demand for light vehicle production rises, automotive logistics companies experience increased shipping volumes. More vehicles and components must be transported from manufacturing facilities to distribution centers and dealerships.

EV Boost in United States

- Federal and state-level incentives have been crucial in promoting EV adoption. The federal government offers tax credits for the purchase of qualifying electric vehicles. For instance, the Qualified Plug-In Electric Drive Motor Vehicle Credit provides a credit of up to USD 7,500.

- Major automakers have made substantial commitments to electric vehicles. Companies like General Motors (GM), Ford, and others have announced plans to invest in developing and producing electric vehicles. In January 2024, Ford Motor Co. inked a deal with a Minnesota-based company to buy a fleet of 1,000 all-electric vehicles, specifically the F-150 Lightning and Mustang Mach-E.

- During the first 11 months of 2023, EV registrations exceeded 1 million units, which is about 7.4% of the total market (up from 5.4% at this same time in 2022). Experts also stated that around 1.1 million battery-electric vehicles (BEVs) were sold in 2023. Tesla sold 1,739,707 Model 3/Y cars in 2023.

- The market's sustainable growth also depends on regulatory developments, given ongoing discussions among federal and national parties regarding the rollback of 2025 fuel-economy standards and state authority under the Clean Air Act.

North America Automotive Logistics Industry Overview

The North American Automotive Logistics Market is fragmented. The increasing demand for EVs, an increase in lighter vehicles, and several other factors are likely to drive the market's growth over the coming years. The competitive landscape is marked by key players such as DHL Supply Chain, Ryder System, and C.H. Robinson. These companies offer a comprehensive range of logistics and supply chain solutions, leveraging their global networks and advanced technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Government Regulations and Initiatives

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Technological Trends in the Industry

- 4.5 Spotlight - Effect of E-commerce on Traditional Automotive Logistics Supply Chain

- 4.6 Insights into Automotive Aftermarket and its Logistics Activities

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Environmental Concerns and Regulations

- 5.1.2 Technological Advancements in Automotive Technology

- 5.2 Market Restraints

- 5.2.1 Economic Uncertainty

- 5.3 Market Opportunities

- 5.3.1 Electric Vehicle Adoption

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Transportation

- 6.1.2 Warehousing, Distribution and Inventory Management

- 6.1.3 Other Services

- 6.2 By Type

- 6.2.1 Finished Vehicle

- 6.2.2 Auto Components

- 6.2.3 Other types

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

- 6.3.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 CEVA Logistics AG

- 7.2.2 DB Schenker

- 7.2.3 DHL

- 7.2.4 DSV

- 7.2.5 GEODIS

- 7.2.6 KUEHNE + NAGEL International AG

- 7.2.7 Nippon Express Co. Ltd

- 7.2.8 Ryder System Inc.

- 7.2.9 XPO Logistics Inc.

- 7.2.10 United Parcel Service Inc.*

- 7.3 Other Companies

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 APPENDIX

- 9.1 GDP Distribution, by Activity

- 9.2 Insights into Capital Flows

- 9.3 Economic Statistics-Transport and Storage Sector, Contribution to Economy