PUBLISHER: Roots Analysis | PRODUCT CODE: 2015364

PUBLISHER: Roots Analysis | PRODUCT CODE: 2015364

Satellite NTN Market, Till 2040: Industry Trends and Global Forecasts

Satellite NTN Market Outlook

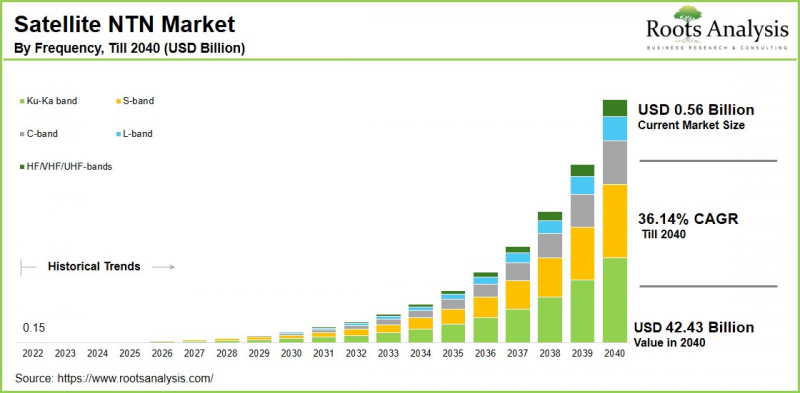

As per Roots Analysis, the global satellite NTN market size is estimated to grow from USD 0.56 billion in current year to USD 42.43 billion by 2040, at a CAGR of 36.14% during the forecast period, till 2040.

Satellite Non-Terrestrial Networks (NTN) refer to wireless communication systems that leverage space- and aerial-based platforms, to deliver connectivity beyond traditional ground-based cellular infrastructure. By extending network coverage to remote regions, and sparsely populated areas, NTN solutions address connectivity gaps where terrestrial networks remain limited or economically unviable.

Satellite NTN technology supports a wide range of applications, enabling reliable communication for navigation, air traffic management, asset tracking, and distributed sensor networks. With capabilities such as direct-to-device connectivity and satellite backhaul integration, NTN enhances data collection, monitoring, and control from virtually any location worldwide. The convergence of satellite and cellular technologies, particularly through 5G and emerging 6G frameworks, is significantly strengthening the deployment of Non-Terrestrial Networks (NTN). As global demand for sustainable connectivity intensifies, satellite NTN is positioned as a strategic enabler of next-generation communication infrastructure.

Strategic Insights for Senior Leaders

Key Drivers Propelling Growth of Satellite NTN Market

The growth of the Satellite Non-Terrestrial Network (NTN) market is driven by the rapid expansion of 5G and its integration with terrestrial networks. This integration enables seamless global coverage, real-time data exchange, enhanced backhaul for remote regions, and standardized deployment through 3GPP protocols. Simultaneously, the increasing deployment of Low Earth Orbit (LEO) satellite constellations equipped with advanced, high-capacity payloads and low-latency links is strengthening the competitiveness of NTN solutions, particularly for broadband services, emergency response, and direct-to-user connectivity.

Moreover, expanding initiatives focused on improving broadband access and bridging the digital divide are accelerating satellite NTN adoption across rural and underserved areas. This trend is particularly evident in high-growth regions such as Asia-Pacific, Africa, and North America, despite fluctuations in commercial sector investments.

Satellite NTN Market: Competitive Landscape of Companies in this Industry

The satellite Non-Terrestrial Network (NTN) market is highly fragmented and characterized by intense competition. Companies are strengthening their market positions through strategic partnerships, investments in multi-orbit constellations, thereby unlocking sustainable revenue streams.

Satellite manufacturers continue to play a dominant role by leveraging strong space system integration expertise and established distribution networks to support 5G and next-generation mobile connectivity. Key industry participants include Airbus Defence and Space, Amazon, Apple, AST SpaceMobile, BAE Systems, Eutelsat OneWeb, Honeywell International, Hughes Network Systems, L3Harris Technologies, Lockheed Martin, NEC Corporation, Safran, SES, SpaceX, SWISSto12, Teledyne, Telesat, and Viasat. These organizations are pursuing aggressive growth strategies focused on technological innovation, strategic alliances, and portfolio diversification. For example, recently, SES announced its acquisition of Intelsat to create a stronger global multi-orbit operator capable of serving evolving customer demands across government, aviation, and smart city NTN infrastructure applications.

Regulatory Framework and Spectrum Management in Satellite NTN

The deployment of Satellite Non-Terrestrial Networks (NTN) is subject to complex regulatory and operational constraints, particularly in spectrum coordination and management. As NTN systems share frequency bands with terrestrial mobile networks, strict coexistence requirements, such as transmission power limits and interference mitigation measures, must be implemented to safeguard ground-based services. As a result, satellite operators face increased payload complexity and more tightly defined coverage parameters. Additionally, licensing frameworks often require satellite operators to collaborate with mobile network operators (MNOs) to access spectrum rights, creating operational dependencies and limiting flexibility in service deployment, which can slow innovation across certain frequency bands. Regulatory mandates further influence technical architecture, increasing payload complexity, power consumption considerations, and adaptive coverage strategies. Collectively, these factors elevate costs and introduce operational constraints that may affect service quality and the scalability of global NTN deployments.

Regional Analysis of Satellite NTN Market

According to our estimates, North America holds a significant market share. This is driven by the rapid rollout of 5G, coupled with substantial government and defense investments in secure and resilient communication networks. Within North America, the United States represents the largest contributor to market revenue, driven by strong demand for satellite-enabled connectivity and national initiatives aimed at bridging the digital divide.

Companies such as SpaceX are expanding high-speed satellite internet services through the Starlink constellation, including direct-to-device connectivity applications that enhance cross-industry communication and orbital service capabilities. Furthermore, supportive regulatory frameworks, continued 5G expansion, Low Earth Orbit (LEO) deployments, and defense-commercial collaboration are fostering innovation.

Key Challenges in Satellite NTN Market

The satellite Non-Terrestrial Network (NTN) market faces several structural risks that may impact long-term sustainability and deployment timelines. Global disruptions have exposed supply chain vulnerabilities within satellite manufacturing and launch ecosystems, leading to delays in service rollouts and increased dependency on limited suppliers. Simultaneously, the rapid expansion of Low Earth Orbit (LEO) and Geostationary Orbit (GEO) constellations has intensified concerns regarding orbital congestion, space debris accumulation, and spectrum interference, necessitating robust international coordination and regulatory oversight.

Moreover, growing scrutiny around environmental impact, emissions, and data privacy is compelling satellite NTN providers to adopt sustainable operational practices.

Satellite NTN Market: Key Market Segmentation

Market Share by Technology

- IoT NTN

- NTN NR

Market Share by Component

- Hardware

- Antenna Onboard Processors

- Onboard Processor Unit

- RF Front End

- Service

- Ground Segment and Terminal Equipment

- Managed Security Services

- Network services

- Satellite infrastructure

- System Integration

- Software

Market Share by Frequency

- C-band

- HF/VHF/UHF-bands

- Ku-Ka band

- L-band

- S-band

Market Share by Orbit

- Geostationary Orbit (GEO)

- Highly Elliptical Orbit (HEO)

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

Market Share by Architecture

- Regenerative Payload

- Transparent Payload

Market Share by Application

- Backhole and network extension

- Broadband Internet Access

- Direct to device connectivity

- IOT/MTM connectivity

Market Share by End Use

- Commercial

- Government

- Defense

Market Share by Geographical Regions

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Rest of Europe

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Rest of Asia

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Rest of Latin America

- Middle East and Africa (MEA)

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Rest of the MEA

- Rest of the World

- Australia

- New Zealand

- Other countries

Example Players in Satellite NTN Market

- Airbus Defense and Space

- Amazon

- Apple

- AST SpaceMobile

- BAE Systems

- Eutelsat OneWeb

- Honeywell International

- Hughes Network Systems

- L3Harris Technologies

- Lockheed Martin

- NEC Corporation

- Safran

- SES

- SpaceX

- SWISSto12

- Teledyne

- Telesat

- Viasat

Satellite NTN Market: Report Coverage

The report on the satellite NTN market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the satellite NTN market, focusing on key market segments, including [A] technology, [B] frequency, [C] orbit, [D] architecture, [E] application, [F] end use, [G] geographical regions and [H] key players.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the satellite NTN market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the satellite NTN market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] product / technology portfolio, [J] recent developments, and an informed future outlook.

- Megatrends: An evaluation of ongoing megatrends in the satellite NTN industry.

- Patent Analysis: An insightful analysis of patents filed / granted in the satellite NTN domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

- Recent Developments: An overview of the recent developments made in the satellite NTN market, along with analysis based on relevant parameters, including [A] year of initiative, [B] type of initiative, [C] geographical distribution and [D] most active players.

- Porter's Five Forces Analysis: An analysis of five competitive forces prevailing in the satellite NTN market, including threats of new entrants, bargaining power of buyers, bargaining power of suppliers, threats of substitute products and rivalry among existing competitors.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2040?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- Detailed Market Analysis: The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- In-depth Analysis of Trends: Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. Each report maps ecosystem activity across partnerships, funding, and patent landscapes to reveal growth hotspots and white spaces in the industry.

- Opinion of Industry Experts: The report features extensive interviews and surveys with key opinion leaders and industry experts to validate market trends mentioned in the report.

- Decision-ready Deliverables: The report offers stakeholders with strategic frameworks (Porter's Five Forces, value chain, SWOT), and complimentary Excel / slide packs with customization support.

Additional Benefits

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

1. PROJECT OVERVIEW

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Concluding Remarks

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Satellite NTN Market

- 6.2.1. Technology for Satellite NTN

- 6.2.2. Advantages of Satellite NTN

- 6.2.3. Challenges Associated with Satellite NTN

- 6.3. Future Perspective

7. REGULATORY SCENARIO

8. COMPREHENSIVE DATABASE OF LEADING PLAYERS

9. COMPETITIVE LANDSCAPE

- 9.1. Chapter Overview

- 9.2. Satellite NTN Market: Overall Landscape

- 9.2.1. Analysis by Year of Establishment

- 9.2.2. Analysis by Company Size

- 9.2.3. Analysis by Location of Headquarters

- 9.2.4. Analysis by Ownership Structure

- 9.3. Key Findings

10. WHITE SPACE ANALYSIS

11. COMPANY COMPETITIVENESS ANALYSIS

12. STARTUP ECOSYSTEM IN THE SATTELITE NTN MARKET

- 12.1. Satellite NTN: Market Landscape of Startups

- 12.1.1. Analysis by Year of Establishment

- 12.1.2. Analysis by Location of Headquarters

- 12.1.3. Analysis by Ownership Structure

- 12.1.4. Analysis by Type of Material

- 12.1.5. Analysis by Type of Installation

- 12.1.6. Analysis by Application Area

13. COMPANY PROFILES

- 13.1. Chapter Overview

- 13.2. Airbus Defense and Space*

- 13.2.1. Company Overview

- 13.2.2. Company Mission

- 13.2.3. Company Footprint

- 13.2.4. Management Team

- 13.2.5. Contact Details

- 13.2.6. Financial Performance

- 13.2.7. Operating Business Segments

- 13.2.8. Service / Product Portfolio (project specific)

- 13.2.9. MOAT Analysis

- 13.2.10. Recent Developments and Future Outlook

- Similar details are presented for other companies mentioned below (based on information in the public domain)

- 13.3. Amazon

- 13.4. Apple

- 13.5. AST SpaceMobile

- 13.6. BAE Systems

- 13.7. Eutelsat OneWeb

- 13.8. Honeywell International

- 13.9. Hughes Network Systems

- 13.10. L3Harris Technologies

- 13.11. Lockheed Martin

- 13.12. NEC Corporation

- 13.13. Safran

- 13.14. SES

- 13.15. SpaceX

- 13.16. SWISSto12

- 13.17. Teledyne

- 13.18. Telesat

- 13.19. Viasat

14. MEGA TRENDS ANALYSIS

15. UNMET NEED ANALYSIS

16. PATENT ANALYSIS

17. RECENT DEVELOPMENTS

- 17.1. Chapter Overview

- 17.2. Recent Funding

- 17.3. Recent Partnerships

- 17.4. Other Recent Initiatives

18. GLOBAL SATTELITE NTN MARKET

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Trends Disruption Impacting Market

- 18.4. Demand Side Trends

- 18.5. Supply Side Trends

- 18.6. Global Satellite NTN Market: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 18.7. Multivariate Scenario Analysis

- 18.7.1. Conservative Scenario

- 18.7.2. Optimistic Scenario

- 18.8. Investment Feasibility Index

- 18.9. Key Market Segmentations

19. MARKET OPPORTUNITIES BASED ON TECHNOLOGY

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Satellite NTN Market for IoT NTN: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.7. Satellite NTN Market for NTN NR: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 19.8. Data Triangulation and Validation

- 19.8.1. Secondary Sources

- 19.8.2. Primary Sources

- 19.8.3. Statistical Modeling

20. MARKET OPPORTUNITIES BASED ON COMPONENT

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Satellite NTN Market for Hardware: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.7. Hardware Satellite NTN Market for Antenna Onboard Processors: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.8. Hardware Satellite NTN Market for Onboard Processor Unit: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.9. Hardware Satellite NTN Market for RF Front End: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.10. Satellite NTN Market for Service: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.11. Service Satellite NTN Market for Ground Segment and Terminal Equipment: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.12. Service Satellite NTN Market for Managed Security Services: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.13. Service Satellite NTN Market for Network services: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.14. Service Satellite NTN Market for Satellite infrastructure: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.15. Service Satellite NTN Market for System Integration: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.16. Satellite NTN Market for Software: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 20.17. Data Triangulation and Validation

- 20.17.1. Secondary Sources

- 20.17.2. Primary Sources

- 20.17.3. Statistical Modeling

21. MARKET OPPORTUNITIES BASED ON FREQUENCY

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Satellite NTN Market for C-band: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.7. Satellite NTN Market for HF/VHF/UHF-bands: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.8. Satellite NTN Market for Ku-Ka band: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.9. Satellite NTN Market for L-band: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.10. Satellite NTN Market for S-band: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 21.11. Data Triangulation and Validation

- 21.11.1. Secondary Sources

- 21.11.2. Primary Sources

- 21.11.3. Statistical Modeling

22. MARKET OPPORTUNITIES BASED ON ORBIT

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Satellite NTN Market for Geostationary Orbit (GEO): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.7. Satellite NTN Market for Highly Elliptical Orbit (HEO): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.8. Satellite NTN Market for Low Earth Orbit (LEO): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.9. Satellite NTN Market for Medium Earth Orbit (MEO)Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 22.10. Data Triangulation and Validation

- 22.10.1. Secondary Sources

- 22.10.2. Primary Sources

- 22.10.3. Statistical Modeling

23. MARKET OPPORTUNITIES BASED ON ARCHITECTURE

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Satellite NTN Market for Regenerative Payload: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.7. Satellite NTN Market for Transparent Payload: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 23.8. Data Triangulation and Validation

- 23.8.1. Secondary Sources

- 23.8.2. Primary Sources

- 23.8.3. Statistical Modeling

24. MARKET OPPORTUNITIES BASED ON APPLICATION

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. Satellite NTN Market for Backhole and network extension: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.7. Satellite NTN Market for Broadband Internet Access: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.8. Satellite NTN Market for Direct to device connectivity: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.9. Satellite NTN Market for IOT/MTM connectivity: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 24.10. Data Triangulation and Validation

- 24.10.1. Secondary Sources

- 24.10.2. Primary Sources

- 24.10.3. Statistical Modeling

25. MARKET OPPORTUNITIES BASED ON END USER

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. Satellite NTN Market for Commercial: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.7. Satellite NTN Market for Government: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.8. Satellite NTN Market for Defense: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 25.9. Data Triangulation and Validation

- 25.9.1. Secondary Sources

- 25.9.2. Primary Sources

- 25.9.3. Statistical Modeling

26. MARKET OPPORTUNITIES FOR SATELLITE NTN IN NORTH AMERICA

- 26.1. Chapter Overview

- 26.2. Key Assumptions and Methodology

- 26.3. Revenue Shift Analysis

- 26.4. Market Movement Analysis

- 26.5. Penetration-Growth (P-G) Matrix

- 26.6. Satellite NTN Market in North America: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.1. Satellite NTN Market in the US: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.2. Satellite NTN Market in Canada: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.3. Satellite NTN Market in Mexico: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.6.4. Satellite NTN Market in Other North American Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 26.7. Data Triangulation and Validation

27. MARKET OPPORTUNITIES FOR SATELLITE NTN IN EUROPE

- 27.1. Chapter Overview

- 27.2. Key Assumptions and Methodology

- 27.3. Revenue Shift Analysis

- 27.4. Market Movement Analysis

- 27.5. Penetration-Growth (P-G) Matrix

- 27.6. Satellite NTN Market in Europe: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.1. Satellite NTN Market in Austria: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.2. Satellite NTN Market in Belgium: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.3. Satellite NTN Market in Denmark: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.4. Satellite NTN Market in France: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.5. Satellite NTN Market in Germany: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.6. Satellite NTN Market in Ireland: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.7. Satellite NTN Market in Italy: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.8. Satellite NTN Market in Netherlands: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.9. Satellite NTN Market in Norway: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.10. Satellite NTN Market in Russia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.11. Satellite NTN Market in Spain: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.12. Satellite NTN Market in Sweden: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.13. Satellite NTN Market in Switzerland: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.14. Satellite NTN Market in the UK: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.6.15. Satellite NTN Market in Other European Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 27.7. Data Triangulation and Validation

28. MARKET OPPORTUNITIES FOR SATELLITE NTN IN ASIA

- 28.1. Chapter Overview

- 28.2. Key Assumptions and Methodology

- 28.3. Revenue Shift Analysis

- 28.4. Market Movement Analysis

- 28.5. Penetration-Growth (P-G) Matrix

- 28.6. Satellite NTN Market in Asia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.1. Satellite NTN Market in China: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.2. Satellite NTN Market in India: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.3. Satellite NTN Market in Japan: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.4. Satellite NTN Market in Singapore: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.5. Satellite NTN Market in South Korea: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.6.6. Satellite NTN Market in Other Asian Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 28.7. Data Triangulation and Validation

29. MARKET OPPORTUNITIES FOR SATELLITE NTN IN LATIN AMERICA

- 29.1. Chapter Overview

- 29.2. Key Assumptions and Methodology

- 29.3. Revenue Shift Analysis

- 29.4. Market Movement Analysis

- 29.5. Penetration-Growth (P-G) Matrix

- 29.6. Satellite NTN Market in Latin America: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.1. Satellite NTN Market in Argentina: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.2. Satellite NTN Market in Brazil: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.3. Satellite NTN Market in Chile: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.4. Satellite NTN Market in Colombia Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.5. Satellite NTN Market in Venezuela: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.6.6. Satellite NTN Market in Other Latin American Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 29.7. Data Triangulation and Validation

30. MARKET OPPORTUNITIES FOR SATELLITE NTN IN MIDDLE EAST AND AFRICA (MEA)

- 30.1. Chapter Overview

- 30.2. Key Assumptions and Methodology

- 30.3. Revenue Shift Analysis

- 30.4. Market Movement Analysis

- 30.5. Penetration-Growth (P-G) Matrix

- 30.6. Satellite NTN Market in Middle East and North Africa (MENA): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.1. Satellite NTN Market in Egypt: Historical Trends (Since 2022) and Forecasted Estimates (Till 205)

- 30.6.2. Satellite NTN Market in Iran: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.3. Satellite NTN Market in Iraq: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.4. Satellite NTN Market in Israel: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.5. Satellite NTN Market in Kuwait: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.6. Satellite NTN Market in Saudi Arabia: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.7. Satellite NTN Market in United Arab Emirates (UAE): Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.6.8. Satellite NTN Market in Other MEA Countries: Historical Trends (Since 2022) and Forecasted Estimates (Till 2040)

- 30.7. Data Triangulation and Validation

31. MARKET CONCENTRATION ANALYSIS: DISTRIBUTION BY LEADING PLAYERS

32. ADJACENT MARKET ANALYSIS

33. KEY WINNING STRATEGIES

34. PORTER'S FIVE FORCES ANALYSIS

35. SWOT ANALYSIS

36. VALUE CHAIN ANALYSIS

37. ROOTS STRATEGIC RECOMMENDATIONS

- 37.1. Chapter Overview

- 37.2. Key Business-related Strategies

- 37.2.1. Research & Development

- 37.2.2. Product Manufacturing

- 37.2.3. Commercialization / Go-to-Market

- 37.2.4. Sales and Marketing

- 37.3. Key Operations-related Strategies

- 37.3.1. Risk Management

- 37.3.2. Workforce

- 37.3.3. Finance

- 37.3.4. Others

38. INSIGHTS FROM PRIMARY RESEARCH

39. REPORT CONCLUSION

40. TABULATED DATA

41. LIST OF COMPANIES AND ORGANIZATIONS