PUBLISHER: Reed Electronics Research | PRODUCT CODE: 1828244

PUBLISHER: Reed Electronics Research | PRODUCT CODE: 1828244

Yearbook of World Electronics Data Volume 2 2025 - An Overview of Electronics Production & Markets in the Americas, Japan & Asia Pacific

Introduction

In providing the forecasts for the current study, which were made at the end of July/beginning of August, we have:

- Taken into accounts developments in the European and global economy, and the on-going impact of tariffs on growth.

- That the impact of inventory balancing across several segments and notably industrial eased over the final months of 2024 with orders normalising in the first half of 2025.

- Component prices and shortages normalised in 2024 although tariffs have put pressure on prices in 2025.

- Consumer spending will remain subdued due to the combination of higher inflation and on-going geopolitical uncertainty.

- AI and data centre consumption will be a key driver of growth in the overall computer market in 2025 and 2026. We also expect demand to feed through to higher computer equipment production.

Americas

In 2024, electronics production in North America amounted to US$359 billion with the US dominating accounting for 79.3% of the total. Mexico, which acts as the low-cost production base for the region, 18.2% while Canada accounted for only 2.5%. After declining in US dollars by 0.1% in 2023, growth increased by 4.3% in 2024 and is forecast to grow by a more substantial 8.2% in 2025.

In Canada the growth in electronics output after increasing by 8.6% and 4.3% in 2022 and 2023, respectively eased to 1.2% in 2024 in part due to lower demand from key export markets. Communications and radar and control and instrumentation represented the largest segments accounting for 36.1% and 35.7% of electronics output, respectively in 2024. The component segment is small, accounting for only 7.5% of output in 2024.

In US dollars electronics output in Mexico increased by 6.3% in 2024 with growth seen across the computing, industrial and communications segments. Growth is forecast to increase by a more robust 15.2% in 2025 led by a 30% increase in computer output on the back of growth in AI and data centre related spending, and a 6.7% increase in communications production with this offset by slower growth in industrial and an 8.0% decline in consumer video.

Mexico will continue to benefit from foreign investment as both OEMs and EMS/ODMs look to utilise low-costs sites in the country as a production base to serve the North American market. The focus will remain on electronics equipment with limited investment expected in expanding the country's electronic components ecosystem.

After growth of 3.9% in 2023 the production of electronics equipment eased to 1.5% in 2024 but is forecast to rebound and increase by 4.3% in 2025 while electronics component output is forecast to increase by 13.1% in 2025 after posting double-digit growth of 11.9% in 2024 and a 6.0% decline in 2023.

The move by US companies to "re-shore" production has gained momentum and is expected to benefit from the move by US companies to localise manufacturing to offset higher tariffs. However, the US will face competition from Mexico for high-volume manufacturing.

Japan

Electronics output increased by 5.6% in 2024, a marked improvement compared to the prior year's decline of 2.8%. Electronics equipment, which accounted for 44.7% of the total, increased by 1.6% while components increased by 9.0%.

Based on official figures for the first six months of the year overall electronics output is forecast to increase by 1.9% in 2025, a 3.6% rise in electronic component production offset by a 1.9% increase in electronics equipment output.

The semiconductor and passive components sectors will continue to be the principal drivers of the Japanese electronics industry over the medium-term with the focus on products based on the latest technologies and continued investment in new capacity. The component sector will be supported by growth in the industrial segment, the emergence of new communication products driven by Internet of Things and 5G and the computer segment, in particular products supporting the development of AI.

Asia

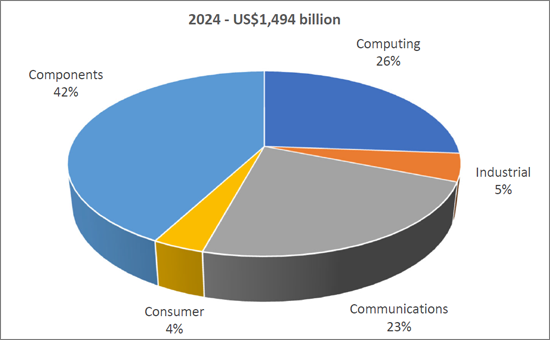

In 2024, the production of electronics equipment and components in Asia was valued at US$1,494 billion of which electronics equipment production accounted for 57.8% of the total with output dominated by computing and communications. Asia is also the centre for electronic component output globally.

China dominates electronics production in the region with total electronics output valued at US$801 billion in 2024. Taiwan and South Korea, with their strong focus on semiconductors, both reported electronics production of over US$150 billion in 2024 at US$164 billion and US$162 billion, respectively while Singapore with output of US$92 billion and Malaysia US$83 billion also benefited from an established semiconductor industry. Vietnam, which due to its lowcosts has seen explosive growth in recent years, is a major centre for the production of mobile phones with overall electronics output of US$81 billion in 2024. Electronics production in India was valued at US$49 billion in 2024 growth being supported by government incentives as the country looks to establish itself as a major global manufacturing hub.

Asian Electronics Production by Sector 2024

Published since 1983 Volume 2 of the Yearbook of World Electronics Data provides:

- A single source solution allowing you to track the electronics industry in 19 countries in the Americas, Japan and Asia Pacific.

- 13 major product groups.

- Market and production forecasts.

- CD-option allows you to manipulate the data quickly and easily: produce your own subsets or summaries of the data, create your own forecasts or cut and paste the data into your own in-house reports and presentations.

Who will benefit ?

The Yearbook is essential research providing key data for all areas of the electronics industry including:

- Distributors and manufacturers of electronic components and materials.

- Suppliers of electronic production equipment.

- OEMs.

- EMS Providers.

- Government, including investment organizations.

- Financial and industry analysts.

- Academic institutes & universities tracking developments in the electronics industry.

The Yearbook of World Electronics Data - tracking developments in the global electronics industry

With a history now extending over 50 years, the first edition of the Volume 1 of the Yearbook of World Electronics Data was first published in 1973, the Yearbook series has been extended to cover 53 countries globally to provide an invaluable and unique insight into the global trends, regional variations and the underlying state of the global electronics market for all stages of the supply chain - OEM, contract manufacturing and design, components and materials suppliers to financial /industry analysts and government and academia.

Although encompassing a range of published and bespoke products the core of RER's research programme is one of the most comprehensive statistical databases covering the global electronics industry, with the resulting analysis being published through three concise and clear demographic volumes, as a series of individual country reports, through customised solutions to meet specific client requirements and a series of Excel databases providing the combination of both historical and forecasted data.

53 country coverage, 13 major product groups

... comparable country by country and product by product.

TABLE OF CONTENTS

1. INTRODUCTION

2. SUMMARY DATA

- 2.1. Economic Overview

- 2.2. Electronics Overview

- 2.2.1. Americas

- 2.2.2. Japan

- 2.2.3. Asia

- 2.3. Imports 2022-2023

- 2.4. Exports 2022-2023

- 2.5. Consolidated Summary of Production 2022

- 2.6. Consolidated Summary of Production 2023

- 2.7. Consolidated Summary of Production 2024

- 2.8. Consolidated Summary of Production 2025

- 2.9. Summary of Medical & Industrial Production

- 2.10. Summary of Consumer Production

- 2.11. Summary of Components Production

- 2.12. Summary of Active Component Production

- 2.13. Summary of Passive Component Production

- 2.14. Summary of Other Component Production

- 2.15. America, Japan, Asia Pacific Total Production

- 2.16. Consolidated Summary of Markets 2022

- 2.17. Consolidated Summary of Markets 2023

- 2.18. Consolidated Summary of Markets 2024

- 2.19. Consolidated Summary of Markets 2025

- 2.20. Consolidated Summary of Markets 2026

- 2.21. Consolidated Summary of Markets 2027

- 2.22. Consolidated Summary of Markets 2028

- 2.23. Summary of Medical & Industrial Markets

- 2.24. Summary of Consumer Markets (Value)

- 2.25. Summary of Components Markets

- 2.26. Summary of Active Component Markets

- 2.27. Summary of Passive Component Markets

- 2.28. Summary of Other Component Markets

- 2.29. America, Japan, Asia Pacific Total Markets

3. COUNTRY DATA

- 3.1. AUSTRALIA

- 3.1.1. Economic Outlook

- 3.1.2. Electronics Industry Overview

- 3.1.3. Australia Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.1.4. Australia Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.2. BRAZIL

- 3.2.1. Economic Outlook

- 3.2.2. Electronics Industry Overview

- 3.2.3. Brazil Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.2.4. Brazil Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.3. CANADA

- 3.3.1. Economic Outlook

- 3.3.2. Electronics Industry Overview

- 3.3.3. Canada Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.3.4. Canada Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.4. CHINA

- 3.4.1. Economic Outlook

- 3.4.2. Electronics Industry Overview

- 3.4.3. China Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.4.4. China Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.5. HONG KONG

- 3.5.1. Economic Outlook

- 3.5.2. Electronics Industry Overview

- 3.5.3. Hong Kong Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.5.4. Hong Kong Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.6. INDIA

- 3.6.1. Economic Outlook

- 3.6.2. Electronics Industry Overview

- 3.6.3. India Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.6.4. India Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.7. INDONESIA

- 3.7.1. Economic Outlook

- 3.7.2. Electronics Industry Overview

- 3.7.3. Indonesia Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.7.4. Indonesia Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.8. ISRAEL

- 3.8.1. Economic Outlook

- 3.8.2. Electronics Industry Overview

- 3.8.3. Israel Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.8.4. Israel Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.9. JAPAN

- 3.9.1. Economic Outlook

- 3.9.2. Electronics Industry Overview

- 3.9.3. Japan Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.9.4. Japan Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.10. MALAYSIA

- 3.10.1. Economic Outlook

- 3.10.2. Electronics Industry Overview

- 3.10.3. Malaysia Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.10.4. Malaysia Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.11. MEXICO

- 3.11.1. Economic Outlook

- 3.11.2. Electronics Industry Overview

- 3.11.3. Mexico Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.11.4. Mexico Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.12. PHILIPPINES

- 3.12.1. Economic Outlook

- 3.12.2. Electronics Industry Overview

- 3.12.3. Philippines Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.12.4. Philippines Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.13. SINGAPORE

- 3.13.1. Economic Outlook

- 3.13.2. Electronics Industry Overview

- 3.13.3. Singapore Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.13.4. Singapore Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.14. SOUTH AFRICA

- 3.14.1. Economic Outlook

- 3.14.2. Electronics Industry Overview

- 3.14.3. South Africa Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.14.4. South Africa Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.15. SOUTH KOREA

- 3.15.1. Economic Outlook

- 3.15.2. Electronics Industry Overview

- 3.15.3. South Korea Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.15.4. South Korea Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.16. TAIWAN

- 3.16.1. Economic Outlook

- 3.16.2. Electronics Industry Overview

- 3.16.3. Taiwan Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.16.4. Taiwan Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.17. THAILAND

- 3.17.1. Economic Outlook

- 3.17.2. Electronics Industry Overview

- 3.17.3. Thailand Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.17.4. Thailand Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.18. USA

- 3.18.1. Economic Outlook

- 3.18.2. Electronics Industry Overview

- 3.18.3. USA Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.18.4. USA Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

- 3.19. VIETNAM

- 3.19.1. Economic Outlook

- 3.19.2. Electronics Industry Overview

- 3.19.3. Vietnam Production

- Computing 2022-2025

- Office Equipment 2022-2025

- Control & Instrumentation 2022-2025

- Medical & Industrial 2022-2025

- Communications & Radar 2022-2025

- Telecommunications 2022-2025

- Consumer 2022-2025

- Video 2022-2025

- Audio 2022-2025

- Personal 2022-2025

- Components 2022-2025

- Active 2022-2025

- Passive 2022-2025

- Other 2022-2025

- 3.19.4. Vietnam Markets

- Computing 2022-2028

- Office Equipment 2022-2028

- Control & Instrumentation 2022-2028

- Medical & Industrial 2022-2028

- Communications & Radar 2022-2028

- Telecommunications 2022-2028

- Consumer 2022-2028

- Video 2022-2028

- Audio 2022-2028

- Personal 2022-2028

- Components 2022-2028

- Active 2022-2028

- Passive 2022-2028

- Other 2022-2028

4. APPENDICES

- 4.1. Exchange Rates

- 4.2. Guide to Interpretation of the Statistics

- 4.3. Guide to Statistical Trade Classifications

- 4.4. Guide to the Definition of Electronic Product Headings

- 4.5. List of Sources